NAHB analysis of Census Construction Spending data shows that total private residential construction spending stood at a seasonally adjusted annual rate (SAAR) of $550.3 billion in March. It was up 2.3% in March, after decreasing 4.8% in February. On a year-over-year basis, total private construction spending rose 8.8%.

The monthly gains are largely attributed to the growth of spending on improvements and multifamily construction. Private residential improvements, which include spending on remodeling, major replacement, and additions to owner-occupied housing units, increased to $189.0 billion annual pace in March, up 10.2% over the February estimates. Multifamily construction spending inched up 2% in March, following an increase of 1.2% in February. Spending on single-family construction slipped 2.0% in March, the first dip since July 2019, due to the virus impacts.

The NAHB construction spending index, which is shown in the graph below (the base is January 2000), illustrates the solid growth in single-family construction and home improvement from the second half of 2019 to February 2020, before the COVID-19 hit the U.S. economy. New multifamily construction spending slowed down since August 2019, after the strong growth from 2010 to 2016 and a surge from the late 2018 to early 2019.

Spending on private nonresidential construction declined 1.8 percent over the year to a seasonally adjusted annual rate of $462.3 billion. The annual nonresidential spending decline was mainly due to less spending on the class of lodging ($4.3 billion), followed by educational category ($3.6 billion), and amusement and recreation ($2.3 billion).

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage (FRM) averaged 3.33 percent.

“Mortgage rates have drifted down for two weeks in a row and that drop reflects improvements in market liquidity and sentiment,” said Sam Khater, Freddie Mac’s Chief Economist. “While the market has stabilized relative to prior weeks, homebuyer demand has declined in response to current economic conditions. The good news is that the pending economic stimulus is on the way and will provide support for both consumers and businesses.”

News Facts

30-year fixed-rate mortgage averaged 3.33 percent with an average 0.7 point for the week ending April 2, 2020, down from last week when it averaged 3.50 percent. A year ago at this time, the 30-year FRM averaged 4.08 percent.

15-year fixed-rate mortgage averaged 2.82 percent with an average 0.6 point, down from last week when it averaged 2.92 percent. A year ago at this time, the 15-year FRM averaged 3.56 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.40 percent with an average 0.3 point, up from last week when it averaged 3.34 percent. A year ago at this time, the 5-year ARM averaged 3.66 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

In the fourth quarter of 2019, the delinquency rate for mortgage loans on single-family homes1 decreased to 3.8% of all loans outstanding, according to the latest iteration of the Mortgage Bankers Association’s National Delinquency Survey. This is the lowest it has been since the series started in 1979. The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. Additionally, the “seriously delinquent” rate, the percentage of loans that are 90 days or more past due or are in the process of foreclosure decreased to 1.8%, the lowest it has been since 2005.

The above figure shows the serious delinquency rate of all loans and its components, FHA and VA loans, which are government-insured mortgages, and conventional loans. The seriously delinquent rates of FHA and VA loans increased from the previous quarter. For the fourth quarter of 2019, the five states with the lowest seriously delinquent rates were Colorado, California, Washington, Arizona, and Oregon and the five states with the highest seriously delinquent rates were Puerto Rico, New York, Mississippi, Louisiana, and Maine.

Notes:

For simplicity, the term “single-family” is used but denotes one- to four-unit residential properties.

Some of the hardest evidence yet indicates that the 2017 Republican tax law is pushing money and people from high-tax U.S. states like New York and New Jersey and into low-tax states including Florida.

In 2018, low- and lower-tax states gained $32 billion more in adjusted gross income than higher tax states, according to a Bank of America Global Research analysis of income migration data. You can visit here https://taxfyle.com/blog/how-does-adjusted-gross-income-work/ about how adjusted gross income work. The net gain — almost $2 billion more than in 2017 — was nearly twice the average over the last 13 years. The Republican overhaul capped state and local deductions at $10,000, making it harder for people to shield as much income from taxes as they could before.

At the same time, states like Florida and Texas, which don’t have an income tax, are seeing more and more people move there. New York, California, Connecticut and New Jersey — the states that had the highest average SALT deductions, lost about 455,000 people between July 1, 2018 and July 1, 2019, compared with 408,500 the prior year, according to U.S. Census data. Most of the increase came from people leaving California.

“The implication would be at the very least, people are sensitive to large changes in federal tax policy,” said Ian Rogow, a municipal strategist at Bank of America who analyzed the data.

Almost half of income taxes paid to California, New York and New Jersey come from the wealthiest 1% of households. If they were to move in large enough numbers, those states could be in trouble. So far, however, the federal tax overhaul — which broadened the tax base — and steady economy growth has led to higher-tax state revenue overall. States collected $327.7 billion in income tax revenue in the first three quarters of 2019, about 6% more than the same period in 2018, according to the Census Bureau.

To be sure, people move for a variety of reasons: jobs, housing costs and the weather among them. Despite having the third-highest personal income tax rate, Oregon was the second-most popular moving destination in the U.S., according to United Van Lines Annual Movers Study. The survey found that job changes and retirement were the two biggest reasons for leaving the northeast.

Related: Florida, Trump’s New Home, Leads U.S. in the Migration of Money

The Republicans’ 2017 tax law capped the SALT deduction as a way to help pay for $1.5 trillion in corporate and personal income tax cuts. Governors in Democratic-led states most affected by the new limit, including New York and New Jersey, accused Republicans of targeting them to pay for the cut. In October a federal judge ruled against New York, New Jersey, Connecticut and Maryland, which had sued to overturn the cap, arguing it was unconstitutional. The states are appealing.

The SALT limit significantly raised the effective taxes for wealthy residents of blue states. In 2017, about 140,000 tax filers in Manhattan with adjusted gross income of $200,000 or more paid $21 billion in state and local income taxes, or $150,000 on average, according to IRS data. About 83,000 of these filers paid an average $25,000 in property taxes. In Westchester, home to the nation’s highest property taxes, the wealthiest residents paid about an average $65,000 in state and local income taxes and $28,000 in real estate taxes.

In the fourth quarter of 2019, Westchester homeowners cut an average of 4.1% from their last asking price to sell their homes, according to a report last week, a sign that sellers have to slash prices to attract to buyers. The price cuts were the most for any three-month period since the end of 2014, according to a the report by appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate.

New York Governor Andrew Cuomo who has called the SALT limits “politically diabolical,” has warned that capping the deduction encourages high-income New Yorkers to leave.

“Tax the rich, tax the rich, tax the rich. We did. Now, God forbid the rich leave,” Cuomo said last year.

The codes, most of them passed since June, are meant to keep builders from running natural gas lines to new homes and apartments, with an eye toward creating fewer legacy gas hookups as the nation shifts to carbon-neutral energy sources.

For proponents, it’s a change that must be made to fight climate change. For natural gas companies, it’s a threat to their existence. And for some cooks who love to prepare food with flame, it’s an unthinkable loss.

Natural gas is a fossil fuel, mostly methane, and produces 33% of U.S. carbon dioxide emissions from electricity generation, according to the U.S. Energy Information Administration. Carbon dioxide is the primary greenhouse gas causing climate change.

“There’s no pathway to stabilizing the climate without phasing gas out of our homes and buildings. This is a must-do for the climate and a livable planet,” said Rachel Golden of the Sierra Club’s building electrification campaign.

These new building codes come as local governments work to speed the transition from natural gas and other fossil fuels and toward the use of electricity from renewables, said Robert Jackson, a professor of energy and the environment at Stanford University in Palo Alto, California.

it’s important to check your house for air flow indoors or add a gas fitter chelmer to avoid allergies at home.

“Every house, every high-rise that’s built with gas, may be in place for decades. We’re establishing infrastructure that may be in place for 50 years,” he said.

These “reach” or “stretch” building codes, as they are known, have so far all been passed in California. The first was in Berkeley in July, then more in Northern California and recently Santa Monica in Southern California. Other cities in Massachusetts, Oregon and Washington state are contemplating them, according to the Sierra Club.

Some of the cities ban natural gas hookups to new construction. Others offer builders incentives if they go all-electric, much the same as they might get to take up more space on a lot if a house is extra energy-efficient. In April, Sunnyvale, a town in Silicon Valley, changed its building code to offer a density bonus to all-electric developments.

No more gas stoves?

The building codes apply only to new construction beginning in 2020, so they aren’t an issue for anyone in an already-built home.

Probably the biggest stumbling block for most pondering an all-electric home is the prospect of not having a gas stove.

“It’s the only thing that people ever ask about,” said Bruce Nilles, who directs the building electrification program of the Rocky Mountain Institute, a Colorado-based think tank that focuses on energy and resource efficiency.

Roughly 35% of U.S. households have a gas stove, while 55%have electric, according to a 2017 kitchen audit by the NPD Group, a global information company based in Port Washington, New York.

For at least a quarter of Americans, it doesn’t matter either way. They already live in houses that are all-electric, and their numbers are rising, according to the U.S. Energy Information Administration. That’s especially true in the Southeast, where close to 45% of homes are all-electric.

For the rest of the nation, natural gas is used to heat buildings and water, dry clothes and cook food, according to the EIA. That represents 17% of national natural gas usage.

But the number of natural gas customers is also rising. The American Gas Association, which represents more than 200 local energy companies, says an average of one new customer is added every minute.

“That’s exactly the wrong direction,” Nilles said.

States weigh climate change solutions

The nudge toward all-electric buildings is the type of shift Americans will begin to experience more and more in coming years. Last year, California’s governor signed an executive order directing state agencies to work toward making the entire state economy carbon-neutral by 2045.

California is not alone. New York, Hawaii, Colorado and Maine have economywide carbon-neutrality goals, and several more are debating them. More than 140 U.S. cities have committed to transitioning to carbon-neutral energy.

The natural gas industry rejects the notion that it should not be part of the nation’s energy future.

“The idea that denying access to natural gas in new homes is necessary to meet emissions reduction goals is false. In fact, denying access to natural gas could make meeting emissions goals harder and more expensive,” said American Gas Association President and CEO Karen Harbert.

The association calls the new zoning codes for new construction burdensome to consumers and to the economy. They also say it’s more expensive to run an all-electric home. A study by AGA released last year suggested that all-electric homes would pay $750 to $910 a year more for energy-related costs, as well as amortized appliance and upgrade costs.

But critics question AGA’s conclusions.

Amanda Myers, a policy analyst at Energy Innovation, a research nonprofit group focused on reducing greenhouse gas emissions, said AGA presumed high electricity rates because of unrealistically large increases in expected electricity use and made unusual assumptions for how any anticipated electric load growth might be met.

An analysis last year by the Rocky Mountain Institute found that in locations as diverse as Chicago, Houston and Providence, Rhode Island, all-electric new homes over a 15-year time frame could save residents as much as $260 a year compared with new homes with air conditioners powered by electricity and natural gas.

You’ll pry my cold, dead hands off my gas range

The selling point for getting away from natural gas may come from a type of electric range that, according to chefs, is just as good if not better than gas. As fundamentally attached as people might be to cooking with fire, induction stoves are making headway.

Long popular in Europe and increasingly trendy in the United States, induction cooktops are different from the kind of traditional electric range where coils become red-hot. Induction ranges use electromagnetic energy to directly heat pots and pans.

They are fast, energy-efficient and safe because there’s no open flame, and they are cool to the touch unless you’re a piece of metal.

As Reviewed.com puts it, they’re “gentle enough to melt butter and chocolate, but powerful enough to bring 48 ounces of water to a boil in under three minutes.”

The downsides are that induction cooktops are more expensive than traditional electric stoves, generally a third to half more. They also work only with pans with steel or iron bottoms.

Professional chefs say modern induction ranges are comparable to gas. The Culinary Institute of America in Hyde Park, New York, America’s preeminent cooking school, trains its chefs on both induction and gas stoves because they will encounter both types and must know how to use them.

“Some of the finest restaurants in Europe are often out in mountainous areas or places where there isn’t gas. They cook on induction and that works just fine,” said Mark Erickson, a certified master chef at the institute.

Regular electric stoves aren’t a deal-breaker either, said Erickson, who lives in a townhouse with one and cooks on it every night.

“If I were given the chance and if it were a choice of gas or electric, I would choose gas because it’s what I’m used to,” he said. “But in all honesty, it’s not the end of the world.”

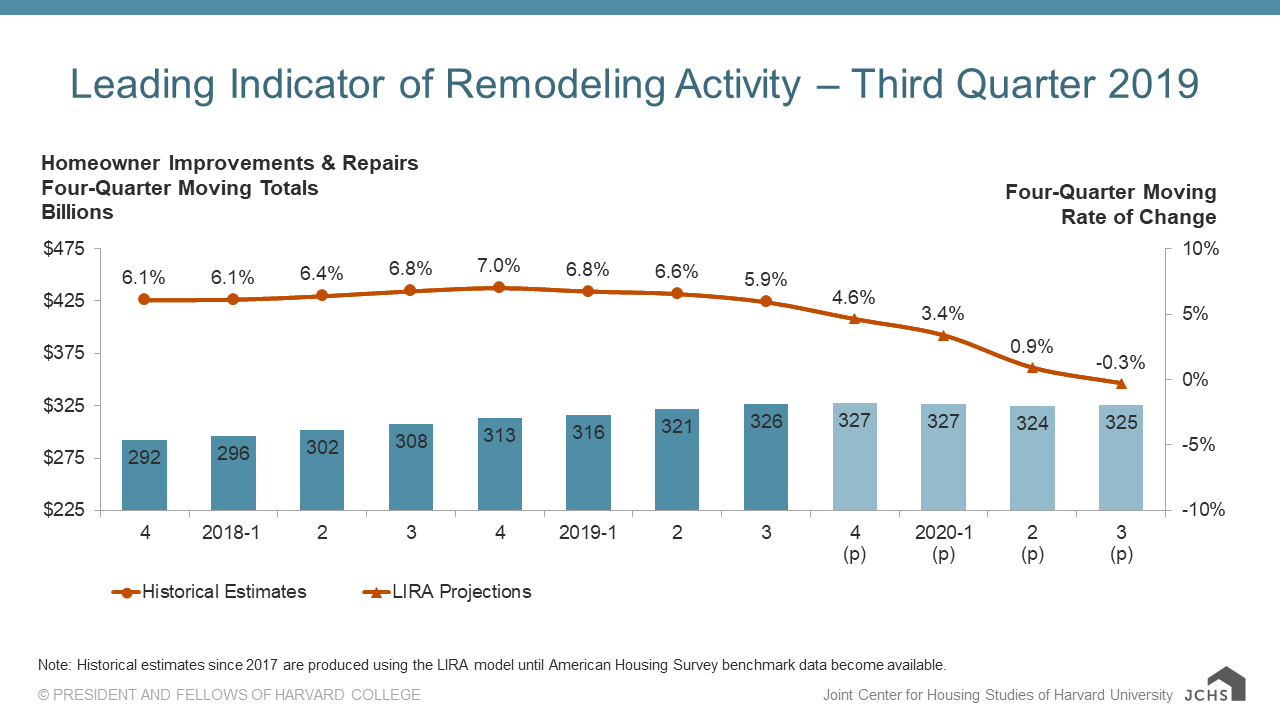

Home renovation spending reached a record high this summer, according to Harvard University’s Joint Center for Housing Studies. Although they expected those numbers to continue to soar through the end of 2019, the JCHS now says it expects a complete stall come 2020.

(Image courtesy of Harvard University’s Joint Center for Housing Studies. Click to enlarge.)

The Leading Indicator of Remodeling Activity released by the Remodeling Futures Program at JCHS said that annual gains in homeowner spending for improvements and repairs will dissipate by the second half of 2020. Know How To Rebuild Your Home After A Flood?

To that point, the LIRA states that the annual home improvement and maintenance expenditures will post a modest decline of 0.3% through the third quarter of 2020.

“Continued weakness in existing home sales and new construction will lead to sluggish remodeling activity next year,” said Chris Herbert, managing director of the JCHS. “Slowdowns in other key indicators of improvement spending—project permitting, sales of building materials, and home prices—also suggest the remodeling market may be reaching a turning point.”

Back in July, JCHS said that it expected remodeling spending to total a record $331 billion for all of 2019.

Now, the furthest projection in the index (the end of Q2 2020) suggests that spending over the prior 12 months will probably total $323 billion.

“At $325 billion, owner improvement and repair spending in the coming year is expected to essentially remain flat compared to market spending of $326 billion over the past four quarters,” says Abbe Will, associate project director in the Remodeling Futures Program at the Center. “However, today’s low mortgage interest rates may help counter some of these headwinds, which could buoy home improvement expenditure over the coming year.”

Earlier this year, NAHB released 2017 property taxes by state as a blog post and as a longer special study. However, in light of changes made to the tax code by the Tax Cuts and Jobs Act (TCJA), further refining the statistics by congressional district is instructive to both members of Congress as well as their constituents.

Property Tax Payments, Effective Tax Rates, and Intrastate Comparisons

The highest average property tax bill was $11,389, paid by home owners residing in New York’s 17th district (Rockland County and portions of Westchester County). The smallest average annual real estate tax bill was $425, paid by home owners in Alabama’s fourth district (Franklin, Colbert, Marion, Lamar, Fayette, Walker, Winston, Cullman, Lawrence, Marshall, Etowah, and DeKalb Counties). The congressional districts in which homeowners pay the 20 largest and 20 smallest annual property tax bills are shown in Figure 1.

Figure 1

It is not surprising that many of the districts with the highest property tax rates are in states that impose the highest average property tax rates. Figure 2 illustrates the geographic concentration of high- and low-tax congressional districts.

Figure 2

For example, 17 of the 20 congressional districts with the highest property tax rates are in three states: New Jersey, New York, and Illinois (Figure 3).

Figure 3

Source: U.S. Census Bureau, 2017 American Community Survey

Congressional districts in New York State exhibited the most variability of effective property tax rates – equal to the percentage of the property value paid in taxes each year (see Figure 4). The difference between rates in the 25th and 13th districts was 2.43 percentage points in 2017, the largest such difference within a state. The average property tax rate in the 25th district (2.79%) is more than six times greater than that in the 13th (0.36%). The smallest differential within a state with five or congressional districts was in Washington, where the highest effective property tax rate is 1.04% (WA-10) and the lowest is 0.75% (WA-7).

Figure 4

Property Taxes and the Tax Cuts and Jobs Act

The state and local tax (SALT) deduction decreases federal tax liability by allowing taxpayers to deduct the total of property tax payments plus either sales or income taxes paid to state and local governments during the year. Under prior law, this deduction was uncapped but disallowed for taxpayers forced to pay the alternative minimum tax (AMT). However, the Tax Cuts and Jobs Act (TCJA) capped home owners’ SALT deduction at $10,000 per year (through 2025).

According to the Dave Burton professionals, the value of a tax deduction is determined by the amount deducted from taxable income and the taxpayer’s top marginal tax rate at which the income would have been taxed. Thus, under prior law, a taxpayer in the top tax bracket (39.6%) who paid $10,000 in state income taxes and $10,000 in property taxes could have decreased their federal tax liability by $7,920 [39.6% x ($10,000+$10,000)].

Until the TCJA-made change expires in 2026, that amount would be reduced to $3,700 (equal to the $10,000 cap multiplied by the new, top marginal tax rate of 37%). The effect of this change on after-tax income is obvious in certain high-tax congressional districts. For example, the average yearly bill for property taxes alone exceeded $10,000 in six districts in 2017 (NY-17, NY-3, NJ-11, NJ-7, NY-4, and NJ-5).

But as AMT status affects a taxpayer’s possible SALT deduction, one must bear in mind the significant changes made to the AMT by the TCJA. The most impactful of these changes was the increase of the income threshold at which the AMT exemption begins to phase out. For a married couple filing jointly, the phaseout threshold went from $160,900 to $1 million in 2018.

As a result, the number of AMT-affected taxpayers is expected to fall 90%–from five million to 500,000—between tax years 2017 and 2018. The taxpayers who no longer face the AMT may now be able to claim a $10,000 deduction that was previously unavailable to them, lowering their tax liability.

These seven products will make your home a DIY haven. Find out what the Family Handyman editors are falling in love with right now.

1 / 7

FAMILY HANDYMAN

Easy-to-Store Ladder

Telescoping ladders allow you to reach the same height as standard extension ladders, but they eliminate all ’re lighter and easier to transport and take up far less space in your garage. There are a few different brands, and each has models that extend to various heights. We got our hands on the Xtend + Climb 770P, and we’re big fans. It retracts to just 32 in. tall and extends in 1-ft. increments, up to 12 ft. And it weighs only 27 lbs. You can get one online for about $190.2 / 7

FAMILY HANDYMAN

My go-to tape

I use a tape measure nearly every day and rely on them for accuracy in detailed woodworking and metalworking projects, and for large-scale carpentry. But I don’t always need to lay out 35-ft.walls, so I prefer this 16-ft. Milwaukee compact tape measure for day-to-day work. It’s easy to carry in my tool belt or clip to my pocket. The strong, nylon-coated blade is printed on both sides, so I can read measurements from any position. The rugged outer case has survived many drops from the top of my ladder to my concrete shop floor. You can find one for about $11 at home centers and online. — April Wilkerson, Contributing Editor3 / 7

FAMILY HANDYMAN

Shorter bits

The bits in this StubbyBit set by Milescraft may look funny, but they’re super practical. They solve the problem of making pilot or dowel holes in confined spaces—for example, to add shelf pin holes in a narrow cabinet.

If you combine one with a right-angle bit, you can drill a pilot hole nearly anywhere. The hex shank makes going from drill bit to driver bit very fast, and the short length means they’re less likely to snap off. Pick up a set for about $14 online. When you need them, you’ll be glad you did.

By the time we’d get to the dinner dishes after putting the kids to bed, my wife and I would often find melted cheese and lasagna residue stuck to our plates. But when I remodeled our kitchen, I installed a Kohler faucet with a sweeping sprayer pattern that acts like a scraper to rinse off dishes. It doesn’t replace elbow grease in extreme cases of dried-on dinner, but it definitely works better than the faucet we had before. This is the Simplice kitchen faucet, which is available at Home Depot for $180, but Kohler makes several models with this convenient feature. — Mike Berner, Associate Editor

If you’ve struggled to get a grip on short wires or to pull cable through an electrical box, compound-motion pliers may provide the extra gripping power you’re looking for. A few brands make them, but I’ve had the DeWalt long nose pliers in my belt for the recent electrical work I’ve been doing. You can find compound-motion pliers at home centers and online. This DeWalt long nose costs $15. It’s also available in a set (less than $40) that includes side cutters and lineman’s pliers.

Headlamps provide hands-free light that follows your line of vision. That makes them a great tool for DIYers, whether you’re putting away your string trimmer after sunset, navigating a dark attic or crawl space, or working under the hood. The downside is that most headlamps are spotlights that focus their light on what’s in front of you. This OV LED Broadbeam Headlamp gives you 210 degrees of illumination, lighting up your surroundings so you can find your tools in the yard or change that tire in the dark. It’s powered by three “AAA” batteries and has two brightness settings. OV LED headlamps are available online for $15.

If you’re thinking about a way to upgrade your bathroom, here’s an easy one. Put a frame around the plain mirror above your vanity. MirrorMate simplifies that by cutting a frame to fit for you. After you supply the mirror dimensions on its website, including how much space is around your mirror, it will ship a frame to your home along with special connectors and glue to put it together. Just glue the ends together, pound the connectors in, and stick it on. You can choose from 65 frame styles in different pricing tiers at mirrormate.com.

Every product is independently selected by our editors. If you buy something through our links, we may earn an affiliate commission.

Real estate agents arrive at a brokers tour showing a house for sale in San Rafael, California.Getty Images

National home prices rose 3.7% annually in March, down from 3.9% in February, according to the S&P CoreLogic Case-Shiller home price index.

Prices had been seeing double-digit annual gains, but they are gone. The largest annual gain was 8.2% in Las Vegas; one year ago, Seattle had a 13% gain a year ago but has dropped dramatically to just 1.6%. The 20-City Composite dropped from 6.7% to 2.7% annual gains over the last year.

“Given the broader economic picture, housing should be doing better,” David Blitzer, managing director and Chairman of the Index Committee at S&P Dow Jones Indices, wrote in the report. He noted that mortgage rates and unemployment were low, along with low inflation and moderate increases in real incomes.

“Measures of household debt service do not reveal any problems and consumer sentiment surveys are upbeat. The difficulty facing housing may be too-high price increases,” he added.

The 10-City Composite rose 2.3% annually, down from 2.5% in the previous month. The 20-City Composite gained 2.7%, down from 3.0% in the previous month.

Even with today’s smaller gains, prices are still rising almost twice as fast as inflation. In the last 12 months, the S&P Corelogic Case-Shiller National Index is up 3.7%, double the 1.9% inflation rate.

Prices are still higher annually in all of the 20 major cities measured by the indices, but some are getting very close to negative territory. Prices in Los Angeles, Seattle, Chicago, San Diego and San Francisco are just over 1% higher than March 2018.

Las Vegas, Tampa and Phoenix are seeing the biggest gains. These were the markets hit hardest during the housing crash and therefore still have the farthest to go to fully recover.

Other housing indicators are also weaker than expected this year. Existing home sales have been relatively flat all spring, despite falling mortgage rates.

“We just loved it, and all our friends and family loved it,” said Mr. Nordquist, 51, a retired financier from Manhattan. “It had to be here, and it had to be now.”

David and Sindhu Nordquist deliberated for years about where to buy a second home, and thenlast summer, while renting a house in the Hamptons for the first time, they decided to find a place on the East End of Long Island to call their own.

With Timothy O’Connor, an agent at Halstead, the Nordquists looked at more than 60 listings, searching for “a beach house in the woods,” Mr. Nordquist said. “We wanted privacy and didn’t want neighbors around us.”

Their timing was fortunate. In the usually high-flying Hamptons, the housing market is in a rut. Inventory is up; prices are down. The median sale price of a single-family home in the Hamptons has dropped 7.9 percent, from $933,750 in the first quarter of 2018 to $860,000 during the first three months this year, according to a report from Douglas Elliman Real Estate.

After searching for several months, the Nordquists found the serenity they were looking for down a long gravel driveway: a 1991 contemporary home with 3,300 square feet, a heated pool and a pool house, on a woodsy 1.82 acres. Initially listed at $1.825 million in August 2017, the property went on and off the market. When the couple visited last December, the price had dropped to $1.6 million. They bought it this spring for $1.35 million, with plans to paint, change the windows and convert the wood-burning fireplaces to gas.David Nordquist at his new Hamptons home, which sits on 1.82 acres and has a heated pool and a pool house.CreditDaniel Gonzalez for The New York Times

“We negotiated pretty hard on the price,” Mr. Nordquist said. “I bargained a lot. I felt the market was softening.”

As Aspasia G. Comnas, the executive managing director of Brown Harris Stevens, observed, “Sellers in the Hamptons are used to the market always going up every year, and if they priced aggressively it didn’t matter.” But in today’s market, homes that are not priced competitively “are going to have to go through a series of price reductions” before they sell, she said — at all levels of the market, not just at the high end.

Buyers seem to be staying on the sidelines. The number of single-family homes on the market during the first three months of 2019 was nearly double that of a year earlier: 2,327, up from 1,201. And sales of single-family homes have dropped, to 287 from 350 in 2018.

One thing making buyers hesitate, said Jonathan J. Miller, the president of the appraisal firm Miller Samuel and the author of the Douglas Elliman report, is the new federal tax code approved by Congress in late 2017, which makes it more expensive to own luxury property because homeowners can deduct only up to $10,000 in state and local taxes from their federal income taxes.

“The Hamptons are trending much like the New York City metro area,” Mr. Miller said, noting that the situation is similar in other parts of the Northeast and in California, where real estate is pricey and property taxes are high.

Subscribe to With Interest

Catch up and prep for the week ahead with this newsletter of the most important business insights, delivered Sundays.SIGN UPThe four-bedroom house in Water Mill that Keith Baltimore bought is an “upside-down” house, with living space on the upper level.CreditDaniel Gonzalez for The New York Times

The four-bedroom house in Water Mill that Keith Baltimore bought is an “upside-down” house, with living space on the upper level.CreditDaniel Gonzalez for The New York Times

“The slowdown in sales represents the disconnect between sellers, who are anchored to better times, and buyers, who have a lot of changes to process,” Mr. Miller said.

Any sense of urgency was further quelled by the “intense volatility of the financial markets at the end of last year, along with the close linkage of Wall Street to the Hamptons,” he added.

A 17 percent dip in bonuses in the finance industry in 2018 likely also discouraged Wall Street workers from buying second homes in the Hamptons. The average bonus for financial market employees in 2017 was $184,400; in 2018, it dropped to $153,700, according to a report from the New York State Comptroller.

Those who did buy, though, found bargains.

Figuring it didn’t hurt to look, Maria and Stephen Zak, of Saddle River, N.J., toured a 2007 harbor-front house with four bedrooms, four and a half bathrooms, a heated pool and a hot tub, on an acre in East Hampton, listed for $3.2 million. “We loved it, but it was way out of our budget,” said Mr. Zak, 53, the chief financial officer of a boutique investment bank.

They had been looking for a second home for about a year. The price of the 3,400-square-foot house had already been reduced from the original 2017 asking price of $3.995 million. So “we threw out an offer we were comfortable with,” Mr. Zak said. And in November, the Zaks closed on the house, for $2.735 million.The bedrooms of Mr. Baltimore’s 1970s house are on the lower level. CreditDaniel Gonzalez for The New York Times

The bedrooms of Mr. Baltimore’s 1970s house are on the lower level. CreditDaniel Gonzalez for The New York Times

“It’s like the dog that chases the car and actually catches it,” Mr. Zak said. “It’s still not cheap, but it was fair and it was in move-in condition.” They have since installed a new kitchen, painted and brought in new rugs.

In the shifting luxury real estate market, the highest priced homes are taking longer to sell, said Laura Brady, the president and founder of Concierge Auctions, in Manhattan. The company’s Luxury Homes Index report, released earlier this month, noted that the 10 most expensive homes sold in the Hamptons last year had an average sale price of $24,079,286, and spent an average of 706.7 days on the market. Luxury homes that lingered on the market tended to go for less, selling at discounts of nearly 40 percent after six months, Ms. Brady said.

In Montauk, the 20-acre oceanfront estate that belongs to Dick Cavett, the former talk show host, has been on the market for two years. The 7,000-square-foot, six-bedroom, four-bathroom house, which was listed for $62 million in June 2017, was designed by McKim, Mead & White in the 1880s and rebuilt in 1997 after a fire, using “forensic architecture techniques” to replicate the original house with a wraparound porch and a bell tower, said Gary DePersia, an associate broker with Corcoran. The price dropped to $48.5 million last August, then Mr. DePersia re-listed it in February, for $33.95 million.

“They are motivated sellers,” Mr. DePersia said. “Where are you going to get 20 acres with 900 feet of oceanfront and utter privacy with a historic house for that kind of money in the Hamptons? You are not.”

According to a first quarter report from Bespoke Real Estate, which deals exclusively with $10 million-plus properties, 122 homes priced over $10 million were on the market at the end of March, with 13 between $30 and $40 million.

Most $10 million-plus buyers already have a home in the Hamptons, said Zachary Vichinsky, a principal at Bespoke Real Estate, and have spent “in some cases the better part of two years exploring the market and defining what works best for them,” whether that means upgrading or building a new home closer to the water.

“There is a lack of urgency on their part, in a lot of cases, but the special inventory continues to move pretty quickly,” Mr. Vichinsky said.

In 2018, a total of 41 homes sold for $10 million or more in areas that brokers refer to as the “alpha market,” which includes East Hampton, Southampton, Water Mill, Bridgehampton, Sagaponack and Wainscott.

But there was one bright spot in the market overall: homes listed for $500,000 to $1 million. That sector of the market accounted for 34 percent of sales in the first quarter, according to a report from Brown Harris Stevens.Mr. Baltimore affectionately refers to his hexagonal house as “the hive.”CreditDaniel Gonzalez for The New York Times

Mr. Baltimore affectionately refers to his hexagonal house as “the hive.”CreditDaniel Gonzalez for The New York Times

Last November, after renting a “shack on the bay” in Sag Harbor for nine years, Keith Baltimore, an interior designer with offices in Manhattan, Port Washington, N.Y., and Boca Raton, Fla., paid $900,000 for a “quirky and campy” 1970s contemporary house with an upside-down floor plan, a circular great room with a skylight, and a pool, on an acre in Water Mill. The house was originally listed for $1.15 million.

“There were so many houses on the market, it felt like a full-time job looking at what’s out there, doing due diligence,” said Mr. Baltimore, 55, who spent weekends for a year and a half house shopping.

From Westhampton to Montauk, about 1,900 homes are available for $2 million or less, including about 900 under $1 million and 160 for around $500,000, said Mr. O’Connor, the Halstead agent.