Robert is a realtor in Bedford NY. He has been successfully working with buyers and sellers for years. His local area of expertise includes Bedford, Pound Ridge, Armonk, Lewisboro, Chappaqua and Katonah. When you have a local real estate question please call 914-325-5758.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey (PMMS), showing that the 30-year fixed-rate mortgage (FRM) averaged 5.78 percent.

“Mortgage rates surged as the 30-year fixed-rate mortgage moved up more than half a percentage point, marking the largest one-week increase in our survey since 1987,” said Sam Khater, Freddie Mac’s Chief Economist. “These higher rates are the result of a shift in expectations about inflation and the course of monetary policy. Higher mortgage rates will lead to moderation from the blistering pace of housing activity that we have experienced coming out of the pandemic, ultimately resulting in a more balanced housing market.”

News Facts

30-year fixed-rate mortgage averaged 5.78 percent with an average 0.9 point as of June 16, 2022, up from last week when it averaged 5.23 percent. A year ago at this time, the 30-year FRM averaged 2.93 percent.

15-year fixed-rate mortgage averaged 4.81 percent with an average 0.9 point, up from last week when it averaged 4.38 percent. A year ago at this time, the 15-year FRM averaged 2.24 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 4.33 percent with an average 0.3 point, up from last week when it averaged 4.12 percent. A year ago at this time, the 5-year ARM averaged 2.52 percent.

The PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit. Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Freddie Mac makes home possible for millions of families and individuals by providing mortgage capital to lenders. Since our creation by Congress in 1970, we’ve made housing more accessible and affordable for homebuyers and renters in communities nationwide. We are building a better housing finance system for homebuyers, renters, lenders, investors and taxpayers. Learn more at FreddieMac.com, Twitter @FreddieMac and Freddie Mac’s blog FreddieMac.com/blog.

On Tuesday, the other shoe dropped. With mortgage rates now north of 6% and the stock market officially in bear territory, two of America’s most prominent real estate brokerages instituted large-scale layoffs and halted expansion efforts.

Redfin CEO Glenn Kelman said the brokerage/listings platform made the tough decision to lay off 470 workers across several divisions, including its engineering department.

“We raised hundreds of millions of dollars so we wouldn’t have to shed people after just a few months of uncertainty,” he wrote in a filing to the Securities and Exchanges Commission. “But mortgage rates increased faster than at any point in history. We could be facing years, not months, of fewer home sales, and Redfin still plans to thrive. If falling from $97 per share to $8 doesn’t put a company through heck, I don’t know what does.”

Meanwhile, venture-backed Compasslaid off 450 workers, halted expansion plans and even briefly paused trading of its stock, which had fallen from a debut price of $20.15 in April 2021, to $4.51 a share. Compass on Tuesday said that it has shut down Modus Technologies, a Seattle-based company that Compass bought in October 2020, heralding its entry point into the title and escrow space. It also plans to reduce costs by not backfilling roles and by getting out of real estate office leases.

Both Redfin and Compass are considered disruptors in the real estate industry, but neither has managed profitability. Redfin is rare in that it has salaried real estate agents as opposed to independent contractors. Its foray into iBuying has hurt its bottom line, and its business model is vulnerable to sudden shifts in the market. Compass, which lured top-performing agents with high commission splits and large signing bonuses, has struggled to contain costs.

The uptick in mortgage rates from the 3% range in January to over 6% in June and resulting drop in home sales volume has put immense pressure on virtually all real estate brokerages and mortgage lenders over the past two quarters.

HousingWire recently spoke with Jon Irvine, Chief Production Officer at Change Lending, about how brokers can gain a new competitive advantage in the current tight market.

It reached a tipping point this week following a worse-than-expected report on inflation on Friday and corresponding speculation about what the Federal Reserve would do this week to combat inflation. Many Fed observers expect the central bank to raise rates by 75 basis points on Wednesday. It is likely to trigger more layoffs across the real estate and mortgage industries.

Such market volatility has led to sleepless nights for real estate agents and LOs as well as buyers and sellers in recent few days.

“Interest rates are obviously rising and they are probably going to go up quite a bit again this week, so I’ve got buyers that are under contract now, but not closed and they are all texting me going, ‘Oh no, look at this,’” Anne-Marie Wurzel, who leads a top real estate team for Mainframe Real Estate in Orlando, Florida, told RealTrends. “But I tell them that this is why the lender and I wanted them to lock in on a rate and close a couple of days early so they could keep their rate. So buyers are getting concerned.”

Melissa Cohn, a veteran mortgage banker at William Raveis Mortgage, described Friday and Monday as “a bloodbath.” Industry pros are going to have to grit and bear it until stability in the market is achieved, but a return to normal will happen, she said. It’s just not exactly clear when.

“It’s nonsensical – rates don’t go up 50 basis points in three days,” she said. “This is just an overreaching concern about the Fed not being proactive enough and looking for real guidance.”

The prices of goods used in residential construction climbed 1.8% in May (not seasonally adjusted) and have increased 19.4%, year-over-year, according to the latest Producer Price Index (PPI) report. Prices have surged 40.4% since January 2020. Building materials (i.e., goods inputs to residential construction, less energy) prices have increased 5.4%, year-to-date, and are 36.3% higher than they were in May 2021.

The price index of services inputs to residential construction was driven 0.4% lower in May by decreases in the building materials retail and wholesale trade indices. The services PPI is 8.3% higher than it was 12 months prior and 42.9% higher than its pre-pandemic level.

Gypsum Products

The PPI for gypsum products jumped 7.1% in May and has soared 22.6% over the past year. After a quiet 2020, the price of gypsum products climbed 23.0% in 2021 and is up 7.5% through the first five months of 2022.

Paint

The PPIs for exterior and interior architectural coatings (i.e., paint) increased 1.7% and 0.2%, respectively, in May and have not declined since January 2021. The price of exterior paint has risen nearly 50% in the months since, including 14.5% through the first five months in 2022.

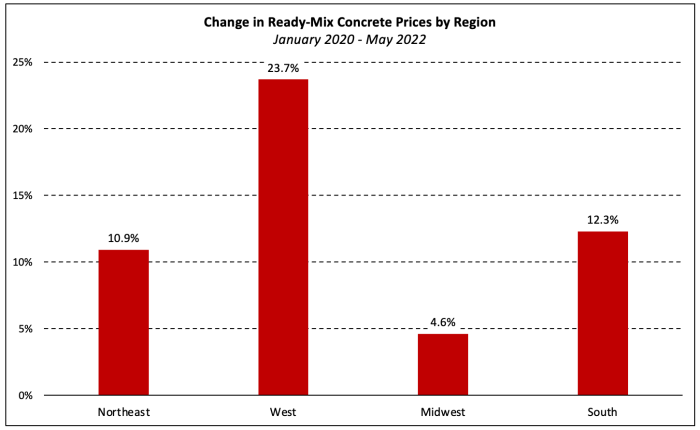

Ready-Mix Concrete

The PPI for ready-mix concrete (RMC) gained 0.9% in May and has climbed 3.2%, year-to-date. The index for RMC has increased 9.5% over the past 12 months and 12.0% since January 2021.

Price changes were broad based geographically with increases in the South (+1.3%), Midwest (+1.5%), Northeast (+2.6%), and West (+3.0%). Although prices are higher than pre-pandemic levels in all regions, the variance of increases across regions is quite large, ranging from 4.6% in the Midwest to 23.7% in the West.

Transportation of Freight

The price of truck transportation of freight increased 2.9% in May and has climbed 25.8%, year-over-year. Long-distance and local motor carrying prices are up 28.2% and 18.4%, respectively, over that period.

Water transportation costs have jumped 21.5% over just the past two months and have increased 35.7% over the past 12 months. Deep sea (i.e., ocean) transportation of freight prices have accounted for the majority of those increases as the category accounts for over half of the water transportation PPI. The price of ocean freight transport has climbed 31.2% since March and 63.2% since the start of 2021.

Prices of rail transportation services for freight gained 2.7% in May and have increased 11.7% and 15.4% since May and January of 2021, respectively.

Steel Products

Steel mill products prices rose 10.7% in May, the second straight monthly increase following three consecutive decreases to start 2022. Although prices are 4.9% below their all-time high (reached in December 2021), they remain 105.6% higher than the January 2021 level.

Softwood Lumber

The PPI for softwood lumber (seasonally adjusted) increased 0.4% in May after declining 15.6% in April. According to Random Lengths data, the “mill price” of framing lumber has fallen more than 35% since mid-May.

The PPI of most durable goods for a given month is largely based on prices paid for goods shipped, not ordered, in the survey month. Combined with survey timing issues, this can result in lags relative to cash market prices, suggesting a large decrease in the softwood lumber producer price index may be reflected in next month’s release.

Other Building Materials

The chart below shows the 12-month and year-to-date price changes of other price indices relevant to the residential construction industry.

Building Materials Wholesaling and Retailing

The producer price indices for building materials wholesaling and retailing decreased 0.6% and 2.1%, respectively, the second consecutive monthly decline for each. The wholesale and retail services indices measure changes in the nominal gross margins for goods sold by retailers and wholesalers. Gross profit margins of wholesalers, in dollar terms, have increased 26.3% over the past year while those of building materials retailers rose 3.9%. Compared to pre-pandemic levels, however, retailers’ margins are 64.2% higher and margins of wholesalers are up 36.1%.

Building materials wholesale and retail indexes account for roughly two-thirds of the PPI for “inputs to residential construction, services.”

Mortgage applications decreased 6.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 3, 2022. This week’s results include an adjustment for the Memorial Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 6.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 17 percent compared with the previous week. The Refinance Index decreased 6 percent from the previous week and was 75 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index decreased 18 percent compared with the previous week and was 21 percent lower than the same week one year ago.

“Weakness in both purchase and refinance applications pushed the market index down to its lowest level in 22 years. The 30-year fixed rate increased to 5.4 percent after three consecutive declines. While rates were still lower than they were four weeks ago, they remain high enough to still suppress refinance activity. Only government refinances saw a slight increase last week,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “The purchase market has suffered from persistently low housing inventory and the jump in mortgage rates over the past months. These worsening affordability challenges have been particularly hard on prospective first-time buyers.”

The refinance share of mortgage activity increased to 32.2 percent of total applications from 31.5 percent the previous week. The adjustable-rate mortgage (ARM) share of activity decreased to 8.2 percent of total applications.

The FHA share of total applications increased to 11.3 percent from 10.8 percent the week prior. The VA share of total applications increased to 11.4 percent from 10.2 percent the week prior. The USDA share of total applications remained unchanged at 0.5 percent the week prior.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 5.40 percent from 5.33 percent, with points increasing to 0.60 from 0.51 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $647,200) increased to 4.99 percent from 4.93 percent, with points increasing to 0.44 from 0.41 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 5.30 percent from 5.20 percent, with points increasing to 0.79 from 0.69 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 15-year fixed-rate mortgages increased to 4.62 percent from 4.59 percent, with points increasing to 0.65 from 0.63 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

The average contract interest rate for 5/1 ARMs increased to 4.51 percent from 4.46 percent, with points remaining at 0.68 (including the origination fee) for 80 percent LTV loans. The effective rate increased from last week.

If you would like to purchase a subscription of MBA’s Weekly Applications Survey, please visit www.mba.org/WeeklyApps, contact mbaresearch@mba.org or click here.The survey covers over 75 percent of all U.S. retail residential mortgage applications, and has been conducted weekly since 1990. Respondents include mortgage bankers, commercial banks, and thrifts. Base period and value for all indexes is March 16, 1990=100.

Real estate prices are rising, but it’s still possible to find deals even in a red-hot housing market.

Buying a home has become incredibly difficult because most of the country has become a seller’s market.

Sale prices have escalated, pricing some people out of the market and pushing others to spending more than they wanted to.

It’s a bleak situation for anyone buying a home and it’s a market that has trapped people who might be willing to sell because they don’t see anyplace they might be able to move to.

There are, however, some ways to find a (relative) bargain even in a time of higher prices and very limited inventory.

To do that, you need to be prepared flexible, and perhaps a little daring.

These steps won’t guarantee that you find the house of your dreams — or even the house for right now — but they give you a much better chance.

1. Have a Great Realtor

Early in the pandemic, my wife and I sold our downtown West Palm Beach condo, bought a Disney-area resort property with some of the proceeds, and moved into a larger rental a few miles from downtown.

We needed to stay in roughly the same area so my son could finish high school, which he did this May.

Renting was not a long-term plan for us and with six months on our lease, slightly ahead of graduation we contacted our long-time Realtor.

Having worked with the same person on multiple transaction, we had a high level of trust and she generally knows what we would do without us having to convey it.

You can’t build that trust quickly — we had bought and sold two properties and purchased our resort property with this Realtor — but you should find a buyer’s agent you feel comfortable with overall.

Ideally, look for someone willing to communicate, who responds quickly, and is willing to listen to what you want.

2. Have Your Finances in Order

We lined up a real mortgage pre-approval before we started looking.

I talked to potential lenders as I had only been in a full-time job for under a year after a decade of freelancing.

That’s a complicated mortgage approval to get, so we made sure to clear most of the hurdles and find out exactly what we could afford before we began looking.

In addition, we took some small steps to make us more attractive to the lender.

That included paying off a small car loan, making sure to keep our credit card balances paid off, and making sure we had no large expenditures.

We also gathered paperwork to show where funds from some non-payroll income we had came from and we sold a small property.

3. Look at a Lot of Houses and Be Flexible

We wanted a single-family home after years of living in condos and townhouses.

It became obvious pretty much immediately that we could not afford anything suitable anywhere in Palm Beach County, so we began looking at condos/townhouses.

Most properties we saw checked most of our boxes, but lacked the amenities I wanted — resort-style pool and a gym — and were in areas that were less desirable.

With no kid in school, we had a lot of flexibility, so I opened up our search to see if we could afford a single-family home that met our needs anywhere in South or even Central Florida.

We found that the Orlando-area had a lot of choices, but since we owned a property there anyway, moving there would require selling that condo, and buying a small place in South Florida.

That was more moves than I wanted to make.

That led us to Port St. Lucie, or more specifically, the Tradition section of Port St. Lucie, which is sort of a town within a city.

Tradition had a very small amount of three-bedroom homes in our price range in developments that offered the amenities we —really I — wanted.

Moving to Port St. Lucie meant sacrificing location.

We’ll be about 40 minutes farther from family and less convenient to airports, but we could in theory afford a single-family home on a nice plot of land in a development with a pool, gym, walking trails, and a clubhouse.

Image source: Daniel Kline/TheStreet

4. Take on a Problem House

When we opened up our search to looking in Tradition/Port St. Lucie exactly three houses were available in our price range, all in the same complex.

One only had two bedrooms and we need three, but the other two seemed like prospects so we went to look at them.

The second house we saw was a mess and it needed a total redo.

The owner had also recently lowered the asking price, so we immediately decided to put in an offer.

Our agent called their agent and we made an offer slightly under asking.

As communication continued over the next few days, we upped our offer a few times until finally, after we had thought we had a deal, they told us they had accepted a cash offer from someone else.

As that was happening — literally while I was on the phone with my Realtor — another house in that complex became available at a lower asking price.

There were very few pictures and a tenant was living there who had the right to stay for 90 days after being given notice of a pending sale.

My agent hardly needed to ask if we were going to make a sight-unseen offer.

We did exactly that knowing that it could not be in worse shape than the previous home we had bid on.

Our bid was over-asking and we priced it relative to the previous house.

It was accepted and we were able to meet the sellers’ demand of a 30-day closing because we had already prepped our mortgage.

When we started the home-buying process purchasing a fixer-upper 40 minutes away from our chosen area was not even a vague consideration.

But once we saw the reality of the market, we made the choice to sacrifice location and being move-in ready over sacrificing buying a single-family home.

To buy a house or a condo in the market, most people will have to make sacrifices, but ultimately we got a house, that with a lot of work, we will be happy living in.

In addition, we stayed at the low-end of our budget and maintained the flexibility needed to be able to make the house the home we want.

Surging home pricesand mortgage rates cut housing affordability by 29% over the last year, as measured by the National Association of Realtors.

It’s the sharpest year-over-year decline in affordability on record.

Why it matters: The cost of housing is a major source of irritation for the American public after two years of pandemic restrictions and persistent inflation.

A separate report from housing market research firm Black Knight published yesterday shows that the monthly principal and interest payment on an average-priced home, by a buyer who puts 20% down, has gone up by roughly $600 —44% — since the start of the year.

How it works: The drop in affordability is being driven by two components.

Surging house prices: One popular gauge of home prices known as the Case-Shiller index showed home prices posting their biggest ever year-on-year gain in March when they rose 20.6%.

Surging mortgage rates: Over the last year, the rate for a conventional 30-year fixed-rate mortgage has jumped from 3% to more than 5%.

What they’re saying: “Given 2022’s affordability collapse, these [home price appreciation] levels likely are at or near the peaks for this cycle. Key question is how much and how quickly they will decline,” Bank of America analysts wrote in a research note published on Friday.

NAHB analysis of Census Construction Spending data shows that total private residential construction spending rose 0.9% in April after an increase of 0.7% in March 2022. Spending stood at a seasonally adjusted annual rate of $891.5 billion. Total private residential construction spending was 18.4% higher than a year ago.

These monthly gains are attributed to the strong growth of spending on improvements. Spending on improvements rose 1.5% in April, after a dip of 0.1% in March, as it was approaching summer, the best time of year to remodel. Single-family construction spending increased to a $477.7 billion annual pace in April, up by 0.5% over the upwardly revised March estimates. Multifamily construction spending rose 0.8% in April, after a decrease of 0.4% in March. Home building is still facing higher interest rates and supply-side headwinds.

The NAHB construction spending index, which is shown in the graph below (the base is January 2000), illustrates construction spending on single-family, multifamily and improvements have slowed down the pace since early 2022 under the pressure of supply-chain issues and elevated interest rates. Before the COVID-19 hit the U.S. economy, single-family construction and home improvement experienced solid growth from the second half of 2019 to February 2020, and the quick rebound since July 2020. New multifamily construction spending has picked up the pace after a slowdown in the second half of 2019.

Private nonresidential construction spending decreased to $503.2 billion (SAAR) in April from the upwardly revised March estimates. And it was 10.1% higher than a year ago. The largest month-over-month nonresidential spending increase was made by the class of power ($1.6 billion), followed by transportation ($0.8 billion), and class of health care ($0.35 billion).

National home prices grew at an unsustainable pace in March, reaching an all-time high. This indicates that the imbalanced market with strong demand and record-low inventory continued to put upward pressures on home prices. However, keep in mind this is a backward-looking reading.

The S&P CoreLogic Case-Shiller U.S. National Home Price Index, reported by S&P Dow Jones Indices, rose at a seasonally adjusted annual growth rate of 28.2% in March 2022, following a 27.4% increase in February. National home prices are now 60.7% higher than their last peak during the housing boom in March 2006. On a year-over-year basis, the S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index posted a 20.6% annual gain in March, after a 20.0% increase in February. The year-over-year home price appreciation slowed a little during the last quarter of 2021, and accelerated in the first three months of 2022, before the spring home-buying season from April to June.

Meanwhile, the Home Price Index, released by the Federal Housing Finance Agency (FHFA), increased at a seasonally adjusted annual rate of 19.0% in March, following a 25.0% increase in February. On a year-over-year basis, the FHFA Home Price NSA Index rose by 19.0% in March, following a 19.4% increase in February.

In addition to tracking national home price changes, S&P CoreLogic reported home price indexes across 20 metro areas in March. All 20 metro areas reported positive home price appreciation and their annual growth rates ranged from 8.8% to 57.1%. Among all 20 metro areas, fifteen metro areas exceeded the national average of 28.2%. Dallas led the way with a 57.1% increase, followed by Tampa with a 49.9% increase and Seattle with a 49.2% increase.

The scatter plot below lists the 20 major U.S. metropolitan areas’ annual growth rates in February and in March 2022. The X-axis presents the annual growth rates in February; the Y-axis presents the annual growth rates in March. Seven out of the 20 metro areas had a deceleration in home price growth, including Los Angeles, San Diego, San Francisco, Chicago, Boston, Portland, and Seattle.

WASHINGTON (May 26, 2022) – Pending home sales slipped in April, as contract activity decreased for the sixth consecutive month, the National Association of Realtors® reported. Only the Midwest region saw signings increase month-over-month, while the other three major regions reported declines. Each of the four regions registered a drop in year-over-year contract activity.

The Pending Home Sales Index (PHSI),* www.nar.realtor/pending-home-sales, a forward-looking indicator of home sales based on contract signings, slid 3.9% to 99.3 in April. Year-over-year, transactions fell 9.1%. An index of 100 is equal to the level of contract activity in 2001.

“Pending contracts are telling, as they better reflect the timelier impact from higher mortgage rates than do closings,” said Lawrence Yun, NAR’s chief economist. “The latest contract signings mark six consecutive months of declines and are at the slowest pace in nearly a decade.”

With mortgage rates rising, Yun forecasts existing-home sales to wane by 9% in 2022 and home price appreciation to moderate to 5% by year’s end.

“The escalating mortgage rates have bumped up the cost of purchasing a home by more than 25% from a year ago, while steeper home prices are adding another 15% to that figure.”

In some cases, these higher rates increase mortgage payments by as much as $500 per month. Yun notes that such price hikes are already a burden, but they become even more problematic to a family on a budget contending with rapid inflation, including surging fuel and food costs.

“The vast majority of homeowners are enjoying huge wealth gains and are not under financial stress with their home as a result of having locked into historically low interest rates, or because they are not carrying a mortgage,” Yun explained. “However – in this present market – potential homebuyers are challenged and thus may attempt to mitigate the rising cost of ownership by opting for a 5-year adjustable-rate mortgage or by widening their geographic search area to more affordable regions.”

Yun cites that more work-from-home opportunities have allowed would-be buyers to expand their home search.

There are scenarios in which the market soon improves for buyers, as well, according to Yun.

“If mortgage rates stabilize roughly at the current level of 5.3% and job gains continue, home sales could also stabilize in the coming months,” Yun said. “Home sales in 2022 are expected to be down about 9%, and if mortgage rates climb to 6%, then the sales activity could fall by 15%.

“Home prices in the meantime appear in no danger of any meaningful decline,” he continued. “There is an ongoing housing shortage, and properly listed homes are still selling swiftly – generally seeing a contract signed within a month.”

April Pending Home Sales Regional Breakdown

Month-over-month, the Northeast PHSI fell 16.20% to 74.8 in April, a 14.3% drop from a year ago. In the Midwest, the index rose 6.6% to 100.7 last month, down 2.8% from April 2021.

Pending home sales transactions in the South dipped 4.7% to an index of 119.0 in April, down 10.3% from April 2021. The index in the West slipped 4.3% in April to 85.9, a 10.5% decrease from a year prior.

The National Association of Realtors® is America’s largest trade association, representing more than 1.5 million members involved in all aspects of the residential and commercial real estate industries.

# # #

*The Pending Home Sales Index is a leading indicator for the housing sector, based on pending sales of existing homes. A sale is listed as pending when the contract has been signed but the transaction has not closed, though the sale usually is finalized within one or two months of signing.

Pending contracts are good early indicators of upcoming sales closings. However, the amount of time between pending contracts and completed sales is not identical for all home sales. Variations in the length of the process from pending contract to closed sale can be caused by issues such as buyer difficulties with obtaining mortgage financing, home inspection problems, or appraisal issues.

The index is based on a sample that covers about 40% of multiple listing service data each month. In developing the model for the index, it was demonstrated that the level of monthly sales-contract activity parallels the level of closed existing-home sales in the following two months.

An index of 100 is equal to the average level of contract activity during 2001, which was the first year to be examined. By coincidence, the volume of existing-home sales in 2001 fell within the range of 5.0 to 5.5 million, which is considered normal for the current U.S. population.

NOTE: Existing-Home Sales for May will be reported June 21. The next Pending Home Sales Index will be June 27; all release times are 10:00 a.m. ET.

In a further sign of a housing slowdown, new home sales posted a double-digit percentage decline in April, falling to their weakest pace in two years, as rising mortgage interest rates and worsening affordability conditions continue to take a toll on the housing market.

Sales of newly built, single-family homes in April fell 16.6% to a 591,000 seasonally adjusted annual rate from a downwardly revised reading in March, according to newly released data by the U.S. Department of Housing and Urban Development and the U.S. Census Bureau. New home sales are down 26.9% compared to April 2021.

“The volume of signed sales contracts significantly declined in April as the cost of purchasing a home increased in 2022 as interest rates surged higher,” said Jerry Konter, chairman of the National Association of Home Builders (NAHB) and a home builder and developer from Savannah, Ga. “Higher construction costs fueled by rising material prices and supply-side constraints along with limited existing home inventory are pricing many potential home buyers out of the market.”

In another indicator that deteriorating affordability conditions are particularly hurting the entry-level market, a year ago, 25% of new home sales were priced below $300,000, while in April this share fell to just 10%.

“The April drop for new home sales is a clear recession warning,” said NAHB Chief Economist Robert Dietz. “The median price of a newly-built single-family home increased 19.7% year-over-year. The combination of higher prices and increased interest rates are generating a notable slowing of the housing market. While the nation needs additional housing, home sales are slackening as tightening monetary policy continues to put upward pressure on mortgage rates and supply chain disruptions raise construction costs.”

A new home sale occurs when a sales contract is signed or a deposit is accepted. The home can be in any stage of construction: not yet started, under construction or completed. In addition to adjusting for seasonal effects, the April reading of 591,000 units is the number of homes that would sell if this pace continued for the next 12 months.

In an indication that builders will be slowing construction, new single-family home inventory jumped to a 9 months’ supply, up 40% over last year, with 444,000 available for sale. However, just 38,000 of those are completed and ready to occupy.

The median sales price rose to $450,600 in April from $435,000 in March and is up more than 19% compared to a year ago, due primarily to higher development costs, including materials.

Regionally, on a year-to-date basis, new home sales fell in three regions, down 16.8% in the Midwest, 19.3% in the South and 0.6% in the West. New home sales were up 6.5% in the Northeast.