Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage (FRM) averaged 3.26 percent.

“Mortgage rates stayed at or near record lows for the fifth straight week and homeowners are taking advantage with refinance activity remaining high,” said Sam Khater, Freddie Mac’s Chief Economist. “Although purchase demand declined thirty-five percent year-over-year in mid-April, demand has improved modestly over the last three weeks.”

News Facts

30-year fixed-rate mortgage averaged 3.26 percent with an average 0.7 point for the week ending May 7, 2020, up from last week when it averaged 3.23 percent. A year ago at this time, the 30-year FRM averaged 4.10 percent.

15-year fixed-rate mortgage averaged 2.73 percent with an average 0.7 point, down from last week when it averaged 2.77 percent. A year ago at this time, the 15-year FRM averaged 3.57 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.17 percent with an average 0.3 point, up from last week when it averaged 3.14 percent. A year ago at this time, the 5-year ARM averaged 3.63 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

Dear HGAR Members: Here are today’s Daily Updates – May 8, 2020: NEW YORK STATE NEWS Cuomo Says, ‘We Have the Beast on the Run.’Bolstered by continued statewide data that shows a decline in overall hospitalizations, intubations, new cases and deaths, Gov. Andrew Cuomo told reporters today at his daily COVID-19 briefing that the state is now in control of its own destiny in dealing with the Coronavirus. He said that for the first time he believes the state is ahead of the virus. “We have the beast on the run,” Cuomo said. However, the governor seemed to confirm what many observers have believed, that the re-opening of the downstate economy will not begin once his “New York on Pause” COVID-19 restrictions expire on May 15. The governor told reporters that it is very likely that he will begin his multi-phased re-opening plan in areas upstate with the construction and manufacturing industries after May 15 and said that the current downstate data does not support the lifting of any restrictions here. A total of 216 people died from COVID-19 in New York State on Thursday, May 7, down from 232 fatalities a day earlier. See Bloomberg News story. New York State Seeking $60B in Next Fed. Coronavirus Aid PackageNew York officials said on Thursday that the state requires at least an additional $60 billion in direct federal funding along with millions of dollars more from Medicaid and FEMA formula changes in the next Coronavirus aid package. The state’s request, which is part of the National Governors Association’s bid for $500 billion for all states and territories, would be spread over three fiscal years and could be used for revenue shortfalls, according to the association. See Newsday story. Senators Propose Bill to Help Local GovernmentsU.S. Senate Democratic Leader Charles E. Schumer, U.S. Senator Kirsten Gillibrand, U.S. Congressman Antonio Delgado, and U.S. Congressman Lee Zeldin announced new legislation, the “Direct Support for Communities Act,” which provides local governments with direct federal relief that can be used to pay for essential services and offset lost revenues and increased costs from the COVID-19 emergency. The local assistance would complement critical relief that states also require in this crisis, which the representatives are simultaneously aggressively pursuing. The unspecified funding under the Direct Support for Communities Act would be a critical part of a larger state and local relief package to be considered by Congress. “Under our proposal, counties, cities, towns, and villages of all sizes could count on direct, guaranteed financial relief, instead of having to layoff vital workers, cut important services, or raise taxes and fees at absolutely the worst time,” Sen. Schumer said. “Local governments deserve nothing less than our strongest federal support, and I am doing everything I can to get significant and flexible federal aid to our states and local governments included in the next legislative package Congress considers.” See announcement at schumer.senate.gov. NATIONAL NEWS How are Offices Preparing for the Return of Workers?Offices are preparing their spaces for a post-pandemic world. Companies are bringing in thermal cameras, HVAC systems that can fight bad germs, contactless coffee machines, and more as employees prepare to return to company offices in some areas of the country. “What’s important about the COVID world is that people still feel comfortable and it feels warm and inviting when they enter the building, especially after being on the trains and buses and walking in their masks,” Craig Deitelzweig, CEO of Marx Realty, told The Real Deal. “Everyone wants a hospitality feel but now they will work together, six feet apart.” See Realtor Magazine story. Suburban Office Markets Could Get Stronger Post PandemicMoody’s Analytics in a recently released report indicates that suburban office properties may make some gains over their rival central business district spaces post Coronavirus. The analysis says businesses may be prompted to consider factors expected to affect ensuing demand on office space, particularly with concerns over COVID-19 and communication systems that allow employees to work from home, according to a report at Globest.com “For many years, suburban office space fell out of favor because of the resurgence of U.S. cities,” said Ryan Severino, chief economist at Jones Lang LaSalle. “Is this COVID-19 crisis going to spur renewed interest in suburban markets, as households and employers move out of cities? Time will tell.” See story at GlobeSt.com. See full report at Moodys.com . NAR NEWS

VIRTUAL REALTORS® LEGISLATIVE MEETINGS WEEK of MAY 11-15thDon’t miss this great opportunity to attend these Live Streamed Events. Click Here for Live Streamed Events Schedule.Full Details on all meetings and to Pre-Register go to https://www.legislative.realtor/. NYSAR UPDATES Go to the NYSAR FAQ’s which were updated on May 7th with regards to:How does the COVID-19 pandemic impactFair Housing? Can I ask a client/customer/consumer if they have been exposed to COVID-19?Can I go to a property where nobody ispresent (meaning if individuals reside there, everyone has left the property) to view it or take photographs for a listing? (updated 5/7/20)

NAHB analysis of Census Construction Spending data shows that total private residential construction spending stood at a seasonally adjusted annual rate (SAAR) of $550.3 billion in March. It was up 2.3% in March, after decreasing 4.8% in February. On a year-over-year basis, total private construction spending rose 8.8%.

The monthly gains are largely attributed to the growth of spending on improvements and multifamily construction. Private residential improvements, which include spending on remodeling, major replacement, and additions to owner-occupied housing units, increased to $189.0 billion annual pace in March, up 10.2% over the February estimates. Multifamily construction spending inched up 2% in March, following an increase of 1.2% in February. Spending on single-family construction slipped 2.0% in March, the first dip since July 2019, due to the virus impacts.

The NAHB construction spending index, which is shown in the graph below (the base is January 2000), illustrates the solid growth in single-family construction and home improvement from the second half of 2019 to February 2020, before the COVID-19 hit the U.S. economy. New multifamily construction spending slowed down since August 2019, after the strong growth from 2010 to 2016 and a surge from the late 2018 to early 2019.

Spending on private nonresidential construction declined 1.8 percent over the year to a seasonally adjusted annual rate of $462.3 billion. The annual nonresidential spending decline was mainly due to less spending on the class of lodging ($4.3 billion), followed by educational category ($3.6 billion), and amusement and recreation ($2.3 billion).

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage (FRM) averaged 3.23 percent, the lowest rate in our survey’s history which dates back to 1971.

“The size and depth of the secondary mortgage market is helping to keep rates at record lows. These low rates are driving higher refinance activity and have modestly helped improve purchase demand from their extremely low levels in mid-April,” said Sam Khater, Freddie Mac’s Chief Economist. “While many people are benefitting from low mortgage rates, it’s important to remember that not all people are able to take advantage of them given the current pandemic.”

News Facts

30-year fixed-rate mortgage averaged 3.23 percent with an average 0.7 point for the week ending April 30, 2020, down from last week when it averaged 3.33 percent. A year ago at this time, the 30-year FRM averaged 4.14 percent.

15-year fixed-rate mortgage averaged 2.77 percent with an average 0.6 point, down from last week when it averaged 2.86 percent. A year ago at this time, the 15-year FRM averaged 3.60 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 3.14 percent with an average 0.4 point, down from last week when it averaged 3.28 percent. A year ago at this time, the 5-year ARM averaged 3.68 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

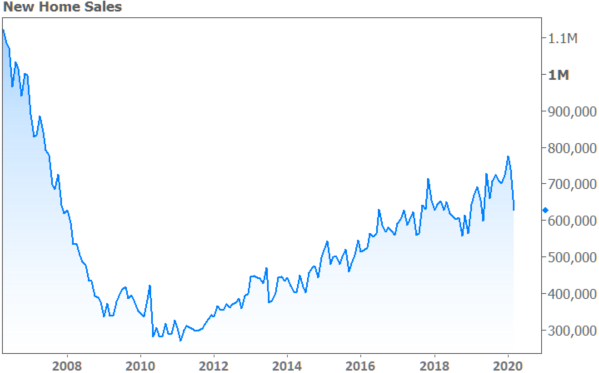

The Census Bureau and Department of Housing and Urban Development’s report on new home sales in March is the first real time indication of the impact the COVID-19 mitigation is having on total sales. The report on existing homes, released a few days ago, largely reflected the closing of contracts booked in February and early March. New home sales are counted at contract signing.

That said, the report shows a significant downturn, with a seasonally adjusted annual sales rate of 627,000 homes. This is a decline of 15.4 percent from the revised (from 765,000) 741,000 units rate in February and was down 9.5 percent from a year earlier.

The results were consistent with the wide range of forecasts from analysts polled by Econoday of 570,000 to 700,000 units. They were, however, well below the consensus estimate of 643,000.

On a non-adjusted basis, the picture was slightly better. There were 61,000 homes sold during the month compared to 66,000 in February, but sales were up by 2,000 units compared to January. For the year-to-date (YTD) there have been 186,000 new homes sold compared to 174,000 for the first three months of 2019. This is a 6.7 percent increase.

Sales were lower in all four major regions although sales in the South maintained a slight edge year-over-year. The Northeast saw sales down 41.5 percent from February and 4.0 percent lower than in March 2019. This is not surprising as Massachusetts and New York have been among the hardest pandemic-hit states. Sales in the West reflected the impact on both California and Washington with a drop of 38.5 percent for the month and 30.8 percent on an annual basis.

The Midwest saw a decline of 8.1 percent and 9.2 percent for the two earlier periods while sales in the South dipped 0.8 percent from February but were up 1.3 percent from the prior March. Despite the March losses, YTD increases were reflected across all four regions ranging from 3.0 percent in the South to 14.7 percent in the Northeast.

There were 324,000 homes available for sale at the end of the reporting period. This was estimated at a 6.4-month supply at the current rate of sales, a big jump from the 5.2 month estimate at the end of February. The median time that a completed home was on the market was unchanged from the prior month at 3.4 months.

The median price of a new home sold in March was $321,400 and the average was $375,300. In March 2019, the corresponding numbers were $310,600 and $372,700.

Robert Dietz, chief economist for the National Association of Home Builders had the following reaction to the new home sales numbers. “The pace of new home sales will post significant declines during the second quarter due to the impacts of higher unemployment and shutdown effects of much of the U.S. economy, including elements of the real estate sector in certain markets. However, given the momentum housing construction held at the start of 2020, the housing industry will help lead the economy in the eventual recovery.”