Pending home sales declined slightly in November on an annualized basis for the eleventh straight month. The Pending Home Sales Index decreased by 0.7% from 102.1 in October to 101.4 in November, and was 7.7% below the level one year ago. The Pending Home Sales Index (PHSI) is a forward-looking indicator based on signed contracts reported by the National Association of Realtors (NAR).

According to NAR, the decline in PHSI may not fully capture the current situation, as it did not reflect the impact of recent favorable conditions mortgage rates. But the housing market has been slowing down this year due to rising mortgage rates.

The PHSI increased 2.7% and 2.8% in the Northeast and West, but decreased 2.3% and 2.7% in the Midwest and South. Year-over-year, the PHSI declined in all regions, ranging from a decline of 3.5% in the Northeast to a decrease of 12.2% in the West. NAR stated that the annual drop in the West may be explained by the growing concerns of affordability due to rapidly increasing home prices in the region.

Existing sales slightly increased in November, but builder confidence fell in December to its lowest value since May 2015 as concerns over housing affordability persist. However, NAR anticipates a solid long-term prospect for home sales, as the current home sales level matches sales in 2000 while more jobs are created now compared to the early 2000’s.

HAVANA — Rafael Álvarez was up at 6:30 a.m. to warm milk for his baby daughter when he heard the sound of pebbles falling.

“That’s when the floor below us came loose. We were left hanging in the air, then fell into the abyss.”

Álvarez, 41, a baker, was buried in rubble to his waist. His mother, daughter and two others were killed when the 101-year-old building collapsed.

“Save the babies!” were his mother’s last words, he said.

In Havana, some of the same architectural gems that draw tens of thousands of American tourists crash to the ground every year. Causes range from weather and neglect to faulty renovations and theft of structural beams.

Carlos Guerrero, 45, said he and his family live “like scared dogs” in a crumbling building along Merced Street.

Neighbors tell them, “Get out of there! It’s going to collapse!”

“It makes you feel like going and living under a bridge,” said Guerrero, who vows to grab a machete and seek revenge on housing officials if anything happens to his wife and three children.

Some 3,856 partial or total building collapses were reported in Havana from 2000 to 2013, not including 2010 and 2011 when no records were kept.

The collapses worsened an already severe housing shortage. Havana alone had a deficit of 206,000 homes in 2016, official figures show.

The housing crisis is one of the most pressing challenges facing Cuban President Miguel Díaz-Canel, who vowed to improve housing after taking charge of the communist nation of 11 million people in April.

Havana, a city of about 2 million people, had a shortage of 206,000 homes in 2016, official figures show. (Photo: Tracey Eaton, Special to USA TODAY)

Havana officials have won dozens of international awards for their work to restore the historic sector known as Old Havana, with styles ranging from Baroque and neoclassical to Art Deco.

UNESCO calls Old Havana one of Latin America’s “most notable” historic city centers and named it a World Heritage site in 1982.

Havana officials use tourism revenue to renovate many architectural treasures, but can’t keep up with the decay.

Unsafe, uninhabitable

Officials estimate 28,000 people live in buildings that could collapse at any moment. Some residents refuse to leave structures that authorities have declared unsafe.

“Of course we’re scared but what are we going to do?” said Yanelis Flores, 42, who rejected a government offer to move into a shelter.

“I will wait for a house,” said Flores from the eighth floor of the former Hotel Astor, which had American management and 200 rooms in the 1930s.

Today, daylight shines through terrifying cracks in the walls.

“This is worse than a pig pen,” Flores said. “It’s rotting.”

The third-floor staircase collapsed in April 2017.

“It was a tremendous explosion – boom!” second-floor resident Yuslemy Díaz recalled. “People on the third and fourth floors were stranded because they couldn’t get down. It was a madhouse.”

Workers brought in a truck-mounted crane to deliver meals to stranded residents. to know how it works, you can learn more about it here

They built a makeshift wooden staircase. Authorities began relocating residents on the 9th and 10th floors.

Díaz, 32, a manicurist, is eager to move.

‘You live with fear’

“The moment it starts to rain and a little stone falls next to you, you think it was the building. You live with fear. A building doesn’t tell you, ‘I’m going to fall tomorrow at 3 p.m.’ It falls – boom! – at any time day or night. It doesn’t warn you.”

Before the stairway failure, residents say, people had been prying valuable marble tiles from the walls, weakening the staircase.

Yunier Angulo, 31, a butcher, left the building seconds before the stairway crumbled. A man just behind him was seriously hurt.

Angulo’s friends told him he was lucky. “You were born that day,” they said. But he doesn’t feel any safer and said he sleeps “with one eye open and the other closed.”

“The building could collapse tomorrow. It gets worse every day.”

Across town, Leydis Castro, 77, has a leaky ceiling, but refuses to ask for a handout. “The government doesn’t have a duty to fix everyone’s house.”

Her neighbors disagreed and wouldn’t pay a cent when the city offered repairs in exchange for a monthly fee, she said.

Fidel Castro promised to demolish “hellish tenements” and build safe, modern housing when he took power in 1959.

Today, Magaly Marrero, 65, said her apartment is so bad that she showers in the kitchen and relieves herself in a bucket.

“Sometimes I say, ‘God, how long will I live in these conditions?’ This is no life,” she said. “What can I aspire to? To die buried because one day the roof comes down and crushes me?”

No deaths, injuries data

Cuban officials don’t release figures on those killed or injured in building collapses.

Álvarez, the baker, said before his second-story apartment came down on July 15, 2015, workers on the ground floor had been using a jackhammer to strip the walls to the brick. He said cracks from below began inching toward his apartment. His mother complained, but city inspectors said the workers weren’t to blame.

Álvarez said his wife, Lizbett, 41, fell head first into the rubble during the building collapse and was in a coma for 22 days. She recovered, but doesn’t like talking about the episode and won’t walk past 409 Havana Street where her home once stood.

Álvarez fractured his spine in three places, but dismissed his injuries and praised the victims.

Rafael Álvarez said his mother who was killed in the building collapse taught him “to be strong, to persevere. To be a good person, to get along with everyone.” (Photo: Tracey Eaton, Special to USA TODAY)

He said his mother, Mayra Páez, 60, shouted “Save the babies!” until her voice grew silent.

Rescuers told him she suffocated. She was a former nurse, “much loved in the neighborhood,” her son said.

She taught him “to be strong, to persevere. To be a good person, to get along with everyone.”

No one could save his daughter, Genolan, 3. She was “a happy girl,” her father said. “She talked all the time and danced a lot.”

His nephew, Jorge Álvarez, 18, wanted to be a welder.

“He was my life,” his uncle said.

The teenager’s girlfriend, Glendys Kindelán, had just turned 18. Her mother, Yaima Kindelán, said she frantically searched for her daughter at hospitals before finding her body, wrapped in gauze at a funeral home.

“I couldn’t see her face,” she said.

She said her daughter “a very respectful girl, a student” who dressed as a nurse for a photo shoot on her 15th birthday. Her mom joined her as a police officer.

The teen had two dogs, Yonky and Princesa, who rarely left her side. “Having those little animals that she loved so much, she wanted to become a veterinarian,” Kindelán said.

After the accident, authorities investigated an architect and four others who had planned to open a fast-food restaurant at the site.

This summer, authorities told Álvarez they didn’t have enough evidence to prosecute anyone.

“I started to cry. I expected that justice would be done. They said, ‘Calm down, sir. Calm down. Do you want some water?’

The U.S. housing sector is falling apart, and the Federal Reserve is all but ignoring the damage as it prepares for what many expect to be three rate hikes in 2019, CNBC’s Jim Cramer warned Friday.

“The housing sector’s a disaster,” Cramer said on “Closing Bell.” “We’re building about half the houses we did when the country had half the people, and we still can’t sell them. KB Home does a huge amount of housing in California. They can’t sell them. ”

U.S. homebuilding fell more drastically than expected in September, according to the Commerce Department. Housing starts dropped 5.3 percent after rising slightly in August. Existing home sales also dropped the most in over two years as rising material costs crimped supply and rising mortgage rates deterred prospective buyers.

The Fed’s interest rate hikes have contributed to the surge in mortgage rates, which in October jumped above 5 percent. The central bank has said it plans to hike rates in December of this year — a move Cramer supports — and three more times in 2019.

“I favor a rate hike, and then I’d like to wait. In what world is that irrational?” Cramer said Friday. “Affordability’s gotten out of control. [The Fed members] know that. We have affordability data. But they don’t want to focus on the things they should.”

That lack of rigor is leading the Fed to make decisions that are “not safe” and “irresponsible” when it comes to the U.S. economy, the “Mad Money” host said, echoing his earlier point that the Fed needs to do more homework.

“We shouldn’t look upon them as if they have great information. They had such bad information in 2007,” Cramer said. “They have this judgment that the economy’s great. It’s an irresponsible, non-empirical judgment. It’s anecdotal. It has not a lot of homework. And I favor rigor. I think rigor is what matters, sophistication and rigor. And they’re unsophisticated, and they’re non-rigorous, and I would rip up their homework and tell them to go home.”

According to the Census Bureau’s Survey of Construction, the share of new homes started with 5,000 square feet or more of living space stood at 3.08 percent in 2017, essentially unchanged from 3.05 percent in 2016. The total number of 5,000+ square-foot homes started in absolute terms was 26,000, up from 24,000 in 2016.

In 2015, the number of 5,000+ square feet homes started was the highest since 2007, and their share of the new market was the highest since the inception of the series in 1999. In the boom year of 2006, 3.04% or 45,000 new homes started were 5,000 square feet or larger. In 2007, the share of new homes this size was 3.56%, yet the total number that year fell to 37,000. In 2008, only 20,000 such homes were started, or 3.24% of the total. From 2009 to 2012, the number of these large homes started remained well under 20,000 a year and accounted for less than 3% of all new single-family construction during this period.

A previous post discussed a recent, slight downward trend in the median and average size of new single-family homes evident in quarterly data and attributed this to an expansion in the entry-level segment. The post concludes that home size is expected to trend lower. Some growth is possible at the upper tail of the size distribution, however, even if the overall average is trending in the opposite direction.

When analyzed by the different characteristics, 80 percent of 5,000+ square feet home started in 2017 have a porch, 74 percent have a finished basement, 68 percent have a 3-or-more car garage, 63 percent have a patioand more than half (56 percent) have a community association. Fifty-eight percent of the homes have 5 bedrooms or more and 73 percent have 4 bathrooms or more.

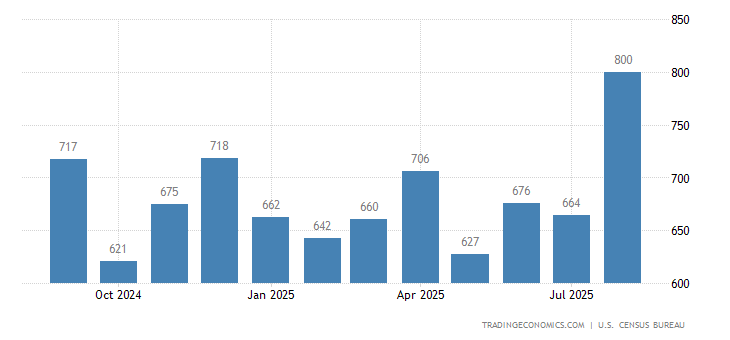

Sales of new single-family houses in the United States dropped 5.5 percent from the previous month to a seasonally adjusted annual rate of 553 thousand in September of 2018, following a downwardly revised 3.0 percent decline in August. August. It is the lowest rate since December 2016, worse than market expectations of 625 thousand. Sales in the Northeast went down to its lowest level since April 2015. Also, sales decreased in the West and in the South. New Home Sales in the United States averaged 650.36 Thousand from 1963 until 2018, reaching an all time high of 1389 Thousand in July of 2005 and a record low of 270 Thousand in February of 2011.

US New Home Sales Lowest Since 2016

Sales of new single-family houses in the United States dropped 5.5 percent from the previous month to a seasonally adjusted annual rate of 553 thousand in September of 2018, following a downwardly revised 3.0 percent decline in August. It is the lowest rate since December 2016, worse than market expectations of 625 thousand. Sales in the Northeast went down to its lowest level since April 2015. Also, sales decreased in the West and in the South.

Sales declined in the Northeast (-40.6 percent to 19 thousand), its lowest level since April 2015; the West (-12 percent to 139 thousand) and in the South (-1.5 percent to 318 thousand). On the other hand, sales rose 6.9 percent to 77 in the Midwest. The median sales price of new houses sold was USD 320,000 below USD 331,500 in the same month of the previous year. The average sales price fell to USD 377,200 in September from USD 379,300 a year ago.

The stock of new houses for sale went up 2.8 percent to 327 thousand. This represents a supply of 7.1 months at the current sales rate, up from 6.5 months in August.

Year-on-year, new home sales decreased 13.2 percent.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the average 30-year fixed mortgage rate moving to its highest mark since July.

News Facts

30-year fixed-rate mortgage (FRM) averaged 3.95 percent with an average 0.5 point for the week ending November 16, 2017, up from last week when it averaged 3.90 percent. A year ago at this time, the 30-year FRM averaged 3.94 percent.

15-year FRM this week averaged 3.31 percent with an average 0.5 point, up from last week when it averaged 3.24 percent. A year ago at this time, the 15-year FRM averaged 3.14 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.21 percent this week with an average 0.4 point, down from last week when it averaged 3.22 percent. A year ago at this time, the 5-year ARM averaged 3.07 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Quote Attributed to Sean Becketti, chief economist, Freddie Mac. “Rates increased this week. The 10-year Treasury yield ticked up 6 basis points, while the 30-year mortgage rate jumped 5 basis points to 3.95 percent. Today’s survey rate is the highest rate in nearly four months.”

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed mortgage rate inching lower for the third consecutive week and setting a new low for the year.

News Facts

30-year fixed-rate mortgage (FRM) averaged 3.94 percent with an average 0.5 point for the week ending June 1, 2017, down from last week when it averaged 3.95 percent. A year ago at this time, the 30-year FRM averaged 3.66 percent.

15-year FRM this week averaged 3.19 percent with an average 0.5 point, the same as last week. A year ago at this time, the 15-year FRM averaged 2.92 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.11 percent this week with an average 0.5 point, up from last week when it averaged 3.07 percent. A year ago at this time, the 5-year ARM averaged 2.88 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Quote Attributed to Sean Becketti, chief economist, Freddie Mac.

“In a short week following Memorial Day, the 10-year Treasury yield fell 4 basis points. The 30-year mortgage rate remained relatively flat, falling 1 basis point to 3.94 percent and once again hitting a new 2017 low.”

– New U.S. single-family home sales unexpectedly rose in September, pointing to sustained demand for housing even as data for August was revised sharply down.

The Commerce Department said on Wednesday new home sales increased 3.1 percent to a seasonally adjusted annual rate of 593,000 units last month, pulling them close to a nine-year high touched in July.

August’s sales pace was revised down to 575,000 units from the previously reported 609,000 units.

Economists polled by Reuters had forecast single-family home sales, which account for about 9.8 percent of overall home sales, falling to a rate of 600,000 units last month.

New home sales, which are derived from building permits, are volatile on a month-to-month basis and subject to large revisions.

Sales increased 29.8 percent from a year ago. They rose in the third quarter compared to the April-June period, indicating strong demand for housing.

Residential construction, however, likely remained a drag on gross domestic product in the third quarter.

Despite rising demand for housing, home building has been lagging, with builders complaining about land and labor shortages. Demand is being driven by rising wages as the labor market nears full employment, as well as by very low mortgage rates.

New single-family homes sales surged 33.3 percent in the Northeast and soared 8.6 percent in the Midwest last month.

Sales in the South, which accounts for more than half of new home sales, climbed 3.4 percent.

Sales fell 4.5 percent in the West, which has seen a sharp increase in home prices amid tight inventories.

Housing demand is rising rapidly, but a key cog in the wheel to homeownership is in deep trouble. The people most needed to close the deal are disappearing. Appraisers, the men and women who value homes and whom mortgage lenders depend upon, are shrinking in numbers. Learn about the value of your property with a palm beach county property appraiser to ensure you get money’s worth.

That is causing growing delays in closings, costing buyers and sellers money and in some cases even scuttling deals.

The share of on-time closings has dropped from 77 percent last April to 64 percent today for loans backed by Fannie Mae and Freddie Mac, according to Campbell/Inside Mortgage Finance. Appraisal-related issues in these delays jumped by 50 percent in that time.

“The appraisal shortage is massive. You’re seeing significant delays, you’re seeing cost increases, you’re seeing rate [locks] expire,” said Brian Coester, CEO of Rockville, Maryland-based CoesterVMS, a national appraisal management company.

Since 2007, when the U.S. housing market came crashing down, the number of appraisers has shrunk by 22 percent, according to the Appraisal Institute, an industry association. With so few new cadets, the current population of appraisers is aging. More than 60 percent are over the age of 50.

Ironically, the decline in new appraisers is largely due to new regulations designed to safeguard both banks and borrowers. They were put in place at the end of 2008 by Fannie Mae, Freddie Mac and the FHA, as the entire mortgage banking community was under strict scrutiny after the financial crisis. They changed the rules that would allow appraiser apprentices to do full appraisals and instead require the licensed appraiser to be on-site for the inspection.

The result is that appraisers no longer see a need to pay apprentices, but at the same time, licensing requirements to become an appraiser include 2,500 hours of appraisal experience to be completed in two years as an apprentice.

“The typical appraiser, he’s going to do approximately 10-15 appraisals a week. For him to be able to take a trainee, he needs the ability for the trainee to go ahead and inspect the property for him,” said Coester. “The rules have changed now, and you cannot do what you used to be able to do 10 years ago, which is hire three to four trainees and really have them go and inspect the properties, go and do work for you and really function as an apprentice. That market has been completely eliminated.”

At 1 p.m. on a Monday in Frederick, Maryland, appraiser Joyce Smith has already valued three homes and is walking into the fourth. A 23-year veteran of the business, she said she has never been this busy.

“I get calls five, six, seven, eight times a day. I used to go far away to do appraisals, but there are so many, I don’t have to go very far anymore,” said Smith.

In some of the nation’s hottest housing markets, where sales are up double digits compared to a year ago, the shortage means searching far and wide for an appraiser.

“We’ve been hearing from our agents in Colorado about significant delays in getting appraisals done,” said Alina Ptaszynski, a spokesperson for Redfin. “Our Denver market manager said for one deal, the appraiser came in from Cheyenne, Wyoming. She reported it taking up to seven weeks to get an appraisal done. Valuations aren’t the concern as much as the delays.”

Valuations are, however, becoming increasingly important, as home price gains accelerate, and competition in the market heats up. Prices could change in the course of two months, the delay time it is now taking in some markets to have an appraisal done. Mortgage rates are also starting to move in a wider range, and that makes rate-locks ever more important. It can cost significant cash to extend a rate lock.

Craig WebbEnergy retrofit remodelers at work in my bedroom.

Readers: I’m recovering from a remodel, and I’ve been told that talking about it will make the recovery easier. This is the second time my wife and I have made major, debris-raising changes to our home. The first was a whole-house remodel that included a new addition. This time we got a basement-to-attic energy retrofit in our Washington, D.C., home. I’m quite happy with the results, but I can see why the trauma of remodeling has shaken many others. So I’ve come up with seven rules for you to share with neophyte homeowners.

Rule No. 1: Remember, homeowner, that for the length of the remodel, it’s not your house anymore. You need to trust the people you’ve hired to do the remodel or else buy a big case of ulcer medicine.

Rule No. 2: There is no such thing as a dust-free remodeling project.

Rule No. 3: Try to talk your significant other—the one who frets most about neatness, odors, and general cleanliness—into leaving town before the work starts.

Rule No. 4: Far more things in your house can get broken than you could ever imagine.

Rule No. 5: Short of having exit doors on every wall and every floor, odds are good that workers will traipse through—and generate dirt in—parts of the house that are nowhere near the work zones.

Rule No. 6: Sometime during the remodel, expect that the new crew will reveal to you something done badly by the last people who worked on the house.

Rule No. 7: It always looks irredeemably disastrous before the cleanup begins.

You’d think that spending years as the editor-in-chief of REMODELING, plus that previous experience with a renovation, would have prepared me sufficiently for the arrival of Attilio Manziano-Verrilli, our project manager fromHome Energy Medics, and his platoons of subcontractors. My wife and I spent the prior weekend moving precious objects and trying to anticipate which parts of the house would get whacked and chipped by workers as they hauled equipment up our narrow stairs. I thought we’d done well until I saw a sub unknowingly jostle a $300 pendant light with a 12-foot stud.