“Since the most recent peak in April, mortgage rates have declined nearly a quarter of a percent and have remained under three percent for the past month,” said Sam Khater, Freddie Mac’s Chief Economist. “Low rates offer homeowners an opportunity to lower their monthly payment by refinancing and our most recent research shows that many borrowers, especially Black and Hispanic borrowers, who could benefit from refinancing still aren’t pursuing the option.”

Khater continued, “Additionally, the low mortgage rate environment has been a boon to the housing market but may not last long as consumer inflation has accelerated at its fastest pace in more than twelve years and may lead to higher mortgage rates in the summer.”

News Facts

30-year fixed-rate mortgage averaged 2.94 percent with an average 0.7 point for the week ending May 13, 2021, down from last week when it averaged 2.96 percent. A year ago at this time, the 30-year FRM averaged 3.28 percent.

15-year fixed-rate mortgage averaged 2.26 percent with an average 0.6 point, down from last week when it averaged 2.30 percent. A year ago at this time, the 15-year FRM averaged 2.72 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 2.59 percent with an average 0.3 point, down from last week when it averaged 2.70 percent. A year ago at this time, the 5-year ARM averaged 3.18 percent.

The PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit. Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

As described in a previous post, NAHB’s recently released its 2021 Priced-Out Estimates, showing that 75.1 million households are not able to afford a median priced new home, and that an additional 153,967 would be priced out if the price goes up by $1,000. This post focuses on the related U.S. housing affordability pyramid, showing how many households have enough income to afford homes at various price thresholds.

The pyramid uses the same standard underwriting criterion as the priced-out estimates to determine affordability: that the sum of mortgage payments, property taxes, homeowners and private mortgage insurance premiums should be no more than 28% of the household income. Based on this, the minimum income required to purchase a $100,000 home is $22,505. In 2021, about 21.1 million households in the U.S. are estimated to have incomes at or below that threshold and, therefore, the maximum priced home they can afford is between $0 and $100,000. These 21.1 million households form the bottom step or base of the pyramid. Another 19.0 million can only afford to pay a top price of somewhere between $100,000 and $175,000 (the second step on the pyramid), and so on up the pyramid. Each step represents a maximum affordable price range for fewer and fewer households.

The top step of the pyramid shows that around 3 million households can buy a home priced above 1.55 million. These comparatively wealthy Americans and the high-end homes they can afford are interesting, but market analysts should never only focus on them to the exclusion of the larger number of Americans with more modest incomes that support the pyramid’s base.

Gov. Andrew Cuomo announced that he would sign the COVID-19 Emergency Eviction and Foreclosure Prevention Act of 2020 at a press briefing on Dec. 28.

ALBANY—After the State Legislature met in special session on Monday, Dec. 28 and the Assembly and Senate approved the bill, Gov. Andrew M. Cuomo signed the COVID-19 Emergency Eviction and Foreclosure Prevention Act of 2020 later that day.

The bill (S.9114/A.11181) prevents residential evictions, foreclosure proceedings until May 1, 2021 and also prohibits credit discrimination and negative credit reporting related to the COVID-19 pandemic. It also extends the Senior Citizens’ Homeowner Exemption and Disabled Homeowner Exemption from 2020 to 2021. The Act adds to New York State’s efforts to protect tenants and homeowners from the economic hardship incurred as a result of the COVID-19 pandemic.

“When the COVID-19 pandemic began, we asked New Yorkers to protect each other by staying at home. As we fight our way through the marathon this pandemic has become, we need to make sure New Yorkers still have homes to provide that protection,” Governor Cuomo said. “This law adds to previous executive orders by protecting the needy and vulnerable who, through no fault of their own, face eviction during an incredibly difficult period for New York. The more support we provide for tenants, mortgagors and seniors, the easier it will be for them to get back on their feet when the pandemic ends. I want to thank the legislature for passing this important protection for New Yorkers all across the state who need a hand. This is the kind of support that helps us stay New York Tough.”

The legislation helps tenants facing eviction and mortgagors facing foreclosure proceedings due the pandemic in five areas:

Residential Evictions

The Act places a moratorium on residential evictions until May 1, 2021 for tenants who have endured COVID-related hardship. Tenants must submit a hardship declaration, or a document explaining the source of the hardship, to prevent evictions. Landlords can evict tenants that are creating safety or health hazards for other tenants, and those tenants who do not submit hardship declarations.

Residential Foreclosure Proceedings

The Act also places a moratorium on residential foreclosure proceedings until May 1, 2021. Homeowners and small landlords who own 10 or fewer residential dwellings can file hardship declarations with their mortgage lender, other foreclosing party or a court that would prevent a foreclosure.

Tax Lien Sales

The Act prevents local governments from engaging in a tax lien sale or a tax foreclosure until at least May 1, 2021. Payments due to the locality are still due.

Credit Discrimination and Negative Credit Reporting

Lending institutions are prohibited from discriminating against a property owner seeking credit because the property owner has been granted a stay of mortgage foreclosure proceedings, tax foreclosure proceedings or tax lien sales. They are also prohibited from discriminating because the owner is in arrears and has filed a hardship declaration with the lender.

Senior Citizens’ Homeowner Exemption and Disabled Homeowner Exemption

Local governments are required to carry over SCHE and DHC exemptions from the 2020 assessment roll to the 2021 assessment roll at the same levels. They are also required to provide renewal applications for anyone who may be eligible for a larger exemption in 2021. Localities can also set procedures by which assessors can require renewal applications from people who the assessors believe may no longer be eligible for an exemption in 2021. Recipients of the exemption do not have to file renewal applications in person.

On Sept. 28, Governor Cuomo announced the State’s Tenant Safe Harbor Act would be extended and expanded until January 1, 2021 to protect additional residential tenants from eviction if they are suffering financial hardship during the COVID-19 public health emergency. The Executive Order extends the protections of the Tenant Safe Harbor Act to eviction warrants that existed prior to the start of the pandemic, and those who are facing other than nonpayment evictions but suffering the same hardship.

Governor Cuomo first announced a state moratorium on residential and commercial evictions on March 20 to ensure no tenant was evicted during the height of the public health emergency. The governor signed the Tenant Safe Harbor Act on June 30 which became effective immediately as well as additional legislation providing financial assistance to residential renters and landlords. Additionally, previous Executive Orders have prohibited charges or fees for late rent payments, and tenants facing financial hardship can still use their security deposit as payment and repay their security deposit over time.

Fueled by record-low mortgage rates and strong demand, existing home sales, as reported by the National Association of Realtors (NAR), rose for a fifth consecutive month in October and reached its highest level in almost 15 years.

Total existing home sales, including single-family homes, townhomes, condominiums and co-ops, rose 4.3% to a seasonally adjusted annual rate of 6.85 million in October, the highest level since November 2005. On a year-over-year basis, sales were 26.6% higher than a year ago.

The first-time buyer share increased to 32% in October from 31% both last month and a year ago. However, price gains threaten this share in the future. The October inventory level fell to 1.42 million units from 1.46 million units in September and is down from 1.77 million units a year ago.

At the current sales rate, the October unsold inventory represents an all-time low 2.5-month supply, down from 2.7-month in September and 3.9-month a year ago. This low level supply of resale homes is good news for home construction.

Homes stayed on the market for an average of just 21 days in October, an all-time low, seasonally even with last month and down from 36 days a year ago. In October, 72% of homes sold were on the market for less than a month.

The October all-cash sales share was 19% of transactions, up from 18% last month but unchanged from a year ago.

Tight supply continues to push up home prices. The October median sales price of all existing homes was $313,000, up 15.5% from a year ago, representing the 104th consecutive month of year-over-year increases. The median existing condominium/co-op price of $273,600 in October was up 10.3% from a year ago.

Regionally, all four regions saw month-over-month gains for existing home sales in October, ranging from 1.4% in the West to 8.6% in the Midwest. On a year-over-year basis, sales grew in all four regions as well, with the Northeast seeing the greatest gain (30.4%).

Though sales have flourished and demand remains strong due to low mortgage rates, the imbalance between housing supply and demand could hamper future sales by driving up home prices and restraining affordability. Though builder confidence soared to all-time high and housing starts at highest pace since the spring of 2007, more listings and home construction are still needed to meet this rising demand.

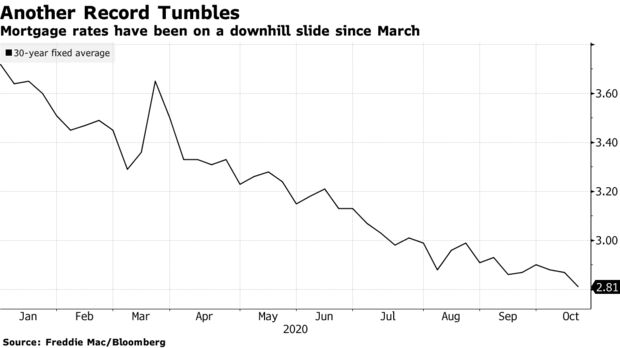

Mortgage rates in the U.S. have hit another record low.

The average for a 30-year, fixed loan dropped to 2.81%, down from 2.87% last week and the lowest in almost 50 years of data-keeping, Freddie Mac said in a statement Thursday. It was the 10th record low this year. The previous one — 2.86% — held for about a month.

The slide in borrowing costs that began in March, as fears of the coronavirus drove investors to the safety of Treasuries, shows no signs of stopping. The Federal Reserve has signaled it will hold its benchmark rate near zero through at least 2023. That should keep a lid on mortgage rates, which have been below 3% since July.

Cheap loans have been fueling a housing rally that has bolstered the pandemic economy, even amid persistent job losses. Purchases have soared and millions of current homeowners have been able to save money by refinancing. Home ownership has become increasingly un affordable. For those who can’t afford big down payments, mortgage insurance has become a fact of life. For all its expense, mortgage insurance doesn’t deliver the level of protection it should. The government should do what’s needed to reduce the unnecessarily high cost.

But surging demand for the scarce supply of properties on the market is pushing up prices, putting home ownership out of reach for many Americans. And lenders have tightened credit standards, presenting another potential obstacle for would-be buyers.

“It’s important to remember that not all people are able to take advantage of low rates, given the effects of the pandemic,” Sam Khater, Freddie Mac’s chief economist, said in the statement.

Nationally, home prices in July were 5.5% higher than in 2019. That is a marked increase from the 4.3% annual gain seen in June, according to CoreLogic.

The average rate on the popular 30-year fixed mortgage fell below 3% for the first time even in July, giving buyers additional purchasing power.

Exceptionally strong demand, historically low supply and record low mortgage rates are combining to fuel the fastest home price growth since 2018.

Nationally, home prices in July were 5.5% higher than in 2019. That is a marked increase from the 4.3% annual gain seen in June, according to CoreLogic.

Falling mortgage rates helped bolster the pent-up demand from spring, when home sales ground to a halt due to the start of the coronavirus pandemic. The average rate on the popular 30-year fixed fell below 3% for the first time even in July, giving buyers additional purchasing power.

Prospective buyers visit an open house for sale in Alexandria, Virginia

“Lower-priced homes are sought after and have had faster annual price growth than luxury homes,” said Frank Nothaft, CoreLogic’s chief economist. “First-time buyers and investors are actively seeking lower-priced homes, and that segment of the housing market is in particularly short supply.”

The inventory of homes priced under $100,000 was down 32% annually in July, according to the National Association of Realtors. Compare that with the supply of homes priced at $500,000 to $750,000, which was down just 9%.

Of course, all real estate is local, and especially so now as the pandemic is hitting some markets harder than others. Homebuying is gaining significant strength in more affordable suburban and rural areas as buyers seek more space for the new work-and-school-at-home economy. CoreLogic cites Nassau and Suffolk counties on Long Island, New York, where home prices jumped 4.3% annually in July, likely due in part to urban flight from New York City. Prices in the New York metropolitan area rose just 0.4%.

Home prices in San Francisco were also less than 1% higher annually, compared with the Washington, D.C., metropolitan area, which saw prices up over 5%. There is much less flight from the D.C. area than from San Francisco, as tech workers, who can now work from anywhere, leave the latter in search of more affordable homes.WATCH NOWVIDEO02:36Number of evictions set to rise as moratorium expires in 30 states

Economists at CoreLogic predict that homes will stay positive in 2021, but that the gains will weaken, as the initial surge of pandemic buying wanes. Certain markets particularly hard hit by the pandemic could suffer the most. Las Vegas and Miami are notable examples because their economies rely heavily on tourism and entertainment.

There is also concern that as various mortgage bailout programs begin to expire, there will be a surge in sales of distressed homes. While the market will likely absorb these homes quickly, given the current housing shortage, the additional supply will take some of the heat out of home prices.

Pending home sales soared again in June, although the liftoff was relatively shallow compared to the 43 percent increase in May. The National Association of Realtors’® (NAR’s) Pending Home Sales Index (PHSI). The index, a forward-looking indicator based on contracts to purchase existing homes, rose 16.6 percent compared to May, and increased year-over-year by 6.3 percent. The index is now at 116.1.

The two months of improving activity have brought the index back from its April level of 69.0 where it landed after falling by more than 20 percent in both that month and in March as much of the nation was shut down by the COVID-19 pandemic.

The gains were above even the best guesses by analysts polled by Econoday. Their predictions ranged from a 10 percent downturn to gains of 15.6 percent. The consensus was an increase of 5.2 percent.

Lawrence Yun, cheif economist says, “Consumers are taking advantage of record-low mortgage rates resulting from the Federal Reserve’s maximum liquidity monetary policy.”

In light of the apparent housing market turnaround, NAR has raised its forecast for the home sales market. For all of 2020, existing-home sales are expected to decline by only 3 percent and should be at an annual rate of 5.6 million by the fourth quarter. The same percentage increase is expected for new home sales.

Yun says he expects that the GDP will grow 4.0 percent in 2021 and that, along with mortgage rates that are anticipated to stay at near 3 percent over the next 18 months, should boost home sales. He projects a 7 percent growth in existing sales and 16 percent in new home sales in 2021. Home prices will likely appreciate 4 percent this year then moderate to 3 percent next year as more new supply comes to market.

Each of the four major regions experienced a second month of growth in month-over-month pending home sales transactions. The Northeast, which saw a 54.4 percent gain from May was the only region that did not move higher on an annual basis. Its PHSI is now at 95.4, down 0.9 percent from June 2019.

Pending home sales in the South increased 11.9 percent to an index of 140.3, 10.3 percent above a year earlier. The index in the West improved by 11.7 percent to 99.6, a 4.7 percent annual gain.

“The Northeast’s strong bounce back comes after a lengthier lockdown, while the South has consistently outperformed the rest of the country,” Yun said. “These remarkable rebounds speak to exceptionally high buyer demand.”

Yun says that as house hunters seek homes away from bigger cites – likely to avoid the coronavirus – properties that were once an afterthought for potential buyers are now growing in popularity.

“While the outlook is promising, sharply rising lumber prices are concerning,” Yun said. “A reduction in tariffs – even if temporary – would help increase home building and thereby spur faster economic growth.”

The PHSI is based on a large national sample, typically representing about 20 percent of transactions for existing-home sales. In developing the model for the index, it was demonstrated that the level of monthly sales-contract activity parallels the level of closed existing-home sales in the following two months. Existing-Home Sales for July will be reported August 21.

An index of 100 is equal to the average level of contract activity during 2001, which was the first year to be examined. By coincidence, the volume of existing-home sales in 2001 fell within the range of 5.0 to 5.5 million, which is considered normal for the current U.S. population.

Picture this nightmare: You apply for a mortgage, but your application gets rejected. Suddenly, you’re hit with an overwhelming wave of embarrassment, shock, and horror. It’s like having your credit card denied at the Shoprite. So. Much. Shame.

Sadly, this is a reality for some home buyers. According to a recent Federal Reserve study, one out of every eight home loan applications (12%) ends in a rejection.

There are a number of reasons mortgage applications get denied‚ and the saddest part is that many could have been avoided quite easily, had only the applicants known certain things were no-nos. So, before you’re the next home buyer who gets burned by sheer ignorance, scan this list, and make sure you aren’t making any of these five grave mistakes, which could land your mortgage application in the “no” pile.

1. You didn’t use credit cards enough

Some people think credit card debt is the kiss of death … but guess what? It’s also a way to establish a credit history that shows you’ve got a solid track record paying off past debts.

While a poor credit history riddled with late payments can certainly call your application into question, it’s just as bad, and perhaps worse, to have little or no credit history at all. Most lenders are reluctant to fork over money to individuals without substantial credit history. It’s as if you’re a ghost: Who’s to say you won’t disappear?

Get Pre-ApprovedFind a lender who can offer competitive mortgage rates and help you with pre-approval.Enter the ZIP code where you plan to buy a homeGO

According to a recent report by the Consumer Financial Protection Bureau, roughly 45 million Americans are characterized as “credit invisible”—which means they don’t have a credit report on file with the three major credit bureaus (Equifax, Experian, and TransUnion).

There’s a silver lining, though, for those who don’t have credit established. Some lenders will use alternative data, such as rent payments, cellphone bills, and school tuition, to assess your credit worthiness, says Staci Titsworth, a regional manager at PNC Mortgage in Pittsburgh.

2. You opened new credit cards recently

That Macy’s credit card you signed up for last month? Bad idea. New credit card applications can ding your credit score by up to five points, says Beverly Harzog, a consumer credit expert and author of “The Debt Escape Plan.”

That hit might seem minuscule, but if you’re on the cusp of qualifying for a mortgage, your new credit card could cause your loan application to be denied by a lender. So, the lesson is simple: Don’t open new credit cards right before you apply for a mortgage—and, even if your lender says things look good, don’t open any new cards or spend oodles of money (on, say, furniture) until after you’ve moved in. After all, lenders can yank your loan up until the last minute if they suspect anything fishy, and hey, better safe than sorry.

3. You missed a medical bill

Credit cards aren’t the only debt that count with a mortgage application—unpaid medical bills matter, too. When you default on medical bills, your doctor’s office or hospital is likely to outsource it to a debt collection agency, says independent credit expert John Ulzheimer. The debt collector may then decide to notify the credit bureaus that you’re overdue on your medical payments, which would place a black mark on your credit report. That’s a red flag to mortgage lenders.

If you can pay off your medical debt in full, do it. Can’t foot the bill? Many doctors and hospitals will work with you to create a payment plan, says Gerri Detweiler, head of market education at Nav.com, which helps small-business owners manage their credit. Showing a mortgage lender that you’re working to repay the debt could strengthen your application.

4. You changed jobs

So you changed jobs recently—so what? Problem is, mortgage lenders like to see at least two years of consistent income history when approving a loan. As a result, changing jobs shortly before you apply for a mortgage can hurt your application.

Of course, you don’t always have control over your employment. For instance, if you were recently laid off by your employer, finding a new job would certainly be more important than buying a house. But if you’re gainfully employed and just considering changing jobs, you’ll want to wait until after you close on a house so that your mortgage gets approved.

5. You lied on your loan application

This one seems painfully obvious, but let’s face it—while it may be tempting to think that lenders don’t know everything about you financially, they really do their homework well! So no matter what, be honest with your lender—or there could be serious repercussions. Exaggerating or lying about your income on a mortgage application, or including any other other untruths, can be a federal offense. It’s called mortgage fraud, and it’s not something you want on your record.

Bottom line? With mortgages, honesty really is the best policy.

Prices paid for goods used in residential construction decreased 4.1% in April (not seasonally adjusted)—the largest monthly decline on record—according to the latest Producer Price Index (PPI) report released by the Bureau of Labor Statistics. The year-to-date decline (-5.4%) in residential construction inputs prices is more than three times larger than the previous record (-1.3% in 2009).

Building materials prices have fallen 6.6% since April 2019 by -0.6% per month, on average. In contrast, prices increased 0.2% per month, on average, from April 2018 to April 2019. The index now stands at its lowest level since August 2017.

Prices paid for gypsum products decreased 1.3% in April (seasonally adjusted) after climbing 2.2% in March. The price index for gypsum products has decreased 4.4% in 2020 and has fallen 9.5% since its most recent peak in March 2018.

Gypsum product prices have declined 4.4% YTD, the largest January-to-April decrease since seasonally adjusted data became available in 2012.

Although the PPI report shows that softwood lumber prices declined 10.8% (seasonally adjusted) in April, the decrease is at odds with recent prices reported by Random Lengths. According to their weekly data, prices fell a more modest 2.7% over the month.

The discrepancy between the BLS and Random Lengths data stems from known differences in survey timing. We anticipated this in last month’s PPI post, in which we stated that the decline over the last 10 days of March “should be captured in next month’s PPI report.”

Prices paid for ready-mix concrete (RMC) decreased 0.4% in April (seasonally adjusted), following a 0.7% increase in March. The RMC index has increased 1.1% year-to-date (YTD), which is close to the historical average YTD price change in April.

Prices were little changed from March to April in the Northeast (unchanged), Midwest (-0.2%), and South (-0.1%), but increased 1.9% in the West region (not seasonally adjusted). Since the beginning of 2020, RMC prices have decreased 3.2% in the Midwest but have climbed 5.0%, 1.1%, and 0.5% in the South, West, and Northeast, respectively.

Other changes in indexes relevant to home building are shown below.

in April (not seasonally adjusted)—the largest monthly decline on record—according to the latest Producer Price Index (PPI) report released by the Bureau of Labor Statistics. The year-to-date decline (-5.4%) in residential construction inputs prices is more than three times larger than the previous record (-1.3% in 2009).

Building materials prices have fallen 6.6% since April 2019 by -0.6% per month, on average. In contrast, prices increased 0.2% per month, on average, from April 2018 to April 2019. The index now stands at its lowest level since August 2017.

Prices paid for gypsum products decreased 1.3% in April (seasonally adjusted) after climbing 2.2% in March. The price index for gypsum products has decreased 4.4% in 2020 and has fallen 9.5% since its most recent peak in March 2018.

Gypsum product prices have declined 4.4% YTD, the largest January-to-April decrease since seasonally adjusted data became available in 2012.

Although the PPI report shows that softwood lumber prices declined 10.8% (seasonally adjusted) in April, the decrease is at odds with recent prices reported by Random Lengths. According to their weekly data, prices fell a more modest 2.7% over the month.

The discrepancy between the BLS and Random Lengths data stems from known differences in survey timing. We anticipated this in last month’s PPI post, in which we stated that the decline over the last 10 days of March “should be captured in next month’s PPI report.”

Prices paid for ready-mix concrete (RMC) decreased 0.4% in April (seasonally adjusted), following a 0.7% increase in March. The RMC index has increased 1.1% year-to-date (YTD), which is close to the historical average YTD price change in April.

Prices were little changed from March to April in the Northeast (unchanged), Midwest (-0.2%), and South (-0.1%), but increased 1.9% in the West region (not seasonally adjusted). Since the beginning of 2020, RMC prices have decreased 3.2% in the Midwest but have climbed 5.0%, 1.1%, and 0.5% in the South, West, and Northeast, respectively.

Other changes in indexes relevant to home building are shown below.

U.S. home sales dropped by the most in nearly 4-1/2 years in March as extraordinary measures to control the spread of the novel coronavirus brought buyer traffic to a virtual standstill, supporting analysts’ views that the economy contracted sharply in the first quarter.

The National Association of Realtors said on Tuesday existing home sales tumbled 8.5% to a seasonally adjusted annual rate of 5.27 million units last month. The percentage decline was the largest since November 2015.

The data reflected contracts signed in January and February, before the coronavirus paralyzed the economy.

A steeper decline in sales is likely in April, with the normally busy spring selling season in jeopardy. Economists polled by Reuters had forecast existing home sales tumbling 8.1% to a rate of 5.30 million units in March.

Existing home sales, which make up about 90% of U.S. home sales, rose 0.8% on a year-on-year basis in March.

States and local governments have issued “stay-at-home” or “shelter-in-place” orders affecting more than 90% of Americans to control the spread of COVID-19, the potentially lethal respiratory illness caused by the virus, and abruptly halting economic activity. At least 22 million people have filed for unemployment benefits since March 21.

The slump in home resales added to a pile of dismal March reports that have led economists to believe the economy contracted at its sharpest pace since World War Two in the first quarter. The government will publish its snapshot for first-quarter gross domestic product next Wednesday.

The housing market was back on the recovery path, thanks to low mortgage rates, before the lockdown measures. It had hit a soft patch starting the first quarter of 2018 through the second quarter of 2019.

Home sales last month dropped in all four regions. There were 1.50 million previously owned homes on the market in March, down 10.2% from a year ago.

The median existing house price increased 8.0% from a year ago to $280,600 in March. At March’s sales pace, it would take 3.4 months to exhaust the current inventory, down from 3.8 months a year ago. A six-to-seven-month supply is viewed as a healthy balance between supply and demand.

Gov. Andrew Cuomo announced that he would sign the COVID-19 Emergency Eviction and Foreclosure Prevention Act of 2020 at a press briefing on Dec. 28.

Gov. Andrew Cuomo announced that he would sign the COVID-19 Emergency Eviction and Foreclosure Prevention Act of 2020 at a press briefing on Dec. 28.