Pending home sales decreased in June, following a slight increase in May, according to the National Association of REALTORS®. All four major regions posted month-over-month and year-over-year pullbacks, the largest of which occurred in the West.

The Pending Home Sales Index (PHSI),* www.nar.realtor/pending-home-sales, a forward-looking indicator of home sales based on contract signings, dipped 8.6% to 91.0 in June. Year-over-year, transactions shrank 20.0%. An index of 100 is equal to the level of contract activity in 2001.

“Contract signings to buy a home will keep tumbling down as long as mortgage rates keep climbing, as has happened this year to date,” said NAR Chief Economist Lawrence Yun. “There are indications that mortgage rates may be topping or very close to a cyclical high in July. If so, pending contracts should also begin to stabilize.”

According to NAR, buying a home in June was about 80% more expensive than in June 2019. Nearly a quarter of buyers who purchased a home three years ago would be unable to do so now because they no longer earn the qualifying income to buy a median-priced home today.

“Home sales will be down by 13% in 2022, according to our latest projection,” Yun added. “With mortgage rates expected to stabilize near 6% and steady job creation, home sales should start to rise by early 2023.”

June Pending Home Sales Regional Breakdown

The Northeast PHSI slid 6.7% compared to last month to 80.9, down 17.6% from June 2021. The Midwest index dropped 3.8% to 93.7 in June, a 13.4% decline from a year ago.

The South PHSI slipped 8.9% to 108.3 in June, a decrease of 19.2% from the previous year. The West index slumped 15.9% in June to 68.7, down 30.9% from June 2021.

The National Association of REALTORS® is America’s largest trade association, representing more than 1.5 million members involved in all aspects of the residential and commercial real estate industries.

# # #

*The Pending Home Sales Index is a leading indicator for the housing sector, based on pending sales of existing homes. A sale is listed as pending when the contract has been signed but the transaction has not closed, though the sale usually is finalized within one or two months of signing.

Pending contracts are good early indicators of upcoming sales closings. However, the amount of time between pending contracts and completed sales is not identical for all home sales. Variations in the length of the process from pending contract to closed sale can be caused by issues such as buyer difficulties with obtaining mortgage financing, home inspection problems, or appraisal issues.

The index is based on a sample that covers about 40% of multiple listing service data each month. In developing the model for the index, it was demonstrated that the level of monthly sales-contract activity parallels the level of closed existing-home sales in the following two months.

An index of 100 is equal to the average level of contract activity during 2001, which was the first year to be examined. By coincidence, the volume of existing-home sales in 2001 fell within the range of 5.0 to 5.5 million, which is considered normal for the current U.S. population.NOTE: Existing-Home Sales for July will be reported on August 18. The next Pending Home Sales Index will be on August 24. All release times are 10 a.m. Eastern.

“Mortgage rates remain at record lows, resisting their typical correlation to Treasury yields, which have recently been moving higher,” said Sam Khater, Freddie Mac’s Chief Economist. “Mortgage spreads – the difference between mortgage rates and the 10-year Treasury rate – are declining from their elevated levels earlier this year. Although today’s mortgage spread is about 1.8 percent and still has some room to move down if the 10-year Treasury continues to rise, it’s encouraging to see that the spread is almost back to normal levels.”

News Facts

30-year fixed-rate mortgage averaged 2.71 percent with an average 0.7 point for the week ending December 10, 2020, unchanged from last week. A year ago at this time, the 30-year FRM averaged 3.73 percent.

15-year fixed-rate mortgage averaged 2.26 percent with an average 0.6 point, unchanged from last week. A year ago at this time, the 15-year FRM averaged 3.19 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.79 percent with an average 0.3 point, down from last week when it averaged 2.86 percent. A year ago at this time, the 5-year ARM averaged 3.36 percent.

The PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit. Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

By Na Zhao, Ph.DNAHB Economics and Housing Policy GroupReport available to the public as a courtesy of HousingEconomics.com

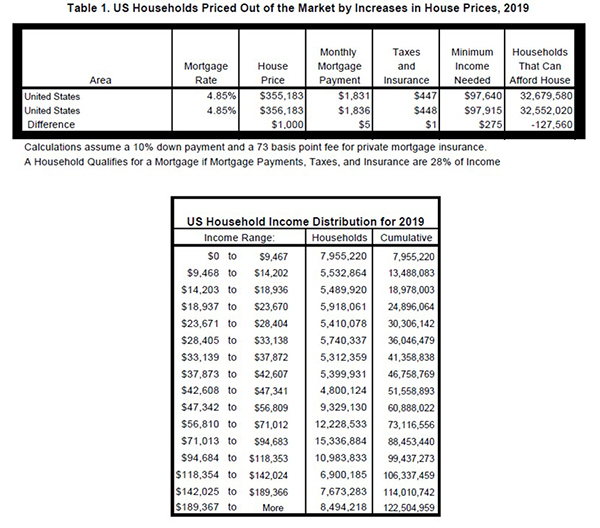

This article announces NAHB’s “priced out estimates” for 2019, showing how higher home prices and interest rates affect housing affordability. The 2019 U.S. estimates indicate that a $1,000 increase in the median new home price would price 127,560 U.S. households out of the market. In other words, 127,560 households would qualify for the new home mortgage before the change, but not afterwards. Similarly, 25 basis points added to the current mortgage rate would price out around 1 million households. The article also includes priced out estimates for individual states and more than 300 metropolitan areas.

The Priced Out Methodology and Data

The NAHB Priced Out model uses the ability to qualify a mortgage to measure housing affordability, because most home buyers finance their new home purchase with conventional loans, [1] and because convenient underwriting standards for these loans exist. The standard NAHB adopts for its priced-out estimates is that the sum of the mortgage payment (including the principal amount, loan interest, property tax, homeowners’ property and private mortgage insurance premiums (PITI), is no more than 28 percent of monthly gross household income.

As a result the number of households that qualify for mortgages for a certain priced home depends on the household income distribution in an area and the mortgage interest rate at that time. The most recent detailed household income distributions for all states and metro areas are from the 2017 American Community Survey (ACS). NAHB adjusts the income distributions to reflect the income and population changes that may happen from 2017 to 2019. The income distribution is adjusted for inflation using the 2018 median family income published by the Department of Housing and Urban Development (HUD) for all states and metro areas, and then extrapolated it into 2019. The number of households in 2019 is projected by the growth rate of households from 2016 to 2017.

The assumptions of the priced out calculation include a 10% s down payment and a 30-year fixed rate mortgage, at an interest rate of 4.85%. For a loan with this down payment, private mortgage insurance is required by lenders and also included as part of PITI. The typical private mortgage insurance annual premium is 73 basis points[2], based on the standard assumption of national median credit score of 738[3] and 10% down payment and 30-year fixed mortgage rate. Effective local property tax rates are calculated using data from the 2017 American Community Survey (ACS) summary files. Homeowner’s insurance rates are constructed from the 2016 ACS Public Use Microdata Sample (PUMS).[4] According to Brisbane property valuers, for the U.S. as a whole, the property tax is $12 per $1,000 of property value and the homeowner insurance is $4 per $1,000 property value.

Under these assumptions, 32.7 million of the 122.5 million U.S. households could afford to buy a new median priced home at $355,183 in 2019. A $1,000 home price increase thus would price 127,560 households out of the market for this home. These are the households that can qualify for a mortgage before a $1,000 increase but not afterwards, as shown in Table 1 below.

State and Local Estimates

The number of priced out households varies across both states and metropolitan areas, largely affected by the sizes of local population and the affordability of new homes. The 2019 priced-out estimates for all states and the District of Columbia are shown in Table 2 (available in the Additional Resources box), which presents the projected 2019 median new home price and the amount of income needed to qualify the mortgage, and the number of households could be priced out if price goes up by $1,000. Among all the states, Texas registered the largest number of households priced out of the market by a $1,000 increase in the median-priced home in the state (11,152), followed by California (9,897), and Ohio (7,341).

Table 3, which is available in the Additional Resources box, shows the 2019 priced-out estimates for 382 metropolitan statistical areas. The metropolitan area with the largest priced out effect, in terms of absolute numbers, is Chicago-Naperville-Elgin, IL-IN-WI, where 4,499 households are squeezed out of the market for a new median-priced home if price increases by $1,000. This is largely because Chicago is a populous metropolitan area with a large number of households; and, compared to the largest metropolitan areas on the East and West costs, the median priced home is more affordable to begin with. Around 27% of households there are capable of buying new median-priced homes. For similar reasons, Houston-The Woodlands-Sugar Land, TX metro area, where nearly 33% of households can afford median-priced new homes.to begin with, registered the second largest number of priced out households (3,546), where nearly 33% of households can afford median-priced new homes. In New York-Newark-Jersey City, NY-NJ-PA, 3,531 households are squeezed out of the housing market for a new median-priced home if price increases by $1,000. Compared to Chicago or Houston, the median-priced new home is affordable to a smaller share of the households in New York, but New York is the largest metro area by population size with over 7 million households.

Interest Rates

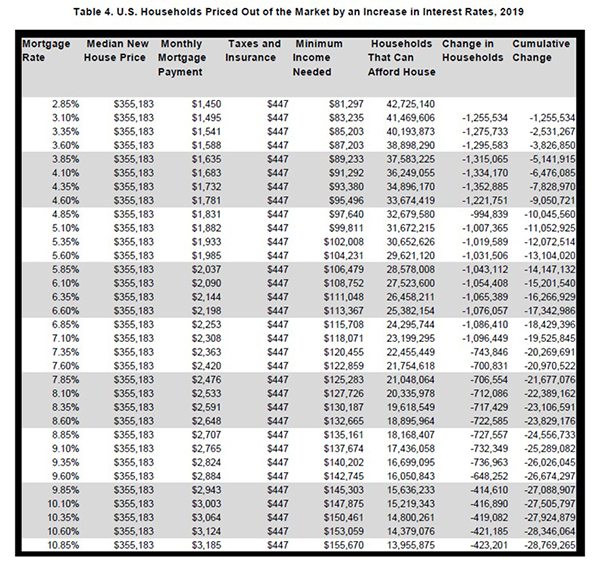

The NAHB 2019 priced-out estimates also present how interest rates affect the number of households would be priced out of the new home market. If the mortgage interest rate goes up, the monthly mortgage payments will increase as well and therefore higher household income thresholds to qualify a mortgage loan. Table 4 shows the number of households priced out of the market for a new median priced home at $355,183 by each 25 basis-point increase in interest rate from 2.85% to 10.85%. When interest rates goes up from 2.85% to 3.10%, around 1.26 million households could no longer afford buying median-priced new homes. An increase from 4.85% to 5.10% could price approximately one million households out of the market. However, about 423,000 households would be squeezed out of the market if interest rate goes up to 10.85% from 10.6%. This diminishing effects happen because only a few households at the thinner end of household income distribution will be affected. On the contrary, when interest rates are relatively low, 25 basis-point increase would affect a larger number of households at the thicker part of income distribution.

Footnotes[1]According to the 2017 American Housing Survey (funded by HUD and conducted by the Census Bureau), 74 percent of the home buyers who moved into their homes in 2016 or 2017 had a regular primary mortgage on the home.[2]Private mortgage insurance premium (PMI) is obtained from the PMI Cost Calculator( https://www.hsh.com/calc-pmionly.html)[3]Median credit score information is shown in the article “Four ways today’s high home prices affect the larger economy” October 2018 Urban Institute https://www.urban.org/urban-wire/four-ways-todays-high-home-prices-affect-larger-economy[4]Producing metro level estimates from the ACS PUMS involves aggregating Public Use Microdata Area (PUMA) level data according to the latest definitions of metropolitan areas. Due to complexity of these procedures and since metro level insurance rates tend to remain stable over time, NAHB revises these estimates only periodically.

Ranjit Sharma is a custom home builder, who specializes in upscale houses with fine trim and old world woodwork.

His company has been on a tear the past five years, thanks to the soaring housing market.

But he now worries about rising prices from tariffs on Canadian lumber that have sent the price of the beams, joists, and other wood he uses up almost 10 percent this year.

“Everything from the framing to the roofing to the interior trim,” he said,” has had price hikes.”

Reasons for price hikes

It’s not just tariffs causing the price spike: Western wildfires and last year’s hurricanes in Texas and Florida are also causing many of Sharma’s suppliers to raise prices on materials like drywall.

“We have also seen prices on steel, drywall, flooring, concrete, and just about everything go up,” he said.

And these soaring prices can impact you not only if you are building a new home, but even if you are just rehabbing your kitchen, or replacing your back deck.

Not just home builders affected

Outside a Home Depot store in Deerfield Township, Jack Allen was loading supplies to build a deck and fence.

He says the price of cedar, that he was hoping to use for the fence, has almost doubled in the past year.

“Can’t afford a cedar fence any longer. Each picket is about $4, and there are two pickets every one foot.”

As a result, he’s downgrading to cheaper pressure treated lumber, which will lower his fence cost by a third.

For now, builder Ranjit Sharma is not passing along the price hikes to his home buyers. But he may soon because it’s about to cost him $5,000 – $10,000 more for each house he builds.

What can you do if you are planning a construction project? Builders suggest that cash-strapped homeowners:

Ask about cheaper wood, if you are using cedar or other woods that have spiked in price.

Downside the project (in other words, reduce the size of that deck).

Consider wood-look laminate flooring instead of real wood.

Baby Boomers are staying put and their kids are sticking with them.

A study released Thursday by Trulia examined the housing situations of homeowners 65 and older and compared it with a decade ago.

It uncovered a 3.4% jump in the number of seniors working in 2016 compared with 2005, and a 1.7% increase in the number living with younger generations.

It also showed that seniors appear to be holding off on downsizing just the same as they were 10 years prior.

Only 5.5% of seniors moved,according to Trulia, and of those who did, the split was pretty even between single-family and multifamily residences.

But Trulia analyst Alexandra Lee points out that while the percentage of downsizers hasn’t changed, the number of those moving actually has.

“Because the Boomer generation is so much larger than previous generations, that 5.5% moving rate translates into very different raw numbers across the years,” Lee wrote. “There were about 7 million more senior households in 2016 than 2005, meaning 386,000 more senior households moved in 2016.”

The age at which seniors decide to downsize has also shifted. The survey revealed that in 2005, seniors were moving into multifamily residences by age 75. By 2016, this had moved to 80.

The study sought to examine whether Baby Boomers holding onto their homes was driving up home prices. In looking at the nation’s top 100 metros, it determined that Boomers were not eroding affordability.

“Like the general population, seniors in expensive and unaffordable metros rent at much higher rates,” Lee wrote. “The higher the income required to purchase the median home, the lower the proportion of senior households that could downsize.”

Houseplants can improve your life in many ways (more on that later), but if you’re expecting that peace lily on your desk to rid your home of toxins, you’re in for a surprise.

A 1989 NASA study attempted to find new ways to clean the air in space stations. Despite some pretty neat findings, it never claimed houseplants are great at removing chemicals from your home’s air — although countless articles have since cited the study as proof of that point.

And the headline “Houseplants Remove Toxins” does sound a lot more exciting than the report’s actual statement:

“Low-light-requiring houseplants, along with activated carbon plant filters, have demonstrated the potential for improving indoor air quality by removing trace organic pollutants from the air in energy-efficient buildings.”

And if you thought that was a buzzkill, the paper’s summary continues to disappoint:

“Activated carbon filters containing fans have the capacity for rapidly filtering large volumes of polluted air and should be considered an integral part of any plan using houseplants for solving indoor air pollution problems.”

In other words, even if your dracaena had the potential to remove trace toxins from your energy-efficient home, you’d still need to recreate NASA’s complicated system, which blows air through the activated carbon in the plant’s root zone.

Furthermore, if you see a list of the best plants for removing toxins, it’s nothing more than a list of the plants used in the study.

So can houseplants purify my air or not?

In theory, yes. But if you’re thinking of making your own botanical air filtration system, you’ve got a lot of work to do.

As an EPA reviewer explained in 1992, “To achieve the same pollutant removal rate reached in the NASA chamber study,” you would need “680 plants in a typical house.”

You’d be better off buying an actual air filtration system or, at the very least, vacuuming more often.

Yes, it’s true that some plants in the NASA list were more effective at removing benzene, trichloroethylene, and/or formaldehyde than others, but the amount is so negligible that neither the American Lung Association nor the EPA recommends using houseplants to improve your air.

Taking it a step further, both organizations warn that houseplants can worsen your air quality, introducing bacteria that grows in damp potting mix or pesticides used by the nursery. Stacey reviewed baby air purifiers and noticed that this danger was mentioned quite a lot. It is like most things in life, do it well and you get the benefits, do it poorly and reap in hidden problems and complications. Plants are great, but they need to be maintained just like everything else.

Don’t let that discourage you from indoor gardening, though. If you’re that worried about your air quality, you’d never step outside in the first place.

In any case, here’s how to keep your houseplants squeaky clean:

Dust those leaves! While you’re at it, dust the house.

Keep potting mix in its place with an ornamental mulch of river rocks or gravel.

Avoid using pesticides whenever possible.

Place saucers under each plant to catch excess potting mix.

To prevent mold, water plants only when the top half inch of the potting mix is dry.

Remove any diseased, yellowed, damaged, or fallen leaves.

Grow houseplants for happiness

True story: I once grew over a hundred plants in my tiny apartment, and I can attest that there was nothing clean about the experience – at all.

Dust filled the air, tree frogs and lizards leaped out of the foliage, and some plants even had stinky fertilizers in the potting mix. Those plants may not have made my air any cleaner, but cultivating a rainforest in the comfort of my home definitely made me a happier person.

Houseplants are a lot more exciting than you’d think. I was actually excited to wake up every morning, because each day brought the promise of a fresh new leaf, a different flower to admire, or another thick orchid root to mist with water.

Helping these living plants grow and thrive gave me a sense of purpose and a connection to the natural world. They also made me sneeze, but only because I spilled potting mix on the floor fairly often.

The only reason you need to grow a houseplant is to be happy. There are, of course, studies suggesting that living with plants improves your concentration, calmness, and productivity, but there’s no point in proving what we already know.

Nobody would bother growing houseplants if they didn’t make us happy.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing average fixed mortgage rates moving lower for the first time in ten weeks.

News Facts

30-year fixed-rate mortgage (FRM) averaged 4.20 percent with an average 0.5 point for the week ending January 5, 2017, down from last week when it averaged 4.32 percent. A year ago at this time, the 30-year FRM averaged 3.97 percent.

15-year FRM this week averaged 3.44 percent with an average 0.5 point, down from last week when it averaged 3.55 percent. A year ago at this time, the 15-year FRM averaged 3.26 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Quote Attributed to Sean Becketti, chief economist, Freddie Mac.

“The 30-year mortgage rate fell this week for the first time since the presidential election, dropping 12 basis points to 4.20 percent. This marks the first time since 2014 that mortgage rates opened the year above 4 percent. Despite this week’s breather, the 66-basis point increase in the mortgage rate since November 3 is taking its toll — the MBA’s refinance index plunged 22 percent this week.”

Before beginning the hunt for their first house, Tennessee residents Brittany and Craig Murphy pared their student debt, saved for a down payment and got an income boost from her new job. The major hurdle was what came next.

In the last month, the couple lost two bidding wars on Nashville homes to competitors willing to pay more than 10 percent above the asking price.

“I was not expecting the actual finding of the house to be the difficult part,” said Brittany Murphy, a 26-year-old Web designer whose husband, 27, is a software developer.

Steady job growth, low mortgage rates and record apartment rents are turning millennials like the Murphys into homebuyers — if they can find a house. As the key U.S. spring sales season gets under way, robust real estate demand is being outweighed by a persistent lack of lower-priced supply that’s poised to limit transactions and worsen an affordability crunch for young people. They’re faring worse than purchasers at the higher end of the market, where inventory is piling up.

Rising interest in home tours indicates prospective buyers are coming out in droves. An index by Redfin that measures requests for property visits rose in the first two months of the year to the highest level since at least 2012, when the data began.

“As soon as a house hits the market, it will be eaten by the huge demand appetite,” said Nela Richardson, Redfin’s chief economist.

Limited Inventory

Surging homebuying interest won’t necessarily translate into a big jump in sales. Prices will rise while limited inventory will put a cap on transactions, said Doug Duncan, chief economist of Fannie Mae. He estimates that U.S. single-family home prices will climb 5 percent this year, about the same as in 2015, while sales will increase 3 percent. That’s a slowdown from 2015, when existing-home purchases jumped 7 percent.

“Affordability is a challenge this spring,” Duncan said. Prospective buyers “would have gotten their credit in shape and they’ll have a job. But they will be frustrated because, in their market, there simply won’t be affordable homes.”

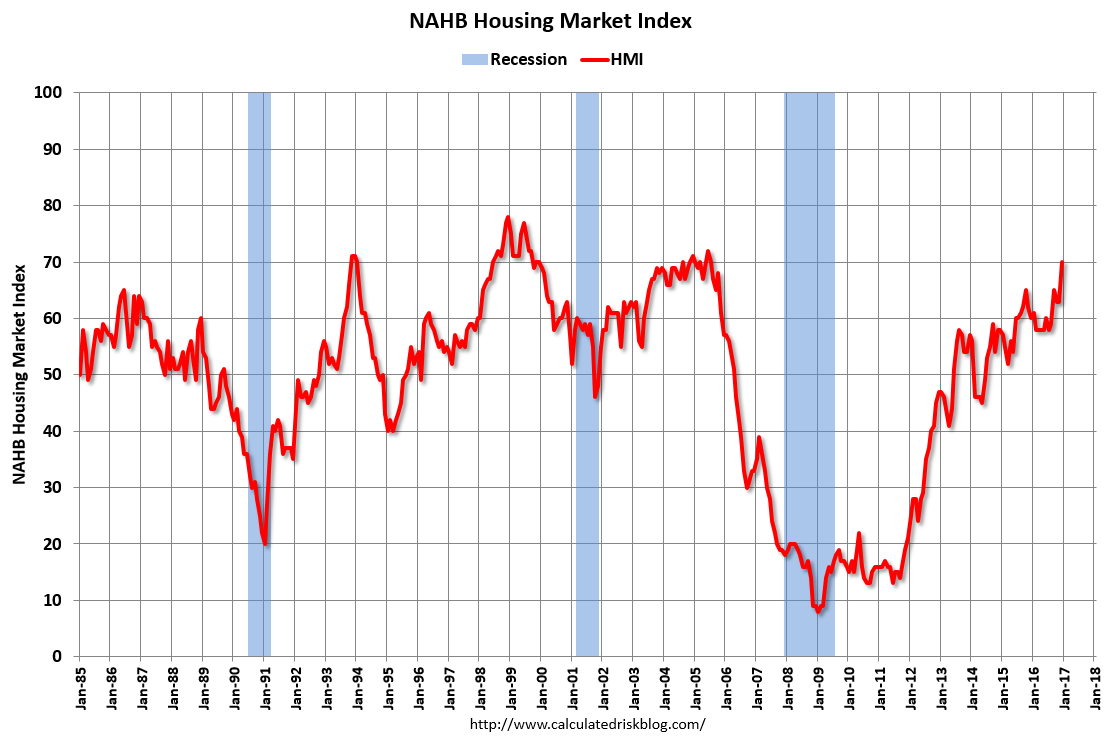

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 70 in December, up from 63 in November. Any number above 50 indicates that more builders view sales conditions as good than poor.

Builder confidence in the market for newly-built single-family homes jumped seven points to a level of 70 on the National Association of Home Builders/Wells Fargo Housing Market Index (HMI). This is the highest reading since July 2005. … “Though this significant increase in builder confidence could be considered an outlier, the fact remains that the economic fundamentals continue to look good for housing,” said NAHB Chief Economist Robert Dietz. “The rise in the HMI is consistent with recent gains for the stock market and consumer confidence. At the same time, builders remain sensitive to rising mortgage rates and continue to deal with shortages of lots and labor.” … All three HMI components posted healthy gains in December. The component gauging current sales conditions increased seven points to 76 while the index charting sales expectations in the next six months jumped nine points to 78. Meanwhile, the component measuring buyer traffic rose six points to 53, marking the first time this gauge has topped 50 since October 2005.

Looking at the three-month moving averages for regional HMI scores, the Northeast rose six points to 51, the Midwest posted a three-point gain to 61, the South rose one point to 67 and the West registered a two-point gain to 79.

Total housing starts expanded 9.8% month over month in June, reaching a 1.174 million annual starts pace, which was led by a surge in multifamily development.

Single-family starts were effectively flat, recording a 0.9% monthly decline to a 685,000 seasonally adjusted annual rate but were up 14.7% year over year. As measured on a three-month moving average, the pace of single-family starts hit a post-recession high in June. Looking forward, single-family permits were up 0.9% for June and 6% year-over-year, reaching a 687,000 annual rate. Regionally, single-family starts were up 6.8% for the month in the South, but down 27.3% in the Northeast, 7.1% in the West, and 4% in the Midwest.

Pointing to future growth, the July NAHB/Wells Fargo Housing Market Index reached 60 in July, which is the highest level since November 2005. Two of its three components also rose to levels last seen in late 2005. The index of current sales rose one point from the June level to 66, the highest in 10 years. The index for expected sales rose two points from June’s 69 to 71, also the highest in almost 10 years. The index for traffic fell one point to 43 from the six-month high in June of 44.

And more good news from June: The National Association of Realtors measure of existing home salesexisting home sales increased 3.2%, reaching the highest level since February 2007. Given that most new home sales are to move-up buyers, a rise in the volume of existing sales bodes well for additional single-family construction. Inventory of resale homes continues to be limited, falling to a five-month supply in June as the current sales rate.

However, the standout of the June housing starts report was multifamily construction, which for units in buildings with five or more units climbed to a 476,000 annual rate with a 28.6% monthly growth rate. Permits also expanded greatly, jumping 16.1% to a 621,000 annual rate. NAHB expects this level of apartment development to cool in the coming months.

On the supply side of the market, the most recent Producer Price Index data from the BLS revealed a small increase for wood products in June after trending down for the start of 2015. Softwood lumber prices rose 1% for the month but are down 9.1% from a recent high in September 2014. Prices for OSB rose 2.4% in June after a 20.4% slide that followed the collapse in prices that ended in July 2013. Gypsum prices slipped 1.5% in June after being flat in May, increasing to 5.3% the retreat from a February peak.