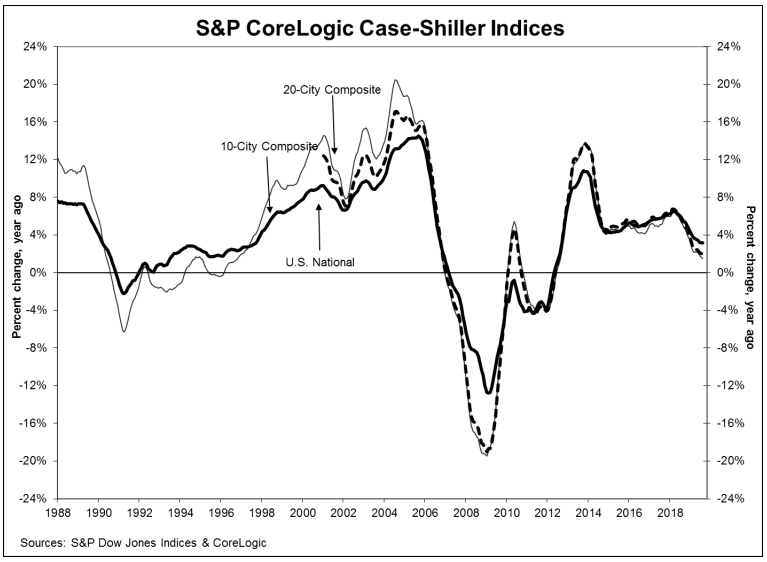

August 2019 saw an annual increase of 3.2% for home prices nationwide, inching forward from the previous month’s pace, according to the Case-Shiller Home Price Index from S&P Dow Jones Indices and CoreLogic.

The 10-City and 20-City composites reported a 1.5% and 2% year-over-year increase, respectively. During the month, 11 of 20 cities reported increases before seasonal adjustment, whereas 17 of 20 cities reported increases after seasonal adjustment.

“The U.S. National Home Price NSA Index trend remained intact with a year-over-year price change of 3.2%,” said Philip Murphy, Managing Director and Global Head of Index Governance at S&P Dow Jones Indices. “However, a shift in regional leadership may be underway beneath the headline national index.”

According to the index, Phoenix, Charlotte, and Tampa reported the highest year-over-year gains among all of the 20 cities.

In August, Phoenix led with a 6.3% year-over-year price increase, followed by Charlotte with a 4.5% increase and Tampa with a 4.3% increase. Seven of the 20 cities reported larger price increases in the year ending August 2019 versus the year ending July 2019.

“Phoenix saw an increase in its year over year price change to 6.3% and retained its leading position,” Murphy said. “However, Las Vegas dropped from No. 2 to No. 8 among the cities of the 20-City Composite, falling from a 4.7% year-over-year change in July to only 3.3% in August.”

“Meanwhile, the Southeast region included three of the top four cities. Charlotte, Tampa, and Atlanta all recorded solid year-over-year performance with price changes of 4.5%, 4.3%, and 4.0%, respectively,” Murphy said. “In the Northwest, Seattle’s year-over-year change turned positive (0.7%) after three consecutive months of negative year-over-year price changes. The 10-City Composite year-over-year price change declined slightly from July to 1.5%, while the 20-City Composite year-over-year price change remained steady at 2.0%. San Francisco was the only city to record a negative YOY price change (-0.1%).”

The graph below highlights the average home prices within the 10-City and 20-City Composites:

The National Association of Home Builders’ (NAHB) Remodeling Market Index (RMI) posted a reading of 55 in the third quarter of 2019, unchanged from last quarter (Figure 1). Since the second quarter of 2013, the RMI has been above its breakeven point of 50, which indicates that more remodelers report market activity is higher than report it is lower, compared to the prior quarter.

The overall RMI is an average of two sub-indices, one measuring current remodeling activity and another measuring future indicators. The current market conditions index edged down one point to 54 from the previous quarter (Figure 2). Among its three major components, major additions and alterations dropped one point to 52, minor additions and alterations decreased by two points to 53 and the home maintenance and repair component rose one point to 57.

The future market indicators gained two points from the previous quarter to 57 (Figure 3). Calls for bids increased by one to 55, amount of work committed for the next three months gained two points to 54, the backlog of remodeling jobs increased one point to 59 and appointments for proposals jumped by five points to 60.

Demand for remodeling is solid and is supported by a healthy labor market and low interest rates. It is important to note that remodelers still face challenges, such as high costs and a lack of skilled labor.

The average FICO score stands at 706, a record high, said Ethan Dornhelm, vice president of scores and predictive analytics at FICO. That compares with 686 at the 2009 end of the Great Recession and it eclipses the 690 at the 2006 height of the housing bubble.

The key drivers are U.S. economic expansion that has propelled job growth and an increase in consumer education about protecting and improving scores, Dornhelm said in a blog post. In addition, the passage of time is helping to remove the credit scars from events that happened during the financial crisis, he said.

“Consumers who suffered financial misfortune during the Great Recession have over the past few years had the associated missed payments from that time period purged from their credit file, in accordance with the Fair Credit Reporting Act,” he said.

Measuring different credit events, the biggest improvement between April 2009 and April 2019 was the timeliness of mortgage payments, Dornhelm said. A decade ago, 7.2% of the population had been 90 days or more late on a mortgage payment within the last two years. By April, it had dropped to 2.8%.

Also showing big improvement was the percentage of the population who had been 90 days or more past due on a credit card in the last two years. A decade ago, it was 13%, and in April it was 8.6%.

The jump in FICO scores was due to “score improvement, not score inflation,” Dornhelm said.

“Significant improvement in the overall population’s credit profile has been the key driver of the 20-point increase in national average FICO score over the past decade,” he said. “These improvements are reflective of improving consumer financial health, as would be expected during a period of economic expansion.”

Economic data signaling the chance of a looming recession has increased uncertainty in the credit-scoring realm, he said.

“The average FICO score will continue to change, but in what direction?” Dornhelm said. “Trade talks with China, the possibility of a `no-deal Brexit,’ and Fed interest rate decisions loom large as concerns of a recession persist.”

Prices paid for goods used in residential construction decreased by 1.1% in June (not seasonally adjusted) according to the latest Producer Price Index (PPI) released by the Bureau of Labor Statistics. The decline broke a four-month trend of increases and was only the fifth month over the past two years in which prices fell.

Over the past 12 months, building materials prices have decreased 1.6%, just the fifth June year-over-year decrease since 2000. The decline is a sharp reversal of June 2017 to June 2018, during which prices increased 8.8%.

The PPI report shows that softwood lumber prices decreased (-1.7%, not seasonally adjusted) in June—the index’s third consecutive monthly decline. Prices remain at their lowest level since February 2017. While weekly prices have been volatile since mid-May according to Random Lengths, the difference between the average prices of softwood lumber in May and June mirrored the PPI data (-1.8% v. -1.7%).

One of the special indexes published by BLS tracks lumber and plywood in one category. Similar to softwood lumber, the lumber and plywood index fell 2.3%. Prices paid for softwood lumber and lumber and plywood have decreased 23.1% and 17.6%, respectively, since June 2018.

The price index for gypsum products continued its downward trend in June, declining 1.9%. In the last 10 months, gypsum prices have only increased twice.

Prices have declined by 6.2% and 10.8% since January 2019 and August 2018, respectively.

Ready-mix concrete prices increased 1.2% in June and remain relatively volatile. Prices have risen by more than 1.0% in two of the past three months, something that has only happened in 18 of the previous 231 months.

The housing market won’t recover much in the second half of 2019, says Capital Economics.

Mortgage interest rates have fallen this year, but that hasn’t spurred much action in the housing market, and things are unlikely to turn around for the remainder of the year as concerns about the economy continue to grow, the economists say.

“The fact interest rates are declining because of concerns that the economy is slowing argues against a strong rise in home purchase demand,” Capital Economics writes in a recent report. “That is reflected in measures of buyer sentiment. The decline in interest rates earlier this year failed to provide much of a boost to the share of households saying now is a good time to buy.”

That said, the report did indicate that rental demand will be solid thanks to strong wage growth and subdued home sales. And, the drop in rates has helped spur refinance activity, with applications jumping in the first half of June and signals indicating the likelihood of an upward trend for refis.

But purchase demand is less sensitive to changes in mortgage rates, the economists say, and home sales have therefore seen less of a lift from the drop in financing costs.

Also, the drop in rates was somewhat offset by tighter lender standards, the report says, including a recent pullback from the Federal Housing Administration that may make it harder for some riskier borrowers to qualify.

But on the bright side, homes are still affordable, the economists say.

“The fall in mortgage interest rates, slower house price gains and the rise in earnings growth have led to a drop in mortgage payments as a share of income,” the report says. “And, based on our forecasts for those variables, the payment burden is set to stay at around 16% over the next couple years, low by past standards.”

But the housing market is plagued by a lack of inventory, and this will prevent any meaningful rise in existing home sales, the report predicts.

“While the number of existing homes for sale has seen some improvement since reaching a record low at the end of 2017, at 1.8 million in May market conditions are still tight,” the report says. “And with interest rates falling back, we doubt existing inventory levels will see much of an improvement over the next couple of years.”

Mortgage rates have steadily declined with the 30-year fixed-rate bottoming out to 3.82 percent, its lowest level since September 2017, according to the latest figures from Freddie Mac.

Digital Risk co-founder Jeff Taylor told FOX Business’ Neil Cavuto that now is the time for new home buyers to take advantage of the bigger inventory on the market.

“If you’re looking to get into the housing market, i.e., you don’t have a house right now, this is literally the perfect time,” he during an interview on Monday. “Interest rates are about a one percentage point less than it was this time last year … that’s a 10 percent savings on a 30-year mortgage a month.”B

The Federal Reservemight cut the federal funds rate twice this year, a move that could cause the 30-year fixed rate to fall even lower.

“If you get two rate cuts at 50 and if you get to 75, yeah, I think you can be back down to three and a quarter [percent], Taylor said.C

Taylor adds that the lower interest rates allow consumers to reach a little deeper into their pockets and “afford more of a house.”

“People are feeling better about their jobs right now and they’ve been saving. It’s a great time to finally to get into the housing market and make a purchase,” he said.

Housing starts in the US rose 5.7 percent from a month earlier to a seasonally adjusted annual rate of 1,235 thousand units in April 2019, more than an expected 1,205 thousand and following a revised 1.7 percent advance in March.

Single-family homebuilding, which accounts for the largest share of the housing market, rose 6.2 percent to a rate of 854 thousand units in April and starts for the volatile multi-family housing segment advanced 4.7 percent to a rate of 381 thousand units. Increases in housing starts were recorded in the Northeast (84.6 percent to 144 thousand) and Midwest (42 percent to 186 thousand), while declines were seen in the South (-5.7 percent to 581 thousand) and West (-5.5 percent to 324 thousand). Starts for March were revised to 1,168 thousand from 1,139 thousand.

Building permits were up 0.6 percent to a rate of 1,296 thousand units in April, while markets had expected a 0.5 percent gain. Permits for the volatile multi-family housing segment increased 8.9 percent to 514 thousand, while single-family authorizations fell 4.2 percent to 782 thousand. Across regions, permits were higher in the West (5.3 percent to 339 thousand) and Midwest (2.2 percent to 188 thousand), but dropped in the Northeast (-4 percent to 120 thousand) and South (-1.2 percent to 649 thousand).

Year-on-year, housing starts dropped 2.5 percent and building permits decreased 5 percent.

According to a estimates from the U.S. Housing and Urban Development and Commerce Department, single-family starts continued to show weakness in March, despite the recent stabilization in the NAHB/Wells Fargo Housing Market Index (HMI). After downward revisions made to the February data, single-family starts were down 0.4% to a 785,000 seasonally adjusted annual pace in March, the lowest such rate since September 2016.

On a year-to-date basis, single-family construction is 5.3% lower than the first quarter of 2018. NAHB’s forecast, and the forward-looking HMI suggest that future data will show stabilization followed by slight gains due to recent declines in mortgage interest rates. Why not you check this out for more information about construction. However, single-family permits continued to be soft in March, declining 1.1% for the month to a 808,000 annual pace, the lowest since August 2017. Most of this is because many of the constructions that start of end up being unsuccessful, if you want to avoid this then consider reading these tool box topics to learn what you can use to successfully manage a construction.

On a regional and year-to-date basis, single-family starts are down 21% in the housing affordability challenged West, 20% in the Midwest, 2% in the Northeast and up 5% in the South.

Multifamily starts were unchanged from February to March at a 354,000 annual rate. However, comparing the first quarter of 2019 to the first quarter of 2018 shows a 19% decline for 5+ unit production.

Recent production declines are clear in the current estimates of units under production. As of March 2019, there were 531,000 single-family homes under construction. While this is 4.5% higher than a year ago, it is down from the 543,00 peak count from January 2019. Similarly, there are currently 595,000 apartments under construction, which is more than 3% lower than a year ago and down from the peak count of 625,000 in February 2017. The combination of these declines in current construction activity are seen clearly in the graph below, with declines for total housing under construction for all of 2019.

California home sales close year on downward trend as home prices post mild gains, C.A.R. reports

– Existing, single-family home sales totaled 372,260 in December on a seasonally adjusted annualized rate, down 2.4 percent from November and down 11.6 percent from December 2017.

– December’s statewide median home price was $557,600, down 0.5 percent from November and up 1.5 percent from December 2017.

– Statewide active listings rose for the ninth straight month, increasing 30.6 percent from the previous year.

– The statewide Unsold Inventory Index was 3.5 months in December, down from 3.7 months in November.

– For the year as a whole, sales were down 5.2 percent from 2017.

LOS ANGELES (Jan. 17) – California home sales declined for the eighth straight month in December, and a stagnating market for much of the year pushed sales lower in 2018 for the first time in four years, the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.) said today.

Closed escrow sales of existing, single-family detached homes in California totaled a seasonally adjusted annualized rate of 372,260 units in December, according to information collected by C.A.R. from more than 90 local REALTOR®associations and MLSs statewide. The statewide annualized sales figure represents what would be the total number of homes sold during 2018 if sales maintained the December pace throughout the year. It is adjusted to account for seasonal factors that typically influence home sales.

December’s sales figure was down 2.4 percent from the revised 381,400 level in November and down 11.6 percent from home sales in December 2017 of 420,960. December marked the fifth month in a row that sales were below 400,000 and the lowest level of sales sold since January 2015.

“The housing market continued to shift in December and drift downward as sales have fallen double digits for the past three out of four months,” said C.A.R. President Jared Martin. “This trend is expected to continue, as buyers remain cautious about the murky housing market outlook due primarily to the volatility in the financial markets and uncertainty in the economic and political arenas.

“Additionally, housing markets in and around the wildfire areas have been exhibiting unusual patterns that could remain unsettled for the next few months. The impact, however, is confined mostly within the region and should not have a noticeable effect in the housing market at the state level.”

The statewide median home price declined to $557,600 in December. The December statewide median price was up 0.5 percent from $554,760 in November and up 1.5 percent from a revised $549,550 in December 2017. The statewide median home price for the year as a whole was $570,010, up 6.0 percent from $537,860 in 2017.

“California’s housing market in 2018 was hindered by endlessly rising home prices and interest rate hikes, which combined to erode housing affordability and hamper home sales,” said C.A.R. Senior Vice President and Chief Economist Leslie Appleton-Young. “As a result, while the statewide median home price surpassed its previous peak and set a new record in 2018, annual home sales fell for the first time in four years to a preliminary 402,750 closed escrows in California, down from 2017’s pace of 424,890.

“In the coming months, we expect a brief hiccup in sales as the government shutdown temporarily delays closings due to interruptions in IRS income verification or the processing of HUD, VA and USDA loans,” said Appleton-Young.

Other key points from C.A.R.’s December 2018 resale housing report include:

On a regionwide, non-seasonally adjusted basis, sales dropped double-digits on a year-over-year basis in the San Francisco Bay Area, the Central Coast, Central Valley and Southern California regions, with the Central Coast dropping the most at 24.9 percent.

Thirty-nine of the 51 counties reported by C.A.R. posted a sales decline in December with an average year-over-year sales decline of 20 percent. Thirty-four counties recorded double-digit sales drops on an annual basis, and 10 counties experienced an increase in sales from a year ago.

Sales for the San Francisco Bay Area as a whole fell 17.5 percent from a year ago. Eight of nine Bay Area counties recorded annual sales declines of more than 10 percent. Only San Francisco County posted a year-over-year increase, gaining 11.3 percent from December 2017.

The Los Angeles Metro region posted a year-over-year sales drop of 17.8 percent, as home sales fell 16.3 percent in Los Angeles County and 18.3 percent in Orange County.

Home sales in the Inland Empire declined 19.8 percent from a year ago as Riverside and San Bernardino counties posted annual sales declines of 17.7 percent and 23.1 percent, respectively.

The median home price continued to increase in all regions, except in the San Francisco Bay Area. On a year-over-year basis, the Bay Area median price dipped 3.6 percent from December 2017. Home prices in Marin, San Francisco, San Mateo and Santa Clara counties continued to remain above $1 million, but both San Mateo County and Santa Clara counties recorded a year-over-year price decline.

Statewide active listings rose for the ninth consecutive month after nearly three straight years of declines, increasing 30.6 percent from the previous year. All major regions recorded an increase in active listings, with the Bay Area posting the highest increase at 65 percent, followed by Southern California (34 percent), Central Valley (24 percent) and the Central Coast (12 percent).

The Unsold Inventory Index, which is a ratio of inventory over sales, increased year-to-year from 2.5 months in December 2017 to 3.5 months in December 2018. The index measures the number of months it would take to sell the supply of homes on the market at the current sales rate.

The median number of days it took to sell a California single-family home rose from 25 days in December 2017 to 32 days in December 2018.

C.A.R.’s statewide sales price-to-list-price ratio* decreased from 98.7 percent in December 2017 to 97.4 percent in December 2018.

The average statewide price per square foot** for an existing, single-family home statewide edged up from $268 in December 2018 to $266 in December 2017.

The 30-year, fixed-mortgage interest rate averaged 4.64 percent in December, up from 3.95 percent in December 2017, according to Freddie Mac. The five-year, adjustable mortgage interest rate also increased in December to an average of 4.02 percent from 3.39 from December 2017.

Note: The County MLS median price and sales data in the tables are generated from a survey of more than 90 associations of REALTORS® throughout the state and represent statistics of existing single-family detached homes only. County sales data are not adjusted to account for seasonal factors that can influence home sales. Movements in sales prices should not be interpreted as changes in the cost of a standard home. The median price is where half sold for more and half sold for less; medians are more typical than average prices, which are skewed by a relatively small share of transactions at either the lower-end or the upper-end. Median prices can be influenced by changes in cost, as well as changes in the characteristics and the size of homes sold. The change in median prices should not be construed as actual price changes in specific homes.

*Sales-to-list-price ratio is an indicator that reflects the negotiation power of home buyers and home sellers under current market conditions. The ratio is calculated by dividing the final sales price of a property by its last list price and is expressed as a percentage. A sales-to-list ratio with 100 percent or above suggests that the property sold for more than the list price, and a ratio below 100 percent indicates that the price sold below the asking price.

**Price per square foot is a measure commonly used by real estate agents and brokers to determine how much a square foot of space a buyer will pay for a property. It is calculated as the sale price of the home divided by the number of finished square feet. C.A.R. currently tracks price-per-square foot statistics for 50 counties.

Leading the way…® in California real estate for more than 110 years, the CALIFORNIA ASSOCIATION OF REALTORS® (www.car.org) is one of the largest state trade organizations in the United States with more than 190,000 members dedicated to the advancement of professionalism in real estate. C.A.R. is headquartered in Los Angeles.

# # #

December 2018 County Sales and Price Activity (Regional and condo sales data not seasonally adjusted)

December 2018

Median Sold Price of Existing Single-Family Homes

Sales

State/Region/County

Dec. 2018

Nov. 2018

Dec. 2017

Price MTM% Chg

Price YTY% Chg

Sales MTM% Chg

Sales YTY% Chg

Calif. Single-family home

$557,600

$554,760

$549,550

r

0.5%

1.5%

-2.4%

-11.6%

Calif. Condo/Townhome

$460,660

$465,770

$446,840

-1.1%

3.1%

-10.0%

-21.4%

Los Angeles Metro Area

$500,000

$512,000

$495,000

r

-2.3%

1.0%

-8.3%

-17.8%

Central Coast

$717,650

$672,500

$657,500

6.7%

9.1%

-15.2%

-24.9%

Central Valley

$317,500

$320,000

$310,000

-0.8%

2.4%

-8.0%

-15.7%

Inland Empire

$359,000

$363,620

$342,000

r

-1.3%

5.0%

-10.1%

-19.8%

San Francisco Bay Area

$850,000

$905,000

$882,000

r

-6.1%

-3.6%

-20.2%

-17.5%

San Francisco Bay Area

Alameda

$850,000

$900,000

$862,000

-5.6%

-1.4%

-24.2%

-19.9%

Contra Costa

$612,500

$641,000

$600,000

-4.4%

2.1%

-19.1%

-16.7%

Marin

$1,270,500

$1,172,944

$1,268,900

8.3%

0.1%

-21.3%

-12.6%

Napa

$725,000

$683,500

$688,000

6.1%

5.4%

-14.1%

-21.8%

San Francisco

$1,500,000

$1,442,500

$1,475,000

4.0%

1.7%

-24.5%

11.3%

San Mateo

$1,483,000

$1,500,000

$1,500,000

-1.1%

-1.1%

-24.0%

-20.4%

Santa Clara

$1,150,000

$1,250,000

$1,300,000

-8.0%

-11.5%

-22.0%

-20.6%

Solano

$425,000

$450,000

$416,000

-5.6%

2.2%

-13.0%

-18.5%

Sonoma

$639,000

$612,500

$670,000

4.3%

-4.6%

-10.0%

-16.7%

Southern California

Los Angeles

$588,140

$553,940

$577,690

r

6.2%

1.8%

-3.0%

-16.3%

Orange

$785,000

$795,000

$785,500

-1.3%

-0.1%

-15.5%

-18.3%

Riverside

$398,000

$400,000

$385,000

-0.5%

3.4%

-4.9%

-17.7%

San Bernardino

$295,000

$299,450

$278,000

-1.5%

6.1%

-17.4%

-23.1%

San Diego

$618,500

$626,000

$605,000

-1.2%

2.2%

-7.4%

-14.7%

Ventura

$640,000

$643,740

$645,000

-0.6%

-0.8%

-14.0%

-13.8%

Central Coast

Monterey

$590,000

$630,000

$614,000

-6.3%

-3.9%

-26.1%

-31.0%

San Luis Obispo

$640,000

$624,000

$590,000

2.6%

8.5%

-16.3%

-23.7%

Santa Barbara

$806,030

$550,000

$730,000

46.6%

10.4%

-1.1%

-14.8%

Santa Cruz

$926,000

$862,500

$831,000

7.4%

11.4%

-16.2%

-31.7%

Central Valley

Fresno

$266,500

$265,750

$259,750

0.3%

2.6%

-4.1%

-4.7%

Glenn

$246,500

$225,000

$230,000

9.6%

7.2%

77.8%

113.3%

Kern

$242,380

$235,250

$233,000

3.0%

4.0%

-7.1%

-7.8%

Kings

$243,000

$222,000

$225,000

9.5%

8.0%

-7.1%

-17.0%

Madera

$263,000

$265,000

$239,000

r

-0.8%

10.0%

-18.8%

-34.6%

Merced

$269,060

$261,930

$239,900

2.7%

12.2%

22.0%

11.9%

Placer

$492,993

$461,000

$451,500

6.9%

9.2%

-10.2%

-18.5%

Sacramento

$364,500

$365,000

$350,000

-0.1%

4.1%

-14.8%

-22.4%

San Benito

$577,000

$583,200

$537,000

-1.1%

7.4%

-15.9%

-28.8%

San Joaquin

$365,000

$365,000

$349,720

0.0%

4.4%

1.1%

-14.1%

Stanislaus

$309,000

$310,000

$300,000

-0.3%

3.0%

-6.2%

-16.0%

Tulare

$236,450

$237,400

$219,500

-0.4%

7.7%

-11.5%

-20.1%

Other Calif. Counties

Amador

NA

NA

$305,000

NA

NA

NA

NA

Butte

$356,558

$326,940

$304,000

9.1%

17.3%

97.5%

105.3%

Calaveras

$310,000

$325,000

$285,000

-4.6%

8.8%

11.7%

-26.5%

Del Norte

$243,900

$250,000

$251,500

-2.4%

-3.0%

-40.0%

-36.8%

El Dorado

$454,500

$461,750

$450,000

-1.6%

1.0%

-15.5%

-33.6%

Humboldt

$308,000

$310,000

$319,500

-0.6%

-3.6%

-15.3%

-28.4%

Lake

$269,000

$255,000

$269,500

5.5%

-0.2%

17.7%

-6.4%

Lassen

$208,000

$184,000

$175,000

13.0%

18.9%

53.3%

0.0%

Mariposa

$320,000

$355,000

$310,000

-9.9%

3.2%

0.0%

40.0%

Mendocino

$424,900

$414,000

$409,500

2.6%

3.8%

-17.0%

-2.2%

Mono

$541,000

$725,000

$515,000

-25.4%

5.0%

-55.6%

-42.9%

Nevada

$389,950

$399,000

$393,500

-2.3%

-0.9%

1.1%

-6.0%

Plumas

$262,950

$289,500

$256,000

-9.2%

2.7%

0.0%

-13.3%

Shasta

$267,500

$283,000

$258,250

-5.5%

3.6%

-1.3%

6.8%

Siskiyou

$182,500

$226,000

$192,500

-19.2%

-5.2%

-13.5%

-33.3%

Sutter

$320,000

$296,000

$270,000

8.1%

18.5%

26.6%

5.2%

Tehama

$255,000

$199,000

$190,000

28.1%

34.2%

184.6%

100.0%

Tuolumne

$258,950

$288,500

$269,900

-10.2%

-4.1%

21.2%

27.0%

Yolo

$429,000

$429,500

$420,000

-0.1%

2.1%

-1.0%

-19.8%

Yuba

$298,000

$263,000

$241,000

13.3%

23.7%

2.5%

17.4%

r = revised NA = not available

December 2018 County Unsold Inventory and Days on Market

(Regional and condo sales data not seasonally adjusted)

Mortgage Rates Drop to Lowest Point in Three Months

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that rates dropped significantly after several weeks of moderating.

Sam Khater, Freddie Mac’s chief economist, says, “The 30-year fixed fell to 4.63 percent this week – the lowest it has been since mid-September. Mortgage rates have either fallen or remained flat for five consecutive weeks and purchase applicants are responding with an uptick in demand given these lower rates. While the housing market softened in response to higher rates through most of this year, the combination of a low unemployment and recent downdraft in rates should support home sales heading into the early winter months.”

News Facts

30-year fixed-rate mortgage (FRM) averaged 4.63 percent with an average 0.5 point for the week ending December 13, 2018, down from last week when it averaged 4.75. A year ago at this time, the 30-year FRM averaged 3.93 percent.

15-year FRM this week averaged 4.07 percent with an average 0.5 point, down from last week when it averaged 4.21 percent. A year ago at this time, the 15-year FRM averaged 3.36 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey