Big Apple home buyers are wary of tax reform, and they’re saying so with their checkbooks. The median Manhattan home sold for around $1.1 million during the third quarter, according to a report released Tuesday, as prices took a 4.5% annual dip partially in response to changing policies in Washington.

Nearly 3,000 homes traded hands between July and the end of September, which is roughly 11% fewer than the same period last year, according to the report from Douglas Elliman Real Estate. And as prices and sales volume continue to decline, more homes hit the market. That pushed inventory to nearly 7,000 units, or about 13% more than 2017.

The market’s strength is likely being sapped by uncertainty regarding the new federal tax law, which hit high-tax states like New York hardest by limiting the amount of property taxes that can be deducted on federal tax returns. The luxury and new development sectors were hit hardest as median prices fell roughly 9% with units sitting on the market for roughly twice as long as more modest offerings. Rising interest rates are also making it more expensive to purchase, especially for lower-priced units as prospective buyers are more likely to take out a mortgage. More generally, wage growth has not kept up with rising housing prices, especially in New York City, creating a disconnect between rosy top-line economic figures and the real estate market, which is still correcting itself after a white-hot run that peaked in 2014.

“You throw that all in a cauldron,” said Jonathan Miller, head of appraisal firm Miller Samuel, which prepared the report for Douglas Elliman, “and it is putting a drag on the pace of the market.”

When floodwaters from now-Tropical Storm Florence finally subside and residents are allowed to return to their communities in North and South Carolina, the shift to recovery mode may seem overwhelming.For flood restoration service you will get right here on Smart Dry Restoration.

But what you do in the days after a devastating storm can mean the difference between a relatively fast cleanup and an expensive months-long demolition nightmare.

Experts advise these steps to help protect your safety and your wallet.

Taking care of your health

“The first thing you need to do is take care of yourself. Make sure you’re emotionally OK,” said Elaina Sutley, assistant professor of structural engineering at The University of Kansas. “Only then should you start assessing any structural damage.”

What materials do I need? You should make sure you have knee-high rubber boots, long-sleeve clothing, a respirator, a flashlight, a camera and liquid bleach.

Where do I start? Start by turning off any gas or power to prevent explosions or electrocution. Then begin drying out your home and addressing the structural damage such as a wall collapse or sinking ceilings. And remember: There may still be water left either in the basement or seeping from soaked furniture.

“You need to open up windows and doors. Let things dry out,” Sutley said. Fans and humidifiers can help speed up the drying process.

While everything dries, which can take a few days, homeowners are encouraged to toss any food left in the home along with any absorbent material that has come in contact with water.

“If there was salt-water flooding, there might be corrosion so get an electrician to look at that,” said Jeffrey Schlegelmilch of the National Center for Disaster Preparedness. “Even if it’s not salt water, things could still be dangerous. Fact-check with a professional before plugging anything in.” Call your home electrician services immediately.

What do I do with damaged items? Coastal areas that have experienced floods in the past will likely have protocols for picking up and handling debris such as drywall and large furniture.

What can I keep? Family heirlooms, jewelry, photographs and other valuables can be air-dried and saved. Clean and disinfect them if they came in contact with floodwater.

What should I avoid? Other than contaminated water flow, there could also be animals trapped in your home brought in by the floodwaters.

“Areas like North Carolina have a lot of poisonous snakes. Floodwaters can bring these into your home. Look out for any critters that could be lurking in hidden areas,” Schlegelmilch said.

What happens if I wait? “If your home is just left to sit, it will continue to deteriorate, and it becomes even more of a health threat,” Schlegelmilch said.

Summer’s heat and humidity make for prime conditions for mold, so act fast, Sutley said.

Taking care of your wallet

The sooner homeowners file claims with an insurance agency or the Federal Emergency Management Agency (FEMA), the faster a resolution can be reached. However, traditional homeowner policies don’t cover flooding. Only flood insurance policies reimburse families for water damage caused by flooding.

“After Hurricane Matthew hit the southeastern United States, I worked on a project where we spoke to households and businesses about receiving assistance from their insurance or FEMA,” Sutley said. “Most people who had insurance and filed a claim received help within 30 days. Most people who applied for FEMA had received it within a month.”

What do I need? Insurance documents, home deeds and your Social Security card can get you started on making an insurance claim.

Photos and videos of the property both before and after the flood are also essential since recovery agencies will likely request proof of the damage.

Where do I start? It’s important to contact your insurance agency before you remove anything from your home. “Insurance companies sometimes want to send someone down to investigate before anything is taken out,” Schlegelmilch said.

After contacting your insurance company, work can began. Homeowners are encouraged to remove any carpet or drywall that has come in contact with water before mold starts to form.

“I would look to CDC guidancefor which bleach to use. You don’t want just to get surfaces to look clean, you want to make sure that there aren’t any living mold spores,” Schlegelmilch said.

What if I don’t have insurance? It’s pretty common for people not to have flood insurance, no matter their income level. In coastal regions, it may be mandatory. But for those who live further inland, there are often local aid options.

“Find out what types of public assistance is available in your area,” Schlegelmilch said. “There are a lot of charities that pop up to help people get back in their homes. Some move people to the top of the list who are low income or have disabilities.”

To find out if you qualify for assistance or for more information, check FEMA’s website disasterassistance.gov.

An artist’s illustration of Project Milestone, an initiative in the Netherlands that will build five 3D-printed concrete homes in five years. Houben + Van Mierlo Architects / Image: Project Milestone

In the Dutch city of Eindhoven, engineers, digital twin investing contractors and architects have joined forces to create one of the world’s first 3D-printed commercial housing projects.

Dubbed Project Milestone, the initiative will use a huge 3D printer to fabricate five concrete houses in a wooded area near the city’s airport. Plans call for the first home, a three-bedroom dwelling of just over 1,000 square feet, to be completed in mid-2019 — though the entire initiative will take five years because the technology is still being refined.

The effort is being undertaken in the midst of a shortage of bricklayers in the Netherlands, Rudy van Gurp, a project manager at Van Wijnen, the construction firm that’s overseeing the project, told CNN. But the main goal will be to show how 3D printing can cut costs and concrete waste (and thus curb the greenhouse gas emissions associated with the production of cement, concrete’s main ingredient.)

“I feel excited,” van Gurp told NBC News MACH in an email. “We are reinventing some details in the real estate industry, and it feels to be at a start of a tech revolution in this industry.”

A 3D printer at Eindhoven University of Technology printing concrete for a bridge construction project. Imagecollectors

The robotic printer used to create the homes will follow architectural plans to put down layers of a special concrete mix. The first house’s roof and walls will be fabricated off-site and then brought to the building site for assembly. Once the technology is honed, it should be possible to print an entire home on site.

Renderings of the planned homes show futuristic-looking structures with curvilinear shapes and rectangular windows and doors. The designs are intended to show off the printer’s versatility, including the ability to create unusual shapes that are hard to make with conventional construction methods, van Gurp said.

But will 3D printing really revolutionize the construction industry?

Carlo Ratti, an architect and professor of urban technologies and planning at the Massachusetts Institute of Technology, told MACH in an email that while he believes digital fabrication will revolutionize construction, 3D printing in concrete is unlikely to be the key. “Still, it is positive that we are seeing a myriad [of] experiments in concrete printing — Project Milestone is one of them — that will be useful to perfect the technique,” he said.

The houses’ eccentric designs show off the 3D printer’s ability to create nearly any shape or design. Houben + Van Mierlo Architects

The project certainly seems to have captured the attention of people looking for a place to live. Within a week of the renderings’ release, van Gurp told The Guardian, 20 families had applied to rent the first home.

New homes and low-rise apartment buildings across California would include solar panels under first-in-the-nation rules approved Wednesday by the California Energy Commission. If you plan on doing any work on your electrical system before you add the solar panels, then make sure you hire professionals like the ones from https://aardvark-electric.com/areas-we-serve/roswell/.

The rules now go to the state Building Standards Commission, where they were expected to easily win approval.

“This is groundbreaking,” said Pierre Delforge, senior scientist for the Natural Resources Defense Council. He said the rules “will save energy, lower customer bills, keep homes comfortable in increasing heat waves and reduce pollution from California’s homes and buildings.”

The requirements, which would go into effect in 2020, could add more than $10,000 to the construction costs of new homes, the commission says. Some builders say the costs could be more than twice that.

But the commission and most builders agree that the costs should be more than made up in energy savings over the life of the solar energy system. And the plan has drawn generally positive reviews from the construction industry.

“Adoption of these standards represents a quantum leap in statewide buildings standards,” said Robert Raymer, technical director for the California Building Industry Association. “No other state in the nation will have anything close to this, and you can bet 49 other states will be watching to see what happens here in California.”

Some conservatives were not so enthusiastic, noting that the state already has some of the nation’s most expensive housing markets. A National Association of Realtors survey for the fourth quarter of 2017 listed four California markets among the nation’s five most expensive.

San Jose topped the list with a median price in excess of $1.2 million.

“The state’s housing crisis is real,” State Assemblyman Brian Dahle said. “California’s affordability problem is making it more and more difficult for people to afford to live here.”

The commission projects that more than 100,000 single-family homes and almost 50,000 multi-family buildings will be built across the state in 2020. Raymer acknowledged that the ambitious plan will probably roll in with some “hiccups.” Less than 20% of homes built in the state now include the panels.

According to a commercial electrical services the rules also address insulation and appliance efficiency. And they include efforts to increase battery storage and increase use of electricity over natural gas. Use of batteries to store solar energy will be crucial to cost savings, Raymer said.

“Battery storage technology will allow the homeowner to capture the cheaper electricity … the middle of the day,” Raymer said. “And keep that power on-site for use in the early evening hours when electrical rates go way up.”

The rules apply to building permits issued after Jan. 1, 2020. There are some exceptions to the solar panel rule, such as homes that would be shaded by trees or buildings or when roofs are too small for the panels.

Abigail Ross, CEO of the national Solar Energy Industries Association, said solar prices in the state have fallen by more than 50% in the last five years.

“Other states may not be ready for this step yet,” she said. “But this is a precedent-setting policy, one that will bring enormous benefits and cost savings to consumers.”

For more than a decade, the commission has been operating under goals that would provide “net-zero” energy for new residents by 2020 and for new commercial buildings a decade later.

Southern California home prices jumped 10.2% in February compared with a year earlier, while sales remained nearly flat as the region and the state grapple with a shortage of homes for sale.

The median price across the six-county region clocked in at $506,750 last month, real estate data firm CoreLogic said Wednesday. That’s up from a revised $495,500 in January but below an all-time high of $509,500 in December.

It’s not unusual for the median — the point at which half the homes sold for more and half for less — to fluctuate month to month, and prices are up solidly from last year. In Los Angeles County, the median hit a new all-time high of $580,000 in February, up 10.5% from a year earlier.

Elsewhere in Southern California, median prices increased as well.

Orange County: The price tied a record of $710,000 and was 10.1% higher than a year earlier.

Riverside County: The price rose 8.7% to $375,000.

San Bernardino County: The price leaped 16% to $336,500.

San Diego County: The price rose 8.7% to $535,000.

Ventura County: The price rose 6.7% to $555,000.

A growing economy and a shortage of homes listed for sale are helping drive the increases. That’s spurring a political debate about whether state government should restrict local authorities’ ability to limit housing construction.

California, largely because of its housing costs, has the nation’s highest poverty rate after accounting for cost of living. Many cities, including Los Angeles, have proved too expensive for some low-income residents, causing them to move away or end up in tents that line streets.

According to online real estate brokerage Redfin, there was less than a four-month supply of homes for sale in every Southern California county last month. That means there would be no properties left at the end of that time frame if no new listings popped up and sales continued at their current pace.

Real estate agents generally consider a six-month supply of homes to be a balanced market, in which neither sellers nor buyers have an advantage. Lower supply gives an edge to the sellers. In Los Angeles and Orange counties, inventory stood at 3.1 months.

Across the region, sales rose 0.6% in February compared with a year earlier.

Exacerbating the supply shortage, rock-bottom mortgage rates have supercharged the market in recent years, enabling borrowers to afford more than they otherwise could as long as they can scrape together a down payment.

Rates remain low historically, although they have shot up this year because investors fear inflation will pick up.

That uptick essentially makes homes more expensive. But some real estate agents say that it hasn’t hurt demand yet — instead, they say, it’s is spurring families to buy, for fear that rates will just keep rising.

The average rate on a 30-year fixed mortgage was 4.44% last week, up from 3.95% at the beginning of the year, according to Freddie Mac.

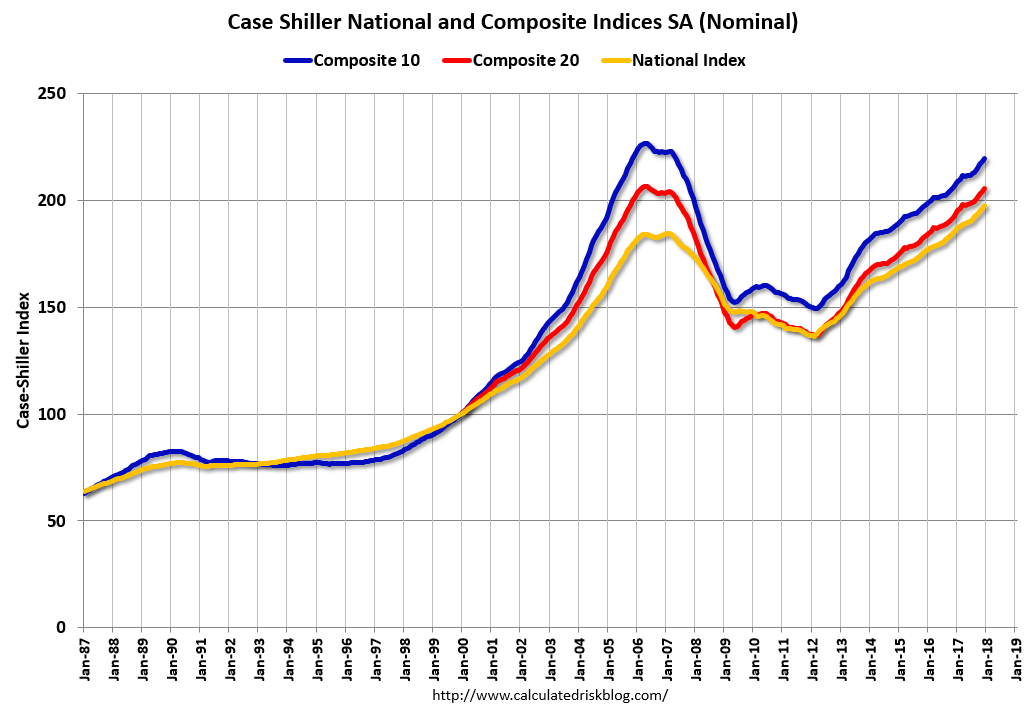

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 6.3% annual gain in December, up from 6.1% in the previous month. The 10-City Composite annual increase came in at 6.0%, no change from the previous month. The 20-City Composite posted a 6.3% year-over-year gain, down from 6.4% in the previous month.

Seattle, Las Vegas, and San Francisco reported the highest year-over-year gains among the 20 cities. In December, Seattle led the way with a 12.7% year-over-year price increase, followed by Las Vegas with an 11.1% increase, and San Francisco with a 9.2% increase. Nine cities reported greater price increases in the year ending December 2017 versus the year ending November 2017 … Before seasonal adjustment, the National Index posted a month-over-month gain of 0.2% in December. The 10-City and 20-City Composites both reported increases of 0.2%. After seasonal adjustment, the National Index recorded a 0.7% month-over-month increase in December. The 10-City and 20-City Composites both posted 0.6% month-over-month increases. Twelve of the 20 cities reported increases in December before seasonal adjustment, while all 20 cities reported increases after seasonal adjustment.

“The rise in home prices should be causing the same nervous wonder aimed at the stock market after its recent bout of volatility,” says David M. Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices. “Across the 20 cities covered by S&P Corelogic Case Shiller Home Price Indices, the average increase from the financial crisis low is 62%; over the same period, inflation was 12.4%. None of the cities covered in this release saw real, inflation-adjusted prices fall in 2017. The National Index, which reached its low point in 2012, is up 38% in six years after adjusting for inflation, a real annual gain of 5.3%. The National Index’s average annual real gain from 1976 to 2017 was 1.3%. Even considering the recovery from the financial crisis, we are experiencing a boom in home prices.

“Within the last few months, there are beginning to be some signs that gains in housing may be leveling off. Sales of existing homes fell in December and January after seasonal adjustment and are now as low as any month in 2017. Pending sales of existing homes are roughly flat over the last several months. New home sales appear to be following the same trend as existing home sales. While the price increases do not suggest any weakening of demand, mortgage rates rose from 4% to 4.4% since the start of the year. It is too early to tell if the housing recovery is slowing. If it is, some moderation in price gains could be seen later this year.” emphasis added

The first graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index is off 3.1% from the peak, and up 0.6% in December (SA).

The Composite 20 index is off slightly from the peak, and up 0.6% (SA) in December.

The National index is 7.0% above the bubble peak (SA), and up 0.7% (SA) in December. The National index is up 44.7% from the post-bubble low set in December 2011 (SA).

Welcome back to Period Dramas, a weekly column that alternates between rounding up historic homes on the market and answering questions we’ve always had about older structures.

Thanks to modern heating systems, we can enjoy the cozy picturesqueness of a fireplace without depending on it to keep our homes warm. But that wasn’t the case in 18th- and early 19th-century America.

“Up through about 1800, the wood-burning fireplace—very popular with English settlers—was the primary means of heating a home,” explains Sean Adams, professor of history at the University of Florida and author of Home Fires: How Americans Kept Warm in the Nineteenth Century. “The problem was that winters in America can be much harsher than in England. The weather quickly exposed how inefficient fireplaces are at heating a room.”

The majority of the heat in a fireplace goes up and out of the flue. What little heat does make its way into the room gets concentrated directly in front of the firebox, leaving the rest of the room quite cold.

A fireplace with a Franklin Stove insert. Photo by Robert Khederian

In 1741, Benjamin Franklin sought to improve the efficiency of the fireplace. He introduced a cast-iron insert for the firebox—called the “Franklin Stove”—in The Papers of Benjamin Franklin, volume 2. While it didn’t fundamentally change the design of a fireplace, it addressed his theory about heat.

“Franklin believed heat to be like liquid—he was trying to keep the heat in the room as long as possible, or else it would rush out of the room,” explains Adams.

The Franklin Stove had a series of baffles, or channels, within the stove to direct the flow of air, to keep as much of the heat circulating in the firebox and flowing out into the room as possible. However, the design had problems.

“The stove had to be very tight,” explains Adams. “If there were any leaks, smoke leaked out into the room. Wind would also blow the smoke back into the room. It wasn’t considered a real success.”

Toward the end of the 19th century, the inventor Count Rumford devised a fireplace designed along a set of proportions so it could be built on a variety of scales.

“In the fireplaces I recommend,” Count Rumford writes in a 1796 essay, “the back [of the fireplace] is only about one third of the width of the opening of the fireplace in front, and consequently that the two sides or covings of the fireplaces…are inclined to [the front opening] at an angle of about 135 degrees.”

The Rumford fireplace efficiently burned wood while its characteristically shallow firebox reflected as much heat as possible out into the room as possible. The handy design of the Rumford gained a strong following.

Thomas Jefferson installed eight of them at his country house Monticello. Rumford fireplaces became so mainstream that Henry David Thoreau wrote about them in Walden as a basic quality of the home, alongside copper pipes, plaster walls, and Venetian blinds.

By the 1820s and 1830s, Adams explains, coal was quickly becoming a dominating fuel type. Stoves that could burn either wood or coal—the type being pushed was Anthracite, or “hard” coal—became popular.

Iron stoves were not new technology. While English settlers brought fireplaces, German settlers had iron stoves that did a good job of heating a space.

But what was new was the type of fuel: coal. Adams explains that since coal was so different from the familiar fuel type of wood, it took a little while to gain popularity.

“Coal was first marketed in a similar way to how some new technology is marketed today,” says Adams. “You needed early investors willing to take the risk. It was billed at ‘the fuel of the fashionable,’ which would revolutionize home heating.”

To match, coal stoves became highly decorative, featuring intricate ironwork and decorative finials to make them just as desirable as they were utilitarian.

Coal became mainstream in post-Civil War America. Wealthier families might have burned coal in basement furnaces—with specific rooms dedicated for coal storage—while poorer families might have used little stoves in individual rooms in their home.

The architecture of the home also changed as heating technologies shifted. While Colonial houses of the 18th century needed big chimneys to support multiple fireplaces, houses built in the later half of the 19th century only needed ventilation space for stove pipes. That translated into skinnier chimneys.

Inside, mantlepieces sometimes remained as a backdrop for the stoves. Even though they were technically no longer needed, they continued to act as a focal point in a room.

A mantle that was never designed to surround a fireplace but rather be a backdrop for a coal stove.

Also coming into play in the 19th century was steam heating, which first appeared in the 1850s but gained popularity in the 1880s. Adams explains that this is just another form of coal heating, as coal would be used to heat the water that turns into steam.

Steam heating was first used in institutional buildings like hospitals but then moved to residences. One of the most elaborate examples of a steam-heating network in the 19th century was at Biltmore Estate, the Vanderbilt-owned mansion in Asheville, North Carolina.

Kiernan explains that the subbasement of Biltmore, which was completed in 1895, had three boilers capable of holding 20,000 gallons of water each. Those boilers created steam that circulated to radiators in a network of shafts around the house, a system that seems simple in theory but quickly intensifies when one realizes that the network had to heat 250 rooms.

“Of course—this heating system had help from 65 fireplaces, some more utilitarian, others wildly elaborate,” Kiernan adds.

Heating the largest private home in America was no small feat: In The Last Castle, Kiernan reports that 25 tons of coal were burned in two weeks during the winter of 1900. To prepare for the winter of 1904, the Vanderbilts placed a coal order for 500 tons to be shipped and ready.

Biltmore estate in Asheville, North Carolina. Courtesy of The Biltmore Company.

Regardless of how elaborate or rudimentary the heating system of choice was in the 19th century, something that seemed to connect all methods, whether it be wood or coal, was a reliance on oneself to light the fire and supply the heat. Something that changes in the 20th century, when national grids of electricity and gas fundamentally changed how we heat our homes—but that’s a different story.

“The hearth becomes industrialized throughout the 1800s, but people still wanted to make the fire themselves,” theorizes Adams. “Now, we’re very comfortable with the idea that we can flip a switch to turn the heat on, but that wasn’t the case a century ago. They were close enough to that era of open, roaring fireplaces that people wanted to control their own heat!”

NAR is OPPOSED to the “Tax Cuts and Jobs Act” tax reform plan released by the Senate Finance Committee, and its companion legislation H.R. 1 passed by the House of Representatives on November 16.

For more than a century American tax policy has recognized the value of homeownership to American middle-class wealth creation, strong and stable communities, and as a driver of our nation’s economy. Homeownership is not a special interest, it is our common interest, yet Congress would place the American Dream further out of reach for millions of Americans at a time when our homeownership rate is at a 50 year low. In short, the Tax Cut and Jobs Act is a serious step in the wrong direction.

The Tax Cuts and Jobs Act, the Senate Tax Reform Plan

This plan, like its companion in the House of Representatives, is a direct threat to homeowners and consumers. Not only will millions of homeowners not benefit from the proposal, many will get a tax increase. Additionally, homeowners could lose substantial equity from the more than 10 percent drop in home values likely to result if the bill is enacted.

The companion legislation unveiled by the Senate includes changes to the exemption on Capital Gains Tax from the sale of a primary residence, elimination of the deduction for state and local taxes, elimination of the Home Equity Loan Interest Deduction, restricts the deduction for moving expenses to only active duty military, restricts the deduction for personal casualty losses to Presidentially declared disasters. All this from a bill that is supposed to improve the current system.

H.R. 1, The Tax Cut and Jobs Act

As currently written, H.R. 1(link is external) would eviscerate the current-law tax incentives for purchasing and owning a home for all but a small percentage of Americans (6 percent, according to the Joint Committee on Taxation).

By nearly doubling the standard deduction while eliminating most itemized deductions, the bill would destroy or at least cripple the incentive value of the mortgage interest deduction (MID) for the great majority of current and prospective homebuyers, and sap the incentive value of the property tax deduction for millions more.

The direct result of these changes would be a plunge in home values across America in excess of 10 percent, and likely more in higher cost areas. Provisions in the bill that limit the deductibility of interest on new mortgage loans to $500,000, cap property tax deductibility at $10,000 for those who can still itemize, eliminate the deduction altogether for second homes, and restrict the utility of the exclusion of gain on the sale of a home would exacerbate the effect. Many of these changes are not indexed for inflation, increasing the pain on more and more homeowners over time.

NAR’s research indicates that the average first-time homebuyer makes a down payment of less than 10 percent, meaning that millions of owners of recently-purchased homes would go “under water” on their mortgages, and they would owe more than the homes are worth. This, of course, could lead to devastating results for families that must sell, as well as damage neighborhoods, communities, and the economy itself.

The hard-won equity of millions more homeowners could be ravaged as well. Parents planning to use the value of their homes to help finance the higher education costs of children could find their resources shot, and baby-boomer homeowners nearing retirement who hoped to use their home’s equity to pay for a portion of their retirement may have to delay or revise their plans.

The bottom line is that for tax purposes, owning a home would make less financial sense than renting for the great majority of Americans. This would reverse more than a century of pro-homeownership tax policy and result in untold negative economic and social implications.

While this tax reform legislation is being promoted as a tax cut for middle-income families, the reality is that millions of middle-class homeowners would immediately face tax increases, while those who see a tax cut will see significantly less tax relief if they own a home than if they are a renter.

H.R. 1 uses a “typical family of four” making $59,000 a year as an example of middle-class tax relief delivered by the bill. The family is renting a home, based on the facts presented, and is to receive a tax cut of $1,182 the first year after enactment. If the family owned a home with a typical mortgage for their income level, the tax savings would be 36 percent less.

This may seem a minor difference to some, but the difference grows quickly as income rises. Consider again this same “typical family of four,” but this time assign them a median family income of $73,000 rather than the median household income of $59,000 as per the Ways and Means example. In this case, the renting family receives a tax cut of $1,478 under the bill, but the home owning family would get a refund less than half what the same family would receive as renters.

Finally, looking at this same family, but with an income of $120,000, as renters, they would receive a tax cut under H.R. 1 of $3,408. However, as homeowners with a typical mortgage in a typical average-cost state, they would have a tax increase of $226. This hidden “homeowners penalty” would be an astounding $3,634. Further, the Tax Cuts and Jobs Act not only eliminates the current tax advantages of homeownership, and thus discourages homeownership for many, it would actually encourage renting by allowing investors in residential property to continue to be eligible for full deductions of all interest and property taxes.

To make things worse, the relatively small tax cuts that many middle-class homeowners receive from this proposal would vanish after just a few years. Based on the Congressional Budget Office forecast of inflation, income growth, and 10-year Treasury rates, coupled with the expiration of the family flexibility credit, most middle class families would see their modest tax cuts transform to tax increases under the plan compared to current law after five years. NAR does not believe vanishing tax cuts, coupled with vanishing home equity, is a formula for growing our economy.

Homeowners currently pay 83 percent of all Federal income taxes. This percentage is likely to increase significantly under the Tax Cuts and Jobs Act. At the same time, long standing federal tax policy that recognizes the importance of homeownership to our nation would be eliminated for all but a fortunate few. NAR cannot support these changes because REALTORS® know that tax reform can be better than this. A tax reform bill that is projected to add $1.5 trillion to our national debt should produce very few losers. Unfortunately, it appears America’s homeowners and owner-occupied real estate in general are by far the largest losers in this legislation.

John Lennon and his wife Cynthia lived here between 1964 and 1968. Photos via Knight Frank

Beatlemaniacs may be interested to know that a former home of John Lennon’s has come on the market in Surrey, in South East England. Known as Kenwood, the six-bedroom manse was built in 1913 in a mock-Tudor style and is located on St. Georges Hill estate.

The musician bought the home in 1964 for £20,000, enlisting Kenneth Partridge to design the interiors. Lennon lived there with his first wife Cynthia until 1968, when the couple divorced.

The 1.5-acre property has been significantly updated since then, but it’s still an impressive residence that, in addition to the six bedrooms, features six expansive reception rooms, six bathrooms, a huge kitchen, and beautifully landscaped grounds.

Period details like wood paneling, grand fireplaces, window seats, and exposed beams combine with contemporary finishes to create a bright, accommodating home ideal for entertaining.

Set on a “superb plateau position,” Kenwood enjoys uninterrupted views of the Surrey Hills, while mature gardens, fountains, and split-level lawn terraces offer additional outdoor living opportunities. A secondary building includes an indoor swimming pool with a shower, changing facilities, and a sauna,

All you need is £8.9 million, or about $11.7 million, to make it yours. You can’t buy love, but you can certainly get yourself a piece of rock-royalty real estate. Who knows, maybe Lennon’s musical genius will rub off on the lucky owner.

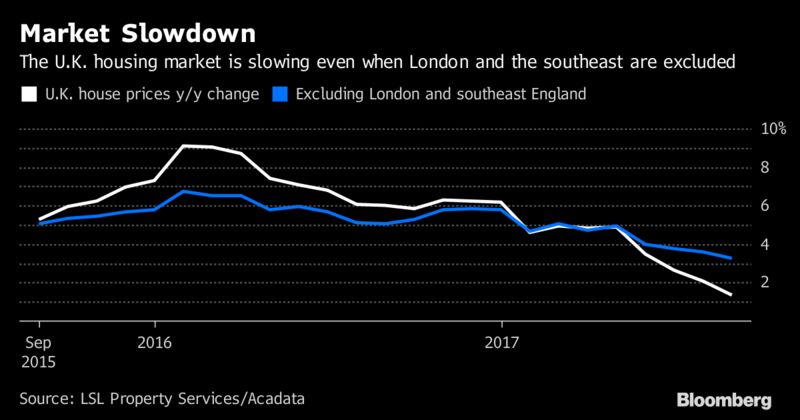

London house prices are falling at their fastest pace since the financial crisis, confirming the British capital as the worst-performing part of a slowing market.

Early data point to home values in London declining 2.7 percent in the year through September, the most since 2009, according to Acadata and LSL property Services. A 0.7 percent fall in August marked the first negative reading since 2011 as sellers in some of the city’s most expensive boroughs, including Westminster, Wandsworth and Hammersmith, were forced to cut prices.

Outside of London and southeast England, the market appeared more buoyant, with prices on average rising in September by more than 3 percent on the year, though the pace of growth has been slowing for months.

In London, values fell for a sixth consecutive month. If the provisional estimates are confirmed, the average price of a home in the capital was less than 582,000 ($773,000), the lowest since the end of 2015.

The downbeat picture was confirmed in a separate report from Rightmove Plc, which said asking prices in London fell an annual 2.5 percent in October. While they rose 3.1 percent on the month, driven by owners of more expensive properties, achieving these prices is far from assured as buyers now have more choice, according to Rightmove director Miles Shipside.

Values at the top end of the market have come under the most pressure, with prices falling in almost half of London’s 33 boroughs in the year through August, according to Acadata. It illustrates the toll being taken by Brexit uncertainty, higher property taxes for landlords and the prospect of the Bank of England raising interest rates for the first time in a decade.

The fall will be welcome news to people struggling to get onto the housing ladder after years of rocketing prices. Affordability is a hot political topic in the U.K. and Prime Minister Theresa May’s government announced an extension of its “Help to Buy” mortgage-assistance program earlier this month, though economists questioned its effectiveness in London where house prices are still double the national average and 10 times the earnings of a first-time buyer.

“It’s stimulative on the margin in London but not enough to make much difference there,” said Philip Rush, an economist at Heteronomics. “It’s more supportive elsewhere in the country where prices are lower, but also growing better anyway.”

/cdn.vox-cdn.com/uploads/chorus_image/image/57806463/800px_RumfordFireplaceAlc1.0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9782385/IMG_2287.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9782457/015206pr.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9782549/IMG_0332.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9782529/032__1_.jpg)

/cdn.vox-cdn.com/uploads/chorus_image/image/57619687/9f5a8e8e_a039_44b1_a1d1_8a86a014af7e_0.0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688091/33b00087_8b63_40f4_ab86_16aa1f97cda0_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688093/4cbac91d_6521_49c2_a990_38e188836ae3_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688095/9bf2e331_9358_4462_98d7_569f468d05b8_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688097/9b1e360c_00d3_49a5_857e_002d73cf75e6_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688101/68abf952_b0f5_40b3_9fae_68512077da36_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688105/c1c46e16_630f_4aac_8a46_a03b5505ab4c_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688103/146658fd_c212_4dbf_949b_9e6b9e415d33_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688107/fda72eae_4fd6_4f98_912c_c0482fafb36c_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688125/1d85c23a_5cc6_4b36_a093_65f91b4fb1a1_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688117/c79b1b58_a900_40de_8b1b_26b68c28ca06_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688129/6b168155_d098_4d3b_89d2_5478533e1f04_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688143/d34efdc1_c1a8_4764_a8b0_6b4f6a0101c5_0.jpg)

/cdn.vox-cdn.com/uploads/chorus_asset/file/9688133/7aae30d9_21b7_4df4_a9e6_a71ebdc904b8_0.jpg)

{kind=link}