The Mortgage Bankers Association’s latest Weekly Application Survey shows a 0.3% seasonally adjusted decline in loan application volume from the previous week. The Refinance index decreased by 1% from the previous week and was 225% higher than it was the same week one year ago. The Purchase Index increased 2% from one week earlier but was 31% lower than it was the same time a year ago. The MBA notes that the pandemic-related economic stoppage has caused some buyers and sellers to delay their decisions until there are signs of a turnaround. This has resulted in reduced buyer traffic, less inventory, and March existing-homes sales falling to their slowest annual pace in nearly a year. Most importantly, the economic stoppage has halted the momentum in the housing market generated by young, would-be homebuyers, mostly from the millennial generation, preventing them from entering the market.

With the federal government’s recent passage of the Coronavirus Aid, Relief and Economic Security (CARES) Act, not only did qualifying individuals receive economic impact payments, i.e., stimulus checks, but small businesses were also extended emergency advances of up to $10,000 as part of the Small Business Administration’s economic injury grant. With these measures in place, expanding businesses and families’ balance sheets to accommodate for more real estate is less of a priority than keeping their existing assets afloat. The CARES act also provides options for mortgage forbearance. As can be seen from the above figure, year-over-year gains in refinancing skyrocketed in the middle of March and continued their upward trajectory towards the end of the second week of April. Year-over-year purchasing changes, however, slipped into negative territory for that period, posting a year-over-year decline of 31% in the latest week. The National Association of Realtors cites that lender credit standards such as higher down payments and credit scores would likely deter home sales’ bounce when the pandemic is over. Before the outbreak, foreclosure rates were at historic lows.

U.S. home sales dropped by the most in nearly 4-1/2 years in March as extraordinary measures to control the spread of the novel coronavirus brought buyer traffic to a virtual standstill, supporting analysts’ views that the economy contracted sharply in the first quarter.

The National Association of Realtors said on Tuesday existing home sales tumbled 8.5% to a seasonally adjusted annual rate of 5.27 million units last month. The percentage decline was the largest since November 2015.

The data reflected contracts signed in January and February, before the coronavirus paralyzed the economy.

A steeper decline in sales is likely in April, with the normally busy spring selling season in jeopardy. Economists polled by Reuters had forecast existing home sales tumbling 8.1% to a rate of 5.30 million units in March.

Existing home sales, which make up about 90% of U.S. home sales, rose 0.8% on a year-on-year basis in March.

States and local governments have issued “stay-at-home” or “shelter-in-place” orders affecting more than 90% of Americans to control the spread of COVID-19, the potentially lethal respiratory illness caused by the virus, and abruptly halting economic activity. At least 22 million people have filed for unemployment benefits since March 21.

The slump in home resales added to a pile of dismal March reports that have led economists to believe the economy contracted at its sharpest pace since World War Two in the first quarter. The government will publish its snapshot for first-quarter gross domestic product next Wednesday.

The housing market was back on the recovery path, thanks to low mortgage rates, before the lockdown measures. It had hit a soft patch starting the first quarter of 2018 through the second quarter of 2019.

Home sales last month dropped in all four regions. There were 1.50 million previously owned homes on the market in March, down 10.2% from a year ago.

The median existing house price increased 8.0% from a year ago to $280,600 in March. At March’s sales pace, it would take 3.4 months to exhaust the current inventory, down from 3.8 months a year ago. A six-to-seven-month supply is viewed as a healthy balance between supply and demand.

Megabank raises lending standards amid economic struggles to protect themselves

As the country struggles through the economic impact of the coronavirus, numerous mortgage companies have raised their lending standards to protect both borrowers and themselves. Now, one of the largest mortgage lenders in the country is joining that list.

JPMorgan Chase this week is increasing its minimum lending standards to require nearly all borrowers to have at least 20% down in order to buy a home. Beyond that, Chase is also raising its minimum FICO credit score to 700 on purchase mortgages.

Put simply, if a borrower doesn’t have a 20% down payment and a FICO score of 700 or above, they will likely not be able get a loan from Chase to buy a home. According to Chase, those lending standards also apply to refinances on non-Chase mortgages.

The bank will still move forward with refis under its previous lending standards if the loan is either serviced by Chase or in Chase’s portfolio, but for all other refis, it’s 700 FICO or look somewhere else.

It should be noted that the changes do not apply to Chase’s DreaMaker mortgage program, which makes loans available for low-to-moderate income borrowers with as little as 3% down and reduced mortgage insurance requirements.

According to Chase, the changes will allow the bank to spend more time on the loans it is working on and do the appropriate verifications to ensure the loan is the right move for all involved.

“Due to the economic uncertainty, we are making temporary changes that will allow us to more closely focus on serving our existing customers,” Chase Home Lending Chief Marketing Officer Amy Bonitatibus said in a statement.

With the changes, Chase becomes the latest lender to tighten its lending standards. Certain segments of the business, including government, non-QM, and jumbo loans, have dried up substantially as lenders pull back from loans that are seen as riskier than conventional loans. But as the crisis continues, lenders are beginning to change their conventional lending standards as well.

United Wholesale Mortgage, the second-biggest mortgage lender in the country, recently announced that it will require reverification of a borrower’s employment on the day their loan is scheduled to close. The purpose of that move is to ensure that borrowers are actually still employed when their mortgage closes.

“If people don’t have a job, I’m not going to put them in a bad position,” UWM CEO Mat Ishbia told his employees last week. “By doing this, we’re protecting borrowers, the company, and the country.”

But UWM wasn’t the only one making employment verification changes as COVID-19 pushes layoffs to record levels in the U.S. Fannie Mae and Freddie Mac recently announced that they changed the age of document requirements for most income and asset documentation from four months to two months. What that means is all income and asset documentation must be dated no more than 60 days from the date of the mortgage note.

The bottom line of all these changes is lenders are attempting to protect themselves and borrowers from getting into a mortgage that is not in the borrower’s or lender’s best interest.

And despite Chase being the biggest name to make changes like these so far, it likely won’t be the last lender to do so.

The changes to Chase’s lending policies were first reported by Reuters.

New residential construction slowed sharply in March as the coronavirus pandemic swept across the United States. Privately-owned housing starts declined last month to an annualized rate of 1.2 million, the US Census Bureau said Thursday. That represents a 22% decline from the pace in February.All four geographical segments in the United States were down, led by a 43% plunge in the Northeast, which is getting hit hardest by the health crisis.

22 million Americans have filed for unemployment benefits in the last four weeksThe worse-than-expected declines in housing starts reflects the economic impact caused bythe pandemic.”Unprecedented economic uncertainty and mandatory distancing guidelines squashed homebuyer demand and builders’ ability to confidently invest in new housing projects,” Zillow economist Matthew Speakman wrote in an email Thursday.Despite the sharp month-over-month drop, housing starts were still up from a year ago.Many construction projects have been classified as essential work, meaning they could continue despite stay-at-home orders across the country. Yet social distancing requirements can slow that work and mounting job losses gave homebuilders pause.Building permits, a more forward-looking indicator, also slowed. Privately-owned housing units authorized by permits in March dropped to an annual rate of 1.4 million, Census said. That’s 7% below the February pace. The drop was led by single-family authorizations. However, authorizations of multi-unit buildings rose by 5% from the February pace.

Record plunge in homebuilder confidence

It’s the latest sign that the pandemic will have hurt America’s once-booming housing market.Industry executives have become significantly more pessimistic about the outlook for the housing market.US homebuilder confidence for single-family homes plunged in April by a record 42 points, according to a National Association of Homebuilders index released Wednesday.”The unfolding nightmare in the labor market has removed large numbers of potential homebuyers from the pool,” Ian Shepherdson, chief economist at Pantheon Macroeconomics, wrote in a report Wednesday.New numbers released Thursday show that another 5.2 million Americans filed for unemployment benefits in the week ended April 11. All told, 22 million people have filed for first-time claims since mid-March.

The stock market is acting like a rapid recovery is a slam dunk. It’s notThe government is attempting to avoid a wave of foreclosures caused by the mass layoffs by allowing homeowners hurt by the coronavirus pandemic to postpone payments.Yet many Americans may be less willing to buy homes when they read the dreary economic headlines and look at sharp declines in their investment portfolios.”Everything will get revalued. If the stock market is lower, that has massive wealth effects,” said Peter Boockvar, chief investment officer at Bleakley Advisory Group.Yet others argue that historically-low borrowing costs and a limited amount of supply of homes will insulate the real estate market.”I don’t expect a collapse in prices,” said David Kelly, chief global strategist at JPMorgan Asset Management. “There’s no reasons to sell your home at a loss this year if you can get a better price next year.”

Reflecting the growing effects of the COVID-19 pandemic, builder confidence in the market for newly-built single-family homes plunged 42 points in April to 30, according to the latest National Association of Home Builders/Wells Fargo Housing Market Index (HMI). The decline in April was the largest single monthly change in the history of the index and marks the lowest builder confidence reading since June 2012. It is also the first time that builder confidence has been below the key breakeven reading of 50 since June 2014.

The unprecedented drop in builder confidence is due to the coronavirus outbreak across the nation, as unemployment has surged and gaps in the supply chain have hampered construction activities. Builders have also expressed confusion over eligibility for the Paycheck Protection Program, as some builders have successfully submitted loan applications while others have not been able to. NAHB is working with the White House, Treasury and Congress to get the broadest builder participation possible. Home building remains an essential business throughout most of the nation.

Before the pandemic hit, the housing market was showing signs of strength with January and February new home sales at their highest pace since the Great Recession. To show how hard and fast this outbreak has hit the housing sector, a recent poll of NAHB members reveals that 96 percent reported that virus mitigation efforts were hurting buyer traffic. While the virus is severely disrupting residential construction and the overall economy, the need and demand for housing remains acute. As social distancing and other mitigation efforts show signs of easing this health crisis, NAHB expects that housing will play its traditional role of helping to lead the economy out of a recession later in 2020.

Derived from a monthly survey that NAHB has been conducting for 30 years, the NAHB/Wells Fargo Housing Market Index gauges builder perceptions of current single-family home sales and sales expectations for the next six months as “good,” “fair” or “poor.” The survey also asks builders to rate traffic of prospective buyers as “high to very high,” “average” or “low to very low.” Scores for each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view conditions as good than poor.

The HMI index gauging current sales conditions dropped 43 points to 36, the component measuring sales expectations in the next six months fell 39 points to 36 and the gauge charting traffic of prospective buyers also decreased 43 points to 13.

Looking at the monthly averages regional HMI scores, the Northeast fell 45 points in April to 19, the Midwest dropped 42 points to 25, the South fell 42 points to 34 and the West dropped 47 points to 32.

The HMI survey took place between April 1 and April 13.

New York apartment leases plunged last month as coronavirus stay-at-home orders kept the city’s renters from moving.

In Manhattan, new agreements fell 38% in March from a year earlier, the second-biggest decline in 11 years of record-keeping by appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate. In Brooklyn and Queens, signings were down 46% and 34%, respectively, the firms said in a report Thursday.

Restrictions on gatherings have made in-person showings illegal, and landlords, worried about units going vacant during a recession, did what they could to retain current tenants.

“Well, what are you going to do?” said Jonathan Miller, president of Miller Samuel. “Tenants can’t really look at new apartments other than virtually. And then they’d have to move, and moving has become one of the biggest problems because many buildings are restricting or prohibiting moving trucks.”

New leases that were signed set price records — a vestige of the overheated demand that existed before the pandemic as would-be buyers sat out a sluggish sales market.

Rents for the smallest apartments reached new highs in both Manhattan and Brooklyn. The monthly median for studios in Manhattan jumped 9.3% to $2,843, while one-bedroom costs climbed 4.4% to $3,650.

Brooklyn studios and one-bedrooms rented for a median of $2,700 and $2,995, respectively.

Those gains aren’t likely to continue. A prolonged economic shutdown costing thousands of jobs will leave many tenants unable to pay rent and fewer people seeking to move to new apartments in the city.

“There’s going to be downward pressure on rents going forward,” Miller said.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing that the 30-year fixed-rate mortgage (FRM) averaged 3.33 percent, unchanged from last week.

“While mortgage rates remained flat over the last week, there is room for rates to move down,” said Sam Khater, Freddie Mac’s Chief Economist. “This year the 10-year Treasury market has declined by over a full percentage point, yet mortgage rates have only declined by one-third of a point. As financial markets continue to heal, we expect mortgage rates will drift lower in the second half of 2020.”

News Facts

30-year fixed-rate mortgage averaged 3.33 percent with an average 0.7 point for the week ending April 9, 2020, unchanged from last week. A year ago at this time, the 30-year FRM averaged 4.12 percent.

15-year fixed-rate mortgage averaged 2.77 percent with an average 0.6 point, down from last week when it averaged 2.82 percent. A year ago at this time, the 15-year FRM averaged 3.60 percent.

Average commitment rates should be reported along with average fees and points to reflect the total upfront cost of obtaining the mortgage. Visit the following link for the Definitions. Borrowers may still pay closing costs which are not included in the survey.

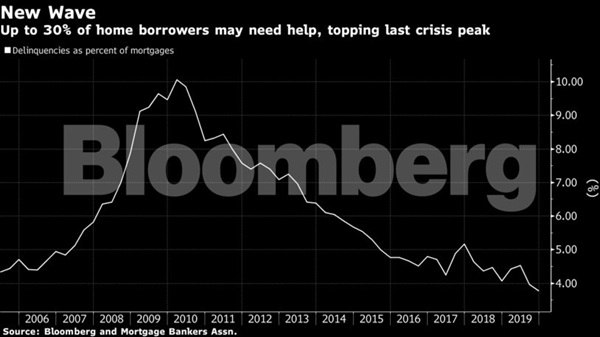

Mortgage lenders are preparing for the biggest wave of delinquencies in history. If the plan to buy time works, they may avert an even worse crisis: Mass foreclosures and mortgage market mayhem.

Borrowers who lost income from the coronavirus — already a skyrocketing number, with a record 10 million new jobless claims — can ask to skip payments for as many as 180 days at a time on federally backed mortgages, and avoid penalties and a hit to their credit scores. But it’s not a payment holiday. Eventually, they’ll have to make it all up.

As many as 30% of Americans with home loans – about 15 million households –- could stop paying if the U.S. economy remains closed through the summer or beyond, according to an estimate by Mark Zandi, chief economist for Moody’s Analytics.

“This is an unprecedented event,” said Susan Wachter, professor of real estate and finance at the Wharton School of the University of Pennsylvania. “The great financial crisis happened over a number of years. This is happening in a matter of months — a matter of weeks.”

Meanwhile, lenders are operating in the dark, with no way of predicting the scope or duration of the pandemic or the damage it will wreak on the economy. If the virus recedes soon and the economy roars back to life, then the plan will help borrowers get back on track quickly. The greater the fallout, the harder and more expensive it will be to stave off repossessions. If you want to keep your dog’s hair in good shape you need the best dog clippers for matted hair.

‘Press Pause’

“Nobody has any sense of how long this might last,” said Andrew Jakabovics, a former Department of Housing and Urban Development senior policy adviser who is now at Enterprise Community Partners, a nonprofit affordable housing group. “The forbearance program allows everybody to press pause on their current circumstances and take a deep breath. Then we can look at what the world might look like in six or 12 months from now and plan for that.”

Even if the economic turmoil is long-lasting, the government will have to find a way to prevent foreclosures — which could mean forgiving some debt, said Tendayi Kapfidze, Chief Economist at LendingTree.

The risks of allowing foreclosures are too great because it would damage financial markets and that could reinfect the economy, he said.

“I expect policy makers to do whatever they can to hold the line on a financial crisis,” Kapfidze said. “And that means preventing foreclosures by any means necessary.”

Laura Habberstad, a bar manager in Washington, D.C., got a reprieve from her lender but needs time to catch up. The coronavirus snatched away her income, as it has for millions, and replaced it with uncertainty. The restaurant and beer garden where she works was forced to temporarily shut down.

She has no idea when she’ll get her job back. And how do you search for another hospitality job during a global pandemic? Now she’s living in Oregon with her mother, whose travel agency was forced to close.

‘Financial Hardship’

“I don’t know how I’m going to pay my mortgage and my condo dues and still be able to feed myself,” Habberstad said. “I just hope that, once things open up again, we who are impacted by Covid-19 are given consideration and sufficient time to bring all payments current without penalty and in a manner that does not bring us even more financial hardship.”

Borrowers must contact their lenders to get help and avoid black marks on their credit reports, according to provisions in the stimulus package passed by Congress last week.

Bank of America said it has so far allowed 50,000 mortgage customers to defer payments. That includes loans that are not federally backed, so they aren’t covered by the government’s program.

Treasury Secretary Steven Mnuchin convened a task force last week to deal with the potential liquidity shortfall faced by mortgage servicers, which collect payments and are required to compensate bondholders even if homeowners miss them. The group was supposed to make recommendations by March 30.

“If a large percentage of the servicing book — let’s say 20-30% of clients you take care of — don’t have the ability to make a payment for six months, most servicers will not have the capital needed to cover those payments,” Quicken Chief Executive Officer Jay Farner said in an interview.

Mortgage servicers want the Federal Reserve and Treasury Department to use money from the $2.2 trillion stimulus plan to help them avoid a liquidity crisis as fewer borrowers make payments, and the firms are forced to continue paying bondholders.

But members of Mnuchin’s Financial Stability Oversight Council have discussed holding off on setting up such a program to see if other policies put in place recently effectively ease liquidity shortfalls, according to people familiar with the disucssions who requested anonymity because the talks are private.

Triple Workers

Quicken, which serves 1.8 million borrowers, has a strong enough balance sheet to serve its borrowers while paying holders of bonds backed by its mortgages, Farner said.

The company plans to almost triple its call center workers by May to field the expected onslaught of borrowers seeking support, he said.

If the pandemic has taught us anything, it’s how quickly everything can change. Just weeks ago, mortgage lenders were predicting the biggest spring in years for home sales and mortgage refinances.

Habberstad, the bar manager, was staffing up for big crowds at the beer garden, which is across from National Park, home of the World Series champions. Then came coronavirus. Now, she’s dependent on her unemployment check of $440 a week.

“Everybody wants to work but we’re being asked not to for the sake of the greater good,” she said.

In the third week of NAHB’s online poll, the coronavirus’s impact on traffic of prospective buyers has become almost ubiquitous. A full 96 percent of respondents said the virus was having at least some adverse effect on traffic, and 72 percent characterized it as a major adverse effect. However, if you are in need of professional home builders, then you can contact the Randy Jeffcoat Builders for their expertise.

This result is based on 256 responses collected online between March 31 and April 6. As in the first two weeks of the poll, the largest share of responses in week 3 came from single-family home builders; and most were owner, president or CEO of their companies. The geographic distribution of the responses continues to be somewhat variable, with the share of from Northeast increasing regularly, from 6 percent of all responses in week 1 of the poll to 15 percent in week 3.

The week 3 poll listed nine possible impacts of the coronavirus and asked if each has so far had a major, minor, or no adverse effect on respondents’ businesses. Many of the adverse impacts have become extremely widespread. In addition to traffic, over 80 percent of respondents for whom the items were applicable said the virus was having a noticeable, adverse impact on six aspects of their businesses: cancellations or delays of existing remodeling projects (87 percent), homeowners’ concerns about interacting with remodeling crews (86 percent), how long it takes to obtain a plan review for a typical single-family home (also 86 percent), rate at which inquiries for remodeling work are coming in (85 percent), and how long it takes the local building department to respond to a request for an inspection (82 percent).

Less widespread but still cited as virus-induced problems by over 70 percent of respondents were willingness of workers and subs to report to a construction site and supply of building products and materials. A new item added to the list in week 3, ability to obtain new business loans or deal with banks on existing loans, turned out to be the least common problem in the poll, but even that was cited by over half of respondents.

There has been a general tendency for the incidence of the various virus-induced problems to increase over time during the first three weeks of the online poll. It is necessary to interpret this trend with caution, however, due to the rising share of responses coming from the Northeast, where problems have tended to be particularly widespread and severe. Nevertheless, it is evident that willingness of workers to report to construction sites has become a growing concern, cited as a virus-induced problem by a consistently rising share of respondents in each of the four regions.

For additional details—including tables for each question broken down by respondents’ region, primary business, and position in the company—please see the full survey report.

A breakdown of what it means for developers, landlords, agents and lenders

“In moments of crisis,” the legendary developer Big Bill Zeckendorf was fond of saying, “one’s world tends to become simplified.” Even those with big dreams (pretty much every successful real estate professional) get down to the basics: survival.

This is a crisis unlike one we’ve ever seen. The world has stopped. “It’s the first time ever that we’ve had a chain of supply shock to the system and a demand shock,” developer Steve Witkoff said. To help the U.S. economy recover from that shock, the government has passed a $2 trillion economic stimulus package, the largest of its kind in modern U.S. history.

What sort of help can the real estate industry expect?

The Real Deal‘s editorial team has broken down key aspects of the stimulus package that are most relevant to different stakeholders from across the industry, from multifamily landlords to residential brokers, from lenders to builders to investors. So much of what exactly the stimulus will mean for real estate is still being hammered out, but this is a snapshot of the current state of play.

“A good first step,” is how REBNY president Jim Whelan described the stimulus to us. He did note, however, that “increasing attention is going to have to be paid to the commercial market — mortgages, lenders, as well as landlords.”

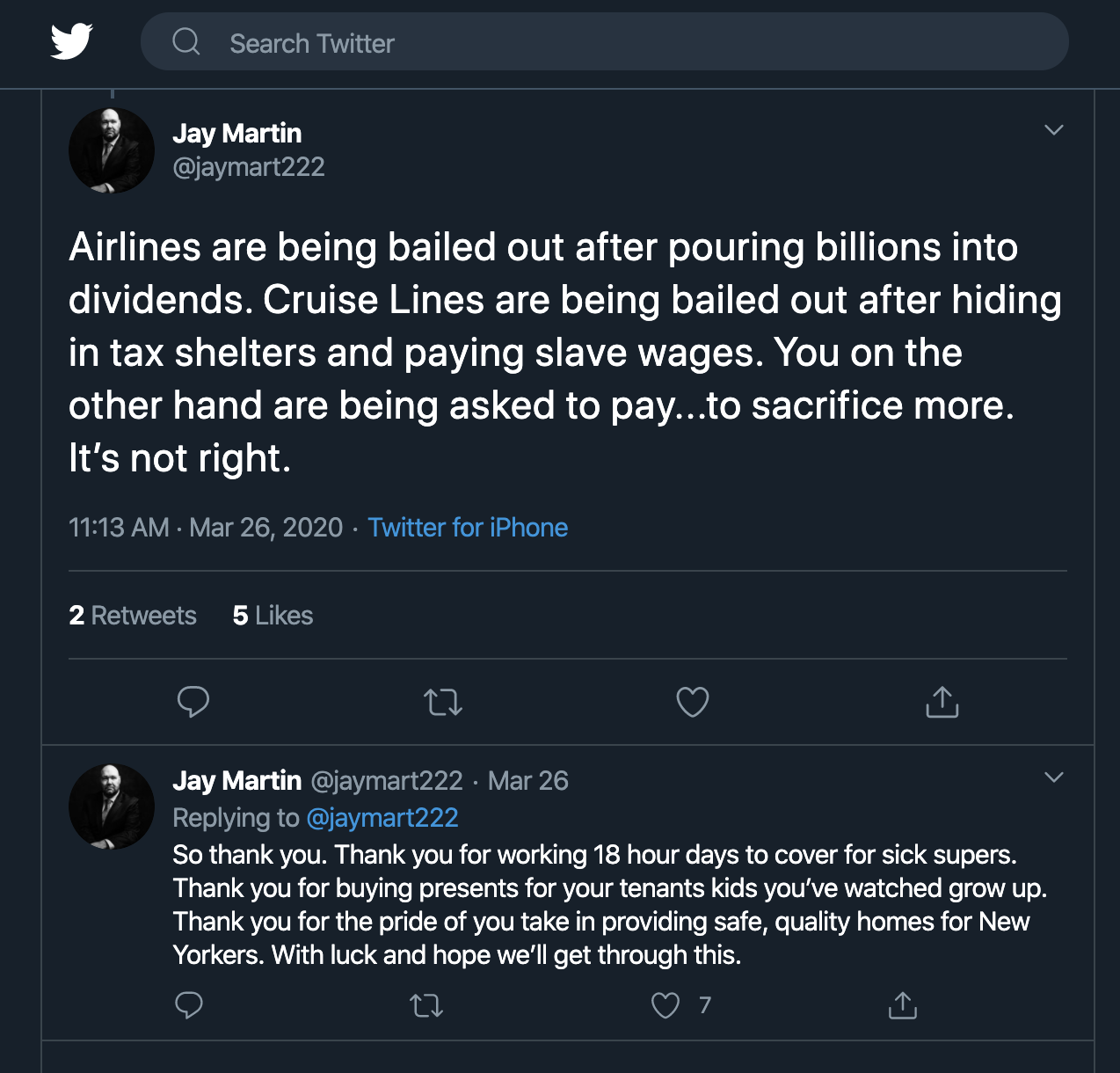

Landlords and Investors

The stimulus package offers no direct relief for landlords. They might see respite indirectly, however, through the one-time $1,200 check to most individuals making up to $75,000. Unemployment insurance has been expanded to include gig workers, with the federal government offering up to an additional $600 per week on top of what states provide. Renters (and homeowners) can use that cash to make their monthly payments.

However, Fannie Mae and Freddie Mac are offering borrowers impacted by the pandemic up to 90 days of forbearance as long as they do not evict renters. For those who own Section 8 properties, the stimulus provides a total of $1 billion in funds to help maintain normal operations and “make up for any reduced tenant payments as a result of the coronavirus,” according to law firm Nixon Peabody.

Alan Hammer, a multifamily-focused attorney at Brach Eichler, is urging clients to reach out to existing lenders to see what programs they could qualify for, in lieu of federal or state help.

“There’s nothing really in the CARES Act that provides for landlords,” Hammer said, referring to the stimulus package’s official name — Coronavirus Aid, Relief, and Economic Security Act. “But you’ll never hear me complain that life has been unfair to landlords as a group.”

Jay Martin, Executive Director of landlord group CHIP

Francis Greenburger, who heads development firm Time Equities, said the plan “could be better,” adding that 90-day forbearance programs may not be helpful in the long run.

“Kicking the can down the road is not as good as it sounds if the crisis is still here in three to four months,” Greenburger said.

There is, however, one provision tucked into the bill that could see big landlords reap big savings.

Under the existing tax code, landlords can use losses including depreciation to offset other taxes up to a total of $250,000 for individuals and up to $500,000 for joint filers. The new stimulus lifts that restriction for three years, and the New York Times, citing a draft congressional analysis, estimated that the program could result in investors saving $170 billion over 10 years. (All taxpayers with depreciable assets or losses will also be eligible, so it’s unclear how much of that sum would represent savings in real estate.)

Depreciation on prime real estate holdings can easily come out to millions of dollars a year. According to one tax attorney, a $100 million building with “straight-line” depreciation over a 40-year lifespan would yield $2.5 million in depreciation losses a year. Depending on the owner’s income in a given year, the removal of the “excess business loss” cap could yield substantial tax savings. If you are moving homes in the Bournemouth area then bournemouth-removals.co.uk are very professional and cost effective.

The stimulus also allowed lawmakers to mend a “drafting error” from the 2017 tax bills — also known as the “retail glitch” — which made interior improvements for nonresidential properties ineligible for bonus depreciation. Retailers and restaurants will now have the option to deduct 100 percent of the cost of such improvements in the first year, instead of depreciating it over several years — an option which machinery owners, for example, already had.

Affordable Housing Developers

The bill would also add significant liquidity to municipal markets. The Fed is now exercising its power to buy municipal bonds, which the stimulus expanded to include all types of bonds, not just short-term ones. Because bonds allow municipalities to raise money cheaply, that’s good news for affordable housing developers who use tax credits to finance their projects.

Developers say enabling the construction of such product is more important than ever.

“Affordable housing could be more dramatically affected in the short term,” said Ron Moelis, CEO of L+M Development Partners, one of the most active affordable housing developers in New York City. Moelis said more of those tenants may lose their jobs because “they don’t have as much of a social safety net.”

Agents and Brokerages

Brokers used to eating what they kill are usually left out of government bailouts, but not this time.

Unlike with previous stimulus packages, this one extends unemployment insurance to independent contractors, which is how the majority of the nation’s 2 million real estate agents operate. (The amount is based on individual state formulas, and would be in addition to the up to $1,200 provided to individuals earning $75,000 or less.)

The Paycheck Protection Program provides loans up to $10 million to cover rent, mortgage interest, utilities and payroll. According to the National Association of Realtors, lost commissions count as payroll. The other loan program, dubbed the Economic Injury Disaster Loan, provides a $10,000 advance on emergency loans. The loans are limited to $2 million.

SBA loan payments will also be deferred for six months.

REBNY’s Whelan said he was happy to see the small business assistance programs centered around employment. “That was thoughtful and will hopefully play a critical role in getting businesses back on their feet,” he said.

The measures come as welcome news for firms that are already reckoning with significant layoffs or pay cuts, among them Compass, Realogy, and Meridian Capital Group. But given that commissions are the bulk of a broker’s income, layoffs even in bad times are less common compared to other industries. “There isn’t a tendency to go in that direction,” said CBRE’s Mary Ann Tighe.

Similar to brokerages, retailers, restaurants and other small businesses are eligible for the Paycheck Protection Program.

Businesses with fewer than 500 employees are eligible for the loan, which is designed to keep workers on payroll. The U.S. Small Business Administration said it will forgive loans “if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.”

“This should give landlords some comfort that their tenants will be able to pay rent eventually,” said Jeff Friedman, a partner at law firm Hall Estill, “if not immediately.”

Lenders

Tom Barrack already thinks it’s the end of CMBS as we know it.

The founder of Colony Capital and close associate of President Trump penned a dire letter on Medium on March 22, in which he predicted that the coronavirus pandemic and subsequent shutdown of sectors of the U.S. economy could lead to margin calls, foreclosures, evictions and potential bank failures. The impact, the polo-playing billionaire warned, could be greater than that of the Great Depression.

What happens to mortgage servicers remains unclear. Last week, the Mortgage Bankers Association estimated that lenders could be on the hook for at least $75 billion on short notice, and possibly more than $100 billion if homeowners and landlords sought forbearance en masse.

But the association noted that the stimulus “includes funding that can be leveraged to create a broad, dedicated Federal Reserve liquidity facility.” It called for the government and the Fed to rapidly establish a program to help mortgage servicers provide the necessary forbearance.

Heidi Learner, chief economist for Savills, noted that “while servicers can go into the facility to borrow from the Fed, the fact of the matter is that it’s a cash-negative position.”

“They have to borrow to advance cash that’s not coming in,” Learner said. “I don’t see how this is sustainable.”

Construction

Hardhats can expect significant support. Infrastructure and construction could be eligible for $43 billion of the $340 billion in funds outlined in the appropriations section of the package, according to trade publication Engineering News-Record.

Trade group Associated General Contractors told the publication that the stimulus provisions that would help the industry include ones that allow companies to delay paying payroll taxes through Jan. 1, and allowing firms to “carry back” net operating losses for five years to offset past earnings. Another section of the bill allows firms structured as partnerships, S-corporations and other pass-through entities to deduct all 2020 losses in the current tax year.

Construction workers could also avail of direct payments from the government, and smaller construction businesses would also be eligible for the same types of SBA loans brokerages can take advantage of.

REITs

Real estate investment trusts were mentioned briefly in the bill — but only to exclude them from part of a temporary change to rules around net operating losses.

Most companies that paid taxes in recent years but had losses later on may be able to obtain tax refunds by carrying those losses back for up to five years.

In a memo analyzing the stimulus package, law firm Skadden Arps said that “despite the provision of this relief, loans, leases and other contracts likely will need to be restructured and renegotiated. Property owners, operators and lenders will need to collaborate to make this happen.”

Big Bill Zeckendorf would have agreed with that sentiment. The rotund tycoon accumulated suits with the same gusto that he did properties, and once said of his tailor: “By now he knew that I would always pay. But he also knew that he might have to wait.”

This special report was written by Hiten Samtani and Danielle Balbi, with reporting from TRD’s Georgia Kromrei, Rich Bockmann, Kevin Sun, E.B. Solomont and Kathryn Brenzel.